4 Climate risk and the Norwegian economy

The analysis of economic implications of climate change is fraught with difficulty. The existing knowledge base is limited, the available data are inadequate in numerous respects and the analyses carried out are subject to considerable uncertainty. Analyses based on historical experience may be of limited validity if fundamental physical circumstances are materially changed or if key social structures fail. The long time lag between emissions and warming means that implications may be further into the future than would normally be captured by model analyses. Many analyses are based on factors that lend themselves to some degree of quantification, but climate change will also have effects which are difficult to quantify, or which cannot meaningfully be quantified. Scenario analyses are therefore necessary to provide a more comprehensive illustration of the uncertainty.

Three stylised future scenarios shed light on a wide range of potential outcomes:

A – Successful climate policy: This scenario involves a successful climate policy that delivers a swift transition to a low-emission society. No significant self-reinforcing mechanisms in the climate system are triggered, thus implying that the climate changes are moderate and the worldwide economic implications are relatively minor. However, the transition to a low-emission society may be challenging for various stakeholders.

B – Late transition: Scenario B involves late climate policy tightening – following a period of further warming. We are, at the same time, «lucky» – and no self-reinforcing mechanisms in the climate system are triggered. The climate changes and economic implications are considerably more pronounced than in scenario A. There is a higher risk that the Norwegian economy will be indirectly affected by climate changes in other countries as the result of conflict escalation, diminished international cooperation and changes in global migration patterns. In addition, belated and more severe policy tightening will increase the risk of financial instability.

C – Dramatic climate change. This is a scenario involving political failure and/or the triggering of self-reinforcing mechanisms in the climate system. The economic implications of such catastrophic climate changes cannot be meaningfully quantified. Risk management advice would be of minor use, and the relevant measure is quite simply an effective climate policy that reduces the probability of ending up in scenario C.

Global factors are important to Norway. As a small, open economy holding considerable international financial wealth, Norway is highly dependent on what happens in the wider world. It is therefore necessary to adopt a global perspective in addition to the national one.

Climate change will curb worldwide economic growth. Numerous estimates indicate a global GDP loss as the result of global warming, compared to a benchmark without climate change. The consequences mount steeply with higher temperatures. In aggregate, the effects suggested by the estimates nonetheless seem modest, relative to the effort required to meet the targets under the Paris Agreement and relative to other uncertainties confronting the world economy. However, there are methodological challenges associated with the estimates and a risk analysis needs to adopt a broader perspective. Global averages conceal large differences between countries, and it is difficult to assess what implications major changes in individual countries or regions may have for the rest of the world through, for example, extensive migration. Besides, many of the implications of climate change are so serious as to not lend themselves to quantification, for example destruction of entire ecosystems or loss of entire societies through sea level rise.

Climate change may destabilise international politics. If already vulnerable states suffer major negative implications of climate change, the risk of political instability, humanitarian disaster and violent conflict will increase, both in and between states. The risk of conflict is also fuelled by the potential for climate change to cause shortages of important goods such as clean water. In addition to the possibility that war and conflict may inhibit growth in the world economy, key risk sources for the international economy may be increased migration flows, unstable food prices, supply disruption and changing production and trading patterns. An ever more closely interwoven international community means that regional crises may have greater ripple effects, and events far away can hit harder, faster and in new ways. Effects of climate change may come to dominate political decision-making processes. The institutional capacity of countries may then become so absorbed by immediate damage control as to result in little attention being paid to international cooperation to resolve global problems, including the climate problem.

A successful climate policy may also have geopolitical implications. A new energy system based on renewable energy will change production patterns and the need for cross-border transport of energy. This will create new linkages, dependencies and power dynamics. Petroleum resources are often an important source of power and conflict. A climate policy resulting in a more decentralised energy system and significantly lower petroleum revenues may change power dynamics and have a destabilising effect on certain countries that are currently dependent on such revenues.

