Keynote speech at Hertie School of Governance, Berlin

Liberal values in a less liberal world? – The economic case for rules-based global integration

Historical archive

Published under: Solberg's Government

Publisher: Ministry of Finance

Speech/statement | Date: 20/02/2019

By Minister of Finance Siv Jensen (Keynote speech at Hertie School of Governance, Berlin)

"Increased opposition and decreased influence of the liberal economic order should motivate renewed efforts to build support for free and open markets and societies. This is the time to improve our model, not swap it for a less liberal one", said Finance Minister Siv Jensen (Progress Party) in her speech today.

Check against

delivery

Thank you for the invitation to come here and speak today.

I will take this opportunity to talk about how the rise of free and open markets throughout the Western world has built trust among nations and raised living standards to a level never seen in history.

I believe our efforts to promote further and deeper integration are key to meet the challenges of tomorrow. Yet, we currently see less support for the core values of the international economic order.

I will argue that the risk of weaker global institutions and of a diluted set of common rules are pressing issues that can only be met by an even stronger commitment to liberal core values.

Norway, as well as Germany, has a long history of trading overseas. The Vikings, often portrayed as primitive, were indeed sophisticated in terms of trading in distant markets. Their extensive trade relations reached as far as Greenland, the Caspian Sea, and the Mediterranean.

Indeed, the sea journeys of the early Vikings tell us that trade links between Norway and Germany go more than a thousand years back.

Recently, researchers, by using DNA from fish bones, could substantiate theories about how the Vikings supplied people of Schleswig with stockfish perhaps as early as in the 9th century.

In the following centuries, trade in the North Sea would increasingly become in the hands of German merchants.

On the Norwegian west coast, a commercial enclave of the influential Hanseatic League was established in the city of Bergen, ensuring a steady supply of Norwegian stockfish, whale oil, and hides to Germany and to ports along the Hanseatic trade routes.

These were influential forces of their time. Yet, even today, international trade, in combination with well-managed national economies, is the main explanatory factor behind the high levels of prosperity in our societies.

In fact, bringing down barriers that separate markets is probably the most successful economic policy ever pursued. From a historical perspective, nowhere is this insight more deeply rooted than in Germany:

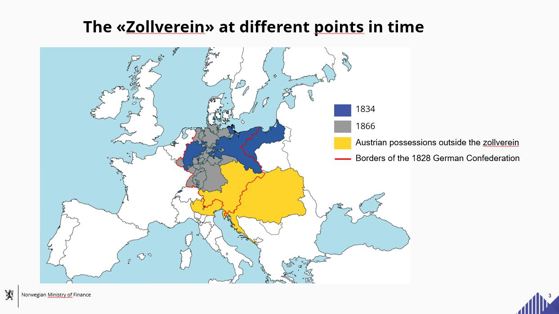

In the early 1830s, a German customs union was established, comprising among a number of, at the time, independent states. The Zollverein was the first of its kind.

With time, the union would unify a myriad of markets, previously separated by customs and tariffs. :

Whereas historians have pointed out a range of political reasons driving this unification of markets, the economic gains were also well understood. To the individual states, giving up tariffs, their primary source of revenue, seemed a high price to pay. Yet, in return, larger markets triggered a massive expansion in the productivity potential of the economy.

The economic historian Florian Ploeckl has shown how the Zollverein triggered growth in manufacturing and shifted the occupational structure towards higher income occupations.

Some decades on, in the 1860s, Sweden-Norway would sign a free trade agreement with the Zollverein, allowing the historic and commercial ties between the German and the Scandinavian markets to grow stronger.

Since then, trade liberalization at a global level has been massive. Technological developments, including improvements in transportation and information and communication technology, have reduced the distance between us. Tariffs have been driven down. As have non-tariff barriers.

Integration of markets has moved in waves. Liberalization in the 1800s was reversed by conflicts, depression and protectionism in the first half of the 1900s. The social, political and economic consequences were devastating.

From this harsh experience, a new notion of mutual dependence emerged. After the Second World War we saw a renewed belief in international cooperation among Western nations. This gave rise to an institutional architecture that would govern international relations up until today.

The IMF, World Bank, UN, OECD and the General Agreement on Tariffs and Trade, which in 1995 expanded into the World Trade Organization, all form part of what often is referred to as an international liberal order.

This system has set the stage for rules-based international trade, as opposed to power-based. It has enabled more countries to connect to global markets. By reducing national discretion, common rules also support more predictable world trade – essential to long-term investments and efficient production patterns.

Today, a large fraction of everyday consumption is produced outside national borders, sometimes in supply chains that crisscross the globe in complex ways.

