Guidelines for dealing with suspected financial irregularities in the foreign service

Guidelines/brochures | Date: 11/12/2018 | Ministry of Foreign Affairs

As of 11 December 2018 (Replaces the previous guidelines of 18 March 2011).

1 Introduction

Zero tolerance of financial irregularities is to be practised in the Foreign Service. This means that the Foreign Service is to respond to any deviations from the rules and conditions that form the basis for the management of the Ministry’s funds, including agreements relating to operational activities and grant management. The form of response will be adapted to the nature and severity of the irregularity.

The guidelines apply to the Foreign Service (Ministry of Foreign Affairs and diplomatic and consular missions) and are designed to ensure that correct procedures are followed when dealing with cases of suspected financial irregularities. They apply to all funds managed by the Foreign Service, both operating funds and grant funds.

The Guidelines must be viewed in conjunction with current applicable legislation and the current Ethical Guidelines for the Public Service.

2 Scope of the guidelines

2.1 Financial irregularities and breaches

The term financial irregularities is used in these guidelines as a general term for financial practices or conduct that are illegal or that involve misuse of Ministry funds.

Examples of financial irregularities include corruption, embezzlement, misuse of funds, fraud, theft, accounting violations, favouritism or nepotism, or other abuse of position in connection with the funds provided by Norway. Grant agreements define and give examples of financial irregularities that are prohibited under the agreements. Corruption and other forms of economic crime are regulated by Norway’s criminal legislation.

The term breaches is used here as a general term for various kinds of breaches of conditions and agreements. The terms ‘financial irregularities’ and ‘breaches’ are partly overlapping, since a financial irregularity will involve a breach of an agreement. Many kinds of breaches, for example delayed reporting, will not, however, constitute a financial irregularity. Breaches may also require a response from the Ministry, depending on their nature and the provisions set out in the agreement concerned.

When the Ministry makes funding available under an agreement, the agreement partner (grant recipient) undertakes to use the funding provided in accordance with the agreement, including in cases where the funding is allocated to third parties. Any deviations from the provisions of the agreement provide grounds for a response from the Ministry.

All cases relating to financial irregularities will be followed up by the Foreign Service Control Unit, while cases involving breaches that are not related to financial irregularities will normally be followed up by the unit responsible for managing the agreement concerned.

2.2 Other unacceptable conditions or issues of concern

These Guidelines for dealing with suspected financial irregularities in the Foreign Service are, as far as possible, to be used in cases that involve unacceptable conditions or issues of concern such as violations of laws, rules and instructions in connection with case processing or the performance of tasks in an official capacity. The Foreign Service has separate guidelines that are to be used when dealing with personnel matters, the Guidelines for dealing with conflicts, harassment or other improper conduct.

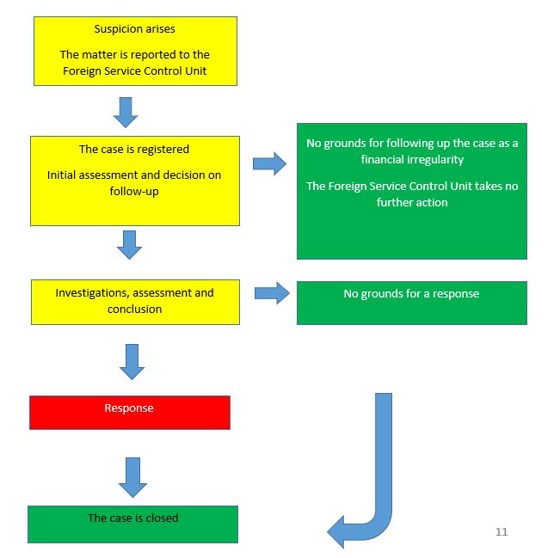

3 Procedure for dealing with cases of suspected financial irregularities

In somewhat simplified terms, the procedure for dealing with cases of suspected financial irregularities is as follows:

The individual steps are described in more detail below.