The considerable uncertainty with regard to international developments means that the range of potential outcomes for the Norwegian economy is very wide. Over the long time horizon we have adopted, the risk outlook will be dominated by the indirect physical risk associated with how the climate change hits other countries. However, direct physical risk and transition risk may also become important, especially the direct and indirect effects of changes in the value of the petroleum wealth. The time perspective is also important in this regard. The transition risk relates to a – hopefully – limited period of time until transition to a low-emission society has taken place. The physical risk will be increasing for a long time to come, even if one succeeds with climate policy, since it takes time to reduce emissions and it takes a long time from greenhouse gas emissions are eliminated until the climate system arrives at a new equilibrium.

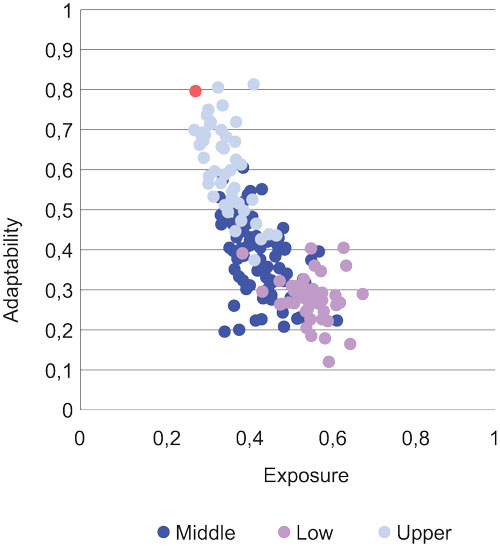

An overall assessment of the key risk factors nonetheless indicates that the Norwegian economy can, all in all, be considered relatively resilient. A moderate level of global warming and climate change will have both negative and positive effects on the Norwegian economy. The implications of major climate change are potentially severe and challenging to envisage. Rich countries in the Northern Hemisphere are generally less exposed to direct negative effects of climate change than are poorer countries in the South. Moreover, rich countries like Norway will by and large have more well-functioning institutions, a higher level of education and a more diversified industrial structure. Higher income levels and flexible labour markets imply a greater capacity for absorbing transition costs whilst transitioning to a low-emission society (see Figure 4.1). Norway seems less vulnerable to climate change than most other countries, and is also held to be one of the best placed countries with regard to adaptability.

Figure 4.1 Exposure and ability to adapt to climate changes. Countries by level of economic development. Norway is indicated in red.

Source University of Notre Dame Global Adaptation Index.

Useful insights can be gleaned by addressing climate risk from a national wealth perspective. An appropriate starting point for assessing climate risk for the Norwegian economy in the long run is to estimate how climate risk may affect Norway’s overall consumption opportunities over time, and thereby the welfare of current and future generations. National wealth does not include all factors of importance to the welfare of the population (such as the value of leisure), and climate change may also affect factors that only have an impact on national wealth over time (such as ecosystems and biological diversity), but useful insights can be gleaned by adopting a national wealth perspective. Both transition risk and physical risk are relevant in this context. For some parts of the national wealth, for example real assets in the form of buildings, roads and railways, physical risk may be the most relevant. For other parts, such as the value of oil and gas resources and financial wealth, transition risk may be the most important. However, by far the most important component of national wealth is human capital; the value of our manpower, so an important question is how that may be affected by climate risk.

It is likely that moderate climate change will have more of an impact on the composition of Norwegian production, than on its level. Both transition risk and physical risk may affect the composition of employment and economic activity in mainland Norway, but it is anticipated that this will have a relatively minor long-run impact on overall economic activity in scenarios in which major climate change is avoided. This reflects the expectation that labour and capital will in the long run have about the same expected return in most industries. The share of the economy accounted for by different industries has changed considerably over the last century, and there is reason to expect that significant changes in the allocation between industries will continue also for the remainder of this century. An adaptable economy, in which manpower swiftly finds its way into new enterprises when needs change, is less exposed to climate risk.