During these decades, we also saw a rising tide of democracies throughout the world. With the fall of the Berlin wall and the end of the Cold War, the tide accelerated. A surge in democratic institutions and a belief in individual rights spread through Eastern Europe, Latin America and Africa.

More countries accepted membership in global institutions. What had predominantly been a Western world order would increasingly become a shared system of rules and values.

This model became an engine of economic growth and technological change. Based on a mindset, in which technological and economic development in one country is seen as the source of other countries’ trade, investment and technological change. A win-win.

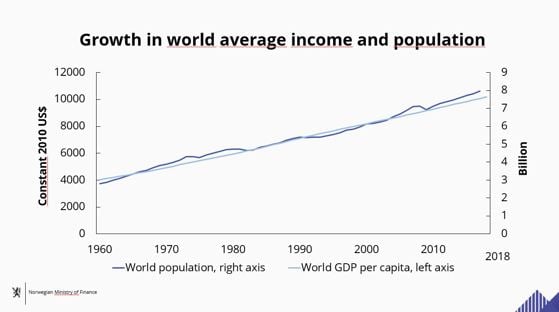

In the past 50 years, average GDP per capita has doubled. At the same time, world population has also doubled. The majority of the world population has benefitted from this astonishing rise in income.

As a result, the share of the world population living in extreme poverty has come down from one in three in 1990 to about one in ten today.

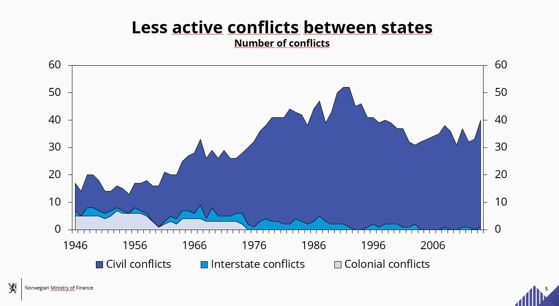

Cooperation and integration have also brought down the level of conflict internationally. As shown by this chart, interstate conflicts have been almost non-existent in recent years.

As a mirror of the Zollverein, Europe from the 1950s again became the arena of the deepest commitment to international integration ever seen.

With the objective of promoting economic prosperity and mutual dependence, the first steps were taken towards the creation of a single market in Europe.

European integration since then has resulted in the world’s largest and deepest cross-border market.

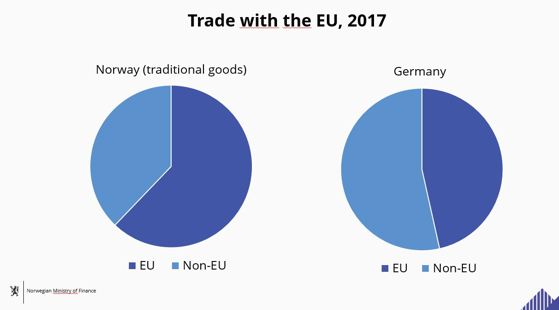

Through the European Economic Area agreement - the EEA - Norway is part of the European single market.

In fact, Norway’s economy is in many ways more deeply integrated into the EU than many EU economies. As seen from this chart, almost two thirds of Norway’s trade is with the EU, while Germany’s trade with the EU comes to less than a half.

Being part of the single market has brought great advantages to the Norwegian economy. Yet, we also face the other side of the coin. The regulatory burden can be overwhelming. I understand those who argue that regulation of the single market has become too extensive and too complex.

As a politician coming from a libertarian political tradition, I believe in the freedom of choice and limited government that empowers people and businesses to achieve their goals. In general, I believe in the virtues of markets and their ability to find the best outcome.

That said, I recognize the need to regulate markets for them to work efficiently. Indeed unregulated markets are not necessarily as well-functioning as the free markets we know from textbook economics. Rather, regulation must frame the market, reducing imbalances and imperfections, promoting easy entry and exit, and levelling the playing field.

Yet, we must regulate wisely. And only to the extent necessary. Not more, not less.

That goes for international markets as well.

Recent decades have witnessed a fall in tariffs and a rise in the regulatory complexity of advanced economies. Today, so-called “non-tariff measures” seem to pose higher barriers to trade than tariffs. As services have become the dominant sector in advanced economies, the role of tariffs has diminished further.

Yet, services are indeed characterized by high barriers to trade. In fact, the OECD suggests that barriers to trade in services largely exceed the average tariff on traded goods.

As a consequence, trade liberalization has increasingly become a question of overcoming trade barriers associated with differences in national rules and regulation. However, opening up to more trade and investment does not necessarily mean deregulation. Rather, in Europe, deep integration has partly been achieved by harmonizing regulation across markets.