3.1 Suspicion arises. The matter is reported to the Foreign Service Control Unit.

It is usually in connection with ordinary case processing that a suspicion of financial irregularities arises. Typically, a suspicion will arise in cases where there is conflicting information or where information is incomprehensible or inadequate.

The nature and gravity of irregularities vary. Simply put, they involve an action or omission that is in violation of current legislation or agreements. If the irregularity is related to a specific agreement, the agreement will be a vital reference document in assessing whether or not an irregularity has taken place and how the case should be followed up.

The unit that has budget responsibility for the funds in question has an obligation to investigate any irregularities that are detected. Any suspected financial irregularities are to be reported in writing without undue delay to the Foreign Service Control Unit. If there is any doubt as to whether the case involves financial irregularities or should be reported, the Foreign Service Control Unit should be consulted.

Usually, reporting to the Foreign Service Control Unit will be done by management, but individual employees may also contact the Foreign Service Control Unit directly.

Everyone has the right to report issues of concern. As an employee, you have a duty to inform the employer of any circumstances or conditions that could cause loss or damage to the employer, employees or the immediate environment.

All employees have a duty to report any suspected financial irregularities.

All those who report an issue of concern may choose to remain anonymous.

More information on reporting concerns can be found on UDintra (click on ‘Gå til’ in the top right-hand corner, and then click on the ‘Whistleblowing’ button in the box that appears). There you will find, among other things, the Guidelines for whistleblowing and reporting issues of concern in the Foreign Service.

Project partners may also detect or report deviations from rules or regulations in connection with their work to follow up projects. In some cases, sources inside a partner organisation may report possible irregularities.

The Foreign Service is to work to ensure that multilateral organisations, global funds and programmes, and other international partners establish satisfactory systems for the prevention, detection and follow-up of financial irregularities. The Foreign Service Control Unit is to be kept informed about the work being done by these actors in this area. Cooperation agreements must be put in place to ensure that cases of suspected financial irregularities involving funding from Norway are reported to the Foreign Service Control Unit.

- Provide a reference number or code for the agreement (PTA number or other information about the agreement);

- Describe as clearly as possible what has happened and indicate how reliable the information is;

- Say what has been done and what steps are being planned in order to establish the facts of the case;

- Send or provide access to relevant documentation;

- Provide any other information you think the Foreign Service Control Unit should have in order to assess how the case should be followed up; and

- Follow the rules on handling personal data and sensitive information.

3.2 Registration, initial assessment, and decision on follow-up

When an issue of concern has been reported to the Foreign Service Control Unit, the Control Unit will make an initial assessment of the case and decide whether to register it as a case of suspected financial irregularities and how it should be dealt with.

The Foreign Service Control Unit will register the case in UDsak and will give the person who reported the matter the case number. This case number is to be included in all further correspondence. Access to cases relating to financial irregularities and other unacceptable conditions or issues of concern is restricted in UDsak.

The person who reported the matter will normally be kept informed about how the case will be followed up, or if the Foreign Service Control Unit has decided not to take any further action. Exceptions may be made in situations where there are reasons why this information cannot be shared, for example considerations relating to the protection of privacy or because sharing the information could compromise the investigation.

Multilateral organisations, global funds and programmes, the Financial Mechanism Office and public–private partnerships will usually be responsible for further examining and dealing with cases of financial irregularities that involve them. In such cases, the Foreign Service Control Unit will not carry out any further investigations.

3.3 Investigations, assessment and conclusion

Affected units in the Foreign Service will be kept informed when a decision has been made to follow up a matter as a suspected case of financial irregularities. The same applies to Norad and FK Norway if the case has relevance for them, for instance because they cooperate with the organisation concerned.