However, this is conditional upon the transition costs not being excessive. In the short run, there will be transition costs associated with the transition to a low-emission economy. The transition risk is an important climate risk factor for many businesses. However, if the transition takes place without any impact on general productivity, it will have no impact on the consumption opportunities of the population in the long run. There may nonetheless be scenarios in which transition costs are so high that they affect consumption opportunities over time, for example a development in line with Scenario B above, involving belated, but severe, tightening of climate policy. Such transition costs may potentially be increased through effects on financial markets.

In the case of major climate change, general productivity and productivity growth – also in the Norwegian economy – may be affected. Norwegian businesses benefit, for example, from well-functioning international trade, from research and development of knowledge which is disseminated globally and from other well-functioning international institutions. If key social structures and institutions of the world are weakened, this will also affect the productivity of Norwegian businesses. Other changes as the result of a warmer climate or associated with the transition to a low-emission society may also entail productivity effects. Lower productivity growth will mean reduced consumption opportunities over time and be reflected in national wealth through a reduction in the value of both human capital and real assets.

Industries based on exploitation of non-renewable natural resources need to be analysed separately in a national wealth perspective. These industries tend to be characterised by high economic rent, i.e. higher return than in other industries involving corresponding risk. In Norway, by far the highest economic rent is reaped in the extraction of petroleum. If such an industry is phased out before the economically viable resources have been exhausted, one cannot expect labour and capital to be able to find new uses in enterprises generating equally high returns. This constitutes a potential loss to the economy.

The value of human capital may be affected by migration flows resulting from climate change. One source of climate risk for Norway is changes in global migration patterns, which may have an impact on the composition and productivity of the population. The long-term implications of immigration for economic activity in Norway are highly uncertain, and are largely dependent on whether the immigrants find jobs, as well as their contribution to the productivity of the overall labour force.

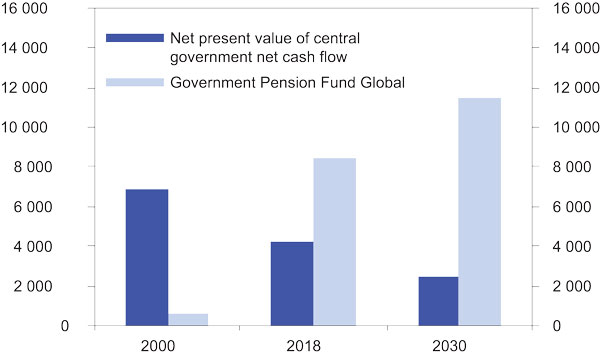

Strict global climate policy will, when taken in isolation, reduce the value of the remaining petroleum reserves. If the targets under the Paris Agreement are to be reached, greenhouse gas emissions will have to be reduced steeply towards the middle of this century. Future prices of fossil energy sources are subject to considerable uncertainty, irrespective of which climate policy is adopted by the world. There are also several different potential price trajectories for oil and gas in a situation in which the world is implementing extensive measures to curtail CO2 emissions. There is nonetheless every indication that implementation of an ambitious climate policy to curb the demand for fossil fuels will entail significantly lower producer prices than a reference pathway involving fewer climate measures. Hence, the difference between an ambitious and a somewhat less ambitious international climate policy may thus be of major importance to the value of Norway’s petroleum reserves. However, the State’s risk associated with the remaining petroleum reserves has declined considerably over the last few decades, in line with the oil and gas resources having been extracted and the central government revenues having been invested through the Government Pension Fund Global (GPFG), see Figure 4.2.

Figure 4.2 Value of the Government Pension Fund Global and the State’s petroleum reserves, NOK billion.

Source Ministry of Finance.