Instead of widening differences between markets, supranational rules and regulations make markets more uniform. When regulatory differences are reduced, markets will work more efficiently, with fewer loopholes and more transparency.

Common standards in product markets, common competition law, common rules for public procurement and for state aid are among the measures that help bring down regulatory barriers within the European single market.

At the same time, there must be room for national adaptations, to take account of local conditions, knowledge and preferences.

Clearly, distinguishing between regulation that better could be implemented at a supranational level and regulation that is better implemented at the national level, is far from straightforward.

Resistance against “being regulated by Brussels” – one important argument leading to Brexit – illustrates how controversial this issue can be. Striking a balance requires “fingerspitzengefühl” and constant adjustments to maintain legitimacy.

As Minister of Finance, the financial sector is the part of the single market under my direct responsibility.

The financial system is critical to the functioning of the economy and a premise for economic stability. When the financial system fails to function, the economy fails.

From experience, we have learned how financial crises can cause severe and long-lasting harm to the economy. In Norway, we suffered a serious banking crisis in the early 1990s, which Carmen Reinhart and Kenneth Rogoff have ranked as one of the «Big Five» in advanced economies.

Promoting financial stability is different from many other areas of economic policymaking. While economic policy generally aims to achieve the best possible outcomes, like maximising welfare for its citizens, policies promoting financial stability aim at preventing the worst possible outcomes.

To safeguard financial stability it is necessary to regulate the financial sector.

Yet also in financial markets, we have to strike a balance. We should never forget that the art of banking is better handled by bankers than politicians.

Deep integration also implies that imbalances can spread fast between institutions and countries. Promoting financial stability across markets requires regulatory cooperation.

The financial crisis in 2008 spurred common efforts led by the G20 and the IMF to develop a set of common standards and rules for the financial sector, with the Basel Committee on Banking Supervision at the helm.

The Basel Capital Accord of 1988 was supplemented by new accords – Basel II and Basel III. Most advanced jurisdictions have transposed these standards into legislation. As a member of the European Economic Area, Norway has an obligation to implement most of the financial regulations adopted by the EU.

I understand those who argue that international common standards for governing the financial sector have become too extensive and complex. Counting the ballooning number of pages of the regulation has become a popular sport.

Still, the instability that might result from too little regulation is probably worse.

Besides the high economic costs of adverse financial shocks, recurrent financial instability undermines peoples’ confidence in the economic system. In countries with persistent financial stress, people resist taking up loans and stash their savings under the mattress, not in the bank.

Opening up to international markets increases exposure to external shocks, not only in financial markets – in all markets. International integration requires continuous adjustments and triggers shifts in the occupational composition that can indeed be painful. Both to those who sees their job opportunities diminish, as well as to the economy as a whole.

Yet, I do not believe in shielding the economy from external influences. Rather, I would argue that we must prepare for such instability, not hide.

Why? Because barriers to integration will over time cause our economies to become less in tune with economic realities outside our borders. Imbalances may rise over time and, eventually, require abrupt adjustments.

Indeed, we must not confuse stable with static. Instead, we should recognize that stable, long-term economic development is the result of continuous adaptation to economic realities.

What is more, open markets and external impulses are important drivers of economic development. By setting off changes to what and how we produce, they present our economies with new opportunities.

In fact, gains from open markets are to be found not in increased exports or more investment abroad, but rather in the ways our domestic resources are put to better use at home.

The gain from opening up the economy is therefore to be measured by the extent it translates into rising productivity. In Norway, periods of major sectorial shifts tend to overlap with periods of high productivity growth.

Let me illustrate with – to me – a familiar example:

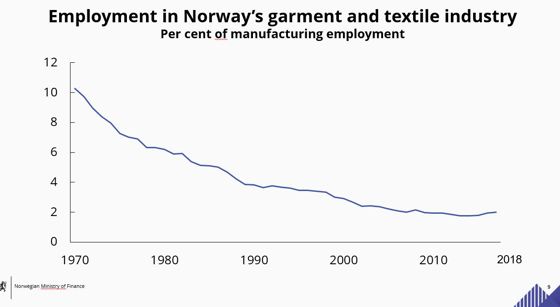

When I grew up, the garment and textile industry was a significant sector in Norway. In 1970, the industry employed one out of ten manufacturing workers, well represented by influential trade unions.

At that point, Norway had been a member of the European Free Trade Association – EFTA – for about ten years.

So had Portugal. With, at the time, a highly cost-competitive garment and textile industry.