As a rule, the Foreign Service Control Unit will then instruct the units concerned to stop further disbursements to the project until the case has been investigated or risk-reducing measures have been implemented. The purpose of this is to prevent any further misuse of Norwegian funds. It is normally only new disbursements under the relevant agreement that will be stopped.[1]

When the investigations concern possible irregularities in an organisation that is registered in PTA, the Foreign Service Control Unit should consider asking for the organisation concerned to be marked with a warning triangle in PTA, with a message to contact the Foreign Service Control Unit before entering into any new agreements with the organisation on additional funding.

In most cases it will be necessary to investigate a suspicion of financial irregularities. The Foreign Service Control Unit decides whether to initiate an investigation, usually in consultation with the unit(s) concerned. If other donors or parties to a contract are affected, they should be contacted with a view to involving them in the further investigation.

The purpose of the investigation phase is to document the facts of the case so that any suspected financial irregularities can be confirmed or dispelled. During the investigation phase, the focus will often be on obtaining documents (reports, accounts, auditing reports – including management letters, minutes of meetings, etc.). In some cases, a field visit may be appropriate. The investigations must be carried out in such a way that they do not increase the risk that the evidence will be tampered with.

Affected units in the Foreign Service will usually be asked to obtain relevant documents relating to the case and will also be consulted on how the case should be followed up. The Foreign Service Control Unit may also ask the units for practical assistance in connection with following up the case.

In some cases, it will be necessary to engage external experts to carry out a forensic audit and/or other forms of investigation, in order to dispel/confirm a suspicion that financial irregularities have occurred.

- The specifications for a forensic audit must be tailored to the case in question.

- All procurement must be in line with the legislation on public procurement and the Ministry’s own instructions and routines (e.g. for financial management and procurement). Framework agreements on forensic audits and investigations are to be used where appropriate and relevant to the specific case.

- It is the Foreign Service Control Unit that approves the specifications for the audit/investigation, chooses who is to be given the assignment/task, and covers the costs of the forensic audit/investigation. Any deviation from this procedure must be agreed in writing.

The principle of the right to be heard must be safeguarded. Nevertheless, in some cases it is important for the further investigation that the person/organisation the suspicion concerns is not informed that the case has been reported. In such cases they must not be informed.

The investigation of the case must be completed within the period of limitation and before the time limit for submitting an application for public prosecution expires. Time limits will vary according to the legislation in the various countries and depending on which country’s rules apply. The time limits that apply should be decided at an early stage. In some cases, it may be appropriate to follow up cases even if the period of limitation has passed. This should be considered in each specific case.

In some cases, the Foreign Service Control Unit will wait for the completion of the internal investigation by the partner concerned before deciding whether there is a need for further investigations. In such cases it may be appropriate for the Foreign Service Control Unit to give guidance on the kind of investigations the partner should carry out. In special cases, the Foreign Service Control Unit can offer to fully or partially cover the costs of the investigations.

Once a case has been sufficiently investigated, the Foreign Service Control Unit is to reach a conclusion on the appropriate response. If necessary, affected units and/or the Legal Affairs Department will be consulted before a conclusion is reached. If, under the applicable guidelines, there is any doubt about how a case should be concluded, it should be referred to the Secretary General for a decision.

3.5 Response

If it has been established that financial irregularities have occurred, the Foreign Service Control Unit decides on the appropriate response. Various forms of response are described in the document Zero tolerance of financial irregularities. They include the suspension of payments; termination of the agreement; claims for the repayment of funds; claims for compensation; legal steps, including criminal proceedings; disciplinary measures; and termination of cooperation.

Follow-up

The Ministry must bring a claim for the repayment of funds within a reasonable period of time, and the rules on the limitation period set absolute limits for when claims for the repayment of funds can legally be brought.

The Regulations and Provisions on Financial Management in Central Government set out a more detailed framework for following up claims. The Ministry has entered into an agreement with the Norwegian National Collection Agency on the recovery of funds.

Civil proceedings

If the claim for repayment or compensation is contested, the Ministry should consider taking legal steps to recover the funds. When deciding which steps to take, consideration should be given to the nature of the case, the amount of funding to be recovered, the provisions of the agreement, the risks involved in the process, and the chances of recovering the funds. It is the Foreign Service Control Unit that makes a decision, having consulted the affected units and the Legal Affairs Department.