Lower petroleum wealth may affect other parts of national wealth. How other components of national wealth are affected by reduced petroleum wealth will depend on what are the causes behind the petroleum wealth decline. If a reduced level of activity in the petroleum industry over time results in lower wages in the economy in general, the human capital component of the national wealth may also be worth less. This suggests higher climate risk than might be indicated by the effect on the value of remaining petroleum resources alone.

Norway’s high financial wealth is exposed to climate risk. The conversion of oil and gas resources in the ground into a broad portfolio of financial assets in the GPFG has served to diversify the risk associated with Norway’s national wealth over the last few decades. At the same time as we have observed reduced exposure to the petroleum sector, the accumulation of high financial wealth has brought new sources of risk. Climate risk is one source of risk which it is of particular importance for a large long-term investor to manage. The investments of the GPFG are diversified across a large number of companies in many countries. Over time, the return on the Fund will largely reflect global economic developments. Hence, the same climate-related risk factors that affect worldwide growth will also be relevant risk factors for the Fund.

Increased precipitation and changed energy mix will affect the value of hydropower. Increased precipitation may give rise to increased power generation, at the same time as electrification generally increases power needs. In Norway, warmer weather may, when taken in isolation, result in lower demand for electrical power for heating. In coming years, climate policy is likely to increase the portion of non-dispatchable power from wind and sun in Europe. This would suggest, when taken in isolation, increased value of Norwegian dispatchable hydropower in periods of low wind and sun production. In the long run, it is uncertain what effect a decarbonisation of the European power sector would have on the value of Norwegian hydropower. An ever-increasing share of non-dispatchable power generation, with very low operating costs, will increase the frequency of periods with very low power prices in the European power market. On the other hand, a strict climate policy that reduces the value of petroleum resources may to some extent increase the value of renewable hydropower resources.

Parts of the fixed capital stock may be subject to increased capital depreciation and maintenance needs. Increased precipitation and stronger wind may result in higher maintenance costs for buildings and roads. Sea level rise along parts of the coastline may result in loss of value or higher costs associated with the relocation of buildings or roads. Adaptations to climate change may curtail such additional costs.

An increasing number of climate-related litigation claims are being brought before courts in different parts of the world. More focus on effects of, and costs associated with, climate change means that stakeholders are seeking to use the judicial system to halt activities which cause emissions or to be compensated for costs and losses resulting from climate change. Two basic types of legal action that may follow in the wake of climate change are tort actions and legal actions that challenge the validity of administrative decisions. Legal actions seeking to influence the substance of a state’s climate policy have also been observed internationally.

The risk of tort litigation increases with the extent of damage. Tort action is a legal action in which the injured parties seek to be compensated for a loss they have incurred directly or indirectly. A typical example from Norway may be compensation for homes destroyed as the result of flooding or landslips relating to climate change, whilst examples from other jurisdictions include legal action brought by government authorities against oil companies to claim compensation for increased infrastructure costs caused by climate change. Tort law in Norway is largely based on legal standards such as «negligence», with the threshold being defined through normative assessments of the acts or omission in question. What is considered to be negligent may be influenced by changes in factual circumstances, changes in the level of knowledge and changes in social expectations as to how certain situations should be dealt with. This implies that a stricter behavioural standard may be applied over time. In addition to serving a restorative purpose, tort law also has a preventive purpose in holding parties accountable. A dynamic development of the legal concepts through case law may thereby also provide incentives for improved response to new risk factors.

Legal actions can be brought against the state, moving for administrative decisions to be declared invalid. The outcome of such actions may be that activities are halted.

Litigation risk may involve large sums. It is difficult to quantify the litigation risk associated with climate change for Norway, but both legal actions to obtain compensation for losses and legal actions to halt activities or restrict the use of a resource may have a considerable financial impact on the parties involved. Even if the claimants ultimately do not prevail in a given legal action, such legal action may in itself have a number of implications for the defendant, both in the form of legal costs and the time and attention devoted to the action within the organisation, and in the form of potential reputational damage and increased uncertainty with regard to future profits.