If civil proceedings have to be initiated before a foreign court, the proceedings could raise questions relating to the immunities of the state and of the posted employees. Questions relating to state immunity and/or diplomatic immunity should be considered in consultation with the Legal Affairs Department before civil proceedings are initiated. If a posted employee is requested to be a witness or to give a statement, the consent of the Ministry of Foreign Affairs must be obtained in advance, as set out in chapter 5, section 3 of the Instructions for the Foreign Service.

Criminal proceedings

Once sufficient documentation has been obtained and it has been established beyond reasonable doubt that financial irregularities have occurred, the Ministry must always consider whether to report the matter to the relevant prosecuting authority. In principle, the Ministry must report all criminal offences, including criminal offences committed by Foreign Service employees.

In each individual case, the legal basis for reporting the matter, the country in which it is to be reported and the relevant prosecuting authority must be considered. The question of whether the case should be reported to a Norwegian prosecuting authority, instead of or as well as to the local prosecuting authority, must also be considered.

There may be cases where it is sufficient to inform the prosecuting authority and/or the ministry of foreign affairs of the country concerned about the facts of the case, and to call on them to initiate criminal proceedings under the legal system in their country.

When deciding whether or not to initiate criminal proceedings in a case, an assessment must always be made of how well the legal system in the country concerned functions. A key question in an assessment of this kind will be whether the legal system upholds the fundamental principles of the rule of law. Other points that may be included in the assessment are whether or not a legal process could lead to capital punishment or other forms of punishment that are not accepted in Norway, whether or not the handling of the case will be based on rule-of-law principles, how long the legal process could take, and what the costs of a process would be. If the Ministry is considering reporting the matter in another country, consideration will have to be given to whether this will mean that the Norwegian state will become a party in the case and/or whether Norwegian civil servants will have to participate in the legal proceedings, e.g. as witnesses. In either case, a special assessment will need to be made on a possible waiver of immunity.

3.6 Closing the case

A case of suspected financial irregularities may be closed if it is concluded that there are no grounds for following up the matter further – either because it has been established that no irregularity has taken place or for other reasons, for example the case is outside the limitation period – or when the Foreign Service’s claims have been met. Decisions to close cases are taken by the Foreign Service Control Unit.

For complex cases, a brief memo summing up the case must be drawn up as a basis for a decision to close the case. Other cases may be closed on the basis of a short recommendation setting out the grounds for closing the case.

4 Handling of documents and information

All documents relating to cases of suspected financial irregularities that are of archival value are to be stored by the Foreign Service Control Unit. Caution should be exercised with regard to the distribution of documents relating to such cases. As a general rule, access to information concerning cases involving suspected financial irregularities should be restricted to the employees in the unit concerned, management staff, the diplomatic or consular mission concerned and the Foreign Service Control Unit.

Case documents are to be properly stored in accordance with the current rules. Specific requirements for the processing and storage of personal data are set out in the Personal Data Act and appurtenant regulations. Sensitive information must be handled in accordance with the Security Act and the Protection Instructions.

The Foreign Service Control Unit deals with requests for access to documents relating to cases of suspected financial irregularities. The unit concerned will be informed of any requests for access. All requests for access are processed in accordance with the Freedom of Information Act and section 18 of the Public Administration Act. Information that is subject to a duty of confidentiality by or pursuant to law is exempted from access under section 13 of the Freedom of Information Act.

The Foreign Service Control Unit publishes quarterly overviews of cases of financial irregularities that have been closed and the response taken (see regjeringen.no). It also publishes an annual report on cases of suspected financial irregularities.

[1] Stopping disbursements under existing agreements should be distinguished from putting new agreements on hold because of a suspicion of irregularities. From both an administrative law and contract law perspective, this is different from stopping disbursements under an existing agreement.