Fierce competition from Portugal, and others, led to a major restructuring of Norway’s garment and textile industry in the following years. By the turn of the millennium, the sector employed only three per cent of manufacturing workers, or as few as 3 per thousand of all employees. This sectorial shift would give rise to job creation in sectors with higher productivity.

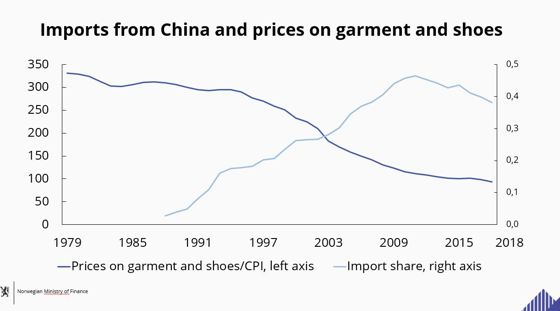

When China entered the WTO in 2001, Norway was well positioned to meet the Chinese supply shock. In fact, to Norway, the entry of China into the world market did not imply job losses. Rather, we saw a sharp decline in prices on products we no longer produced, among them clothing and shoes.

And higher demand for our exports. The result was a massive rise in our overall terms of trade.

The lesson from this story can be summarized as follows: We should not be afraid of change. When firms fail, or even entire sectors become marginalized, they give the floor to others – often with higher productivity.

And, when markets function well, higher productivity translates into more generous compensation of employees and increasing return on investment.

There is nothing new in this insight. More than 200 years ago, Adam Smith gave us a theoretical basis for how economies thrived with the division of labour. Within the next decades, David Ricardo presented the theory of comparative advantage.

These early theories of international trade have been elaborated and refined – still, the overarching message is clear and consistent: Opening up markets allows for an improved composition of production and consumption.

Their insights have been supported by experience. For centuries, we have witnessed how integration into international markets has boosted business potentials, increased personal freedom and lifted overall living standards. The result is a world that is more interconnected than ever seen in history.

To the consumer, opening up the economy gives access to more and cheaper goods and services. Open markets also set in motion technology transfers. And they provide greater incentives for research and investment in technology.

When introduced, technological developments benefit from economies of scale offered by larger markets, often setting off significant cost reductions in early production of new technology.

With time, more and more countries have chosen to open their markets. A number of low-income countries have in recent decades, increased their participation in world trade. Many of which have become significant production sites in international value chains – allowing them to become deeply integrated in a relatively short time.

So far, common rules and systems for dispute settlement have supported a peaceful integration of these new economies into the global market. It is easy to overlook how astonishing this achievement is.

When China re-entered the world stage in the years leading up the turn of the millennium, it represented a major supply shock to the world economy. In terms of labour and of goods. For a long time this transition went on peacefully.

Today, the global trading climate is changing. Trade is at the core of the ongoing rivalry between the US and China. The idea of rules-based trade is compromised by the implementation of protectionist measures.

A few days ago, the US administration concluded an investigation report on whether imports of cars and car parts pose a threat to US national security. The world follows developments closely, as a sharp rise in tariffs may cause serious harm to the world economy – including the economies of Germany and the US itself.

Protectionist tendencies are spreading, not only in the US, but also worldwide. Whereas tariffs have come down to low levels globally, the use of protectionist measures, more broadly defined, moves in the wrong direction.

Considering our long history as trading nations, one might ask: How can anyone oppose the benefits of trade?

In recent years, increasing inequality in advanced economies has raised doubt as to whether open markets and technological change serve the interests of the majority. Whereas the richest percentiles have seen their wealth soar, the low- and medium-skilled perceive income growth and opportunities to be limited.

Another strand of opposition is rooted in the fear that national sovereignty is compromised by liberalization. To some extent, international commitments might imply less room to regulate at the national level.

Reducing national discretion is indeed the means by which markets become more uniform. Yet, there is always a balance. And international agreements in general leave ample room for national differences in regulation.

Still, we must take the discontent seriously! The legitimacy of pursuing further integration rests with our ability to translate the opportunities of international markets into broad-based rises in living standards.

Only with a fair distribution of opportunities and gains can we expect confidence in the political agenda to grow stronger.

Going forward, a lack of support may impede international institutions’ ability to carry out their task. They represent the liberal order that has served our economies so well.

If undermined, it will be bad news for all. Both for open economies, heavily dependent on trade, and for economies where potential gains from trade are still left unrealized.

Alongside a rise in protectionist tendencies, we are also witnessing how more general liberal values are met with increasing resistance.

Recently, the independent watchdog Freedom House, which analyses developments in global democracy, country by country, warned about a reversal of global freedom. Support for democratic values seems to be on the decline.

Looking ahead, we should expect the Western world to be relatively smaller, both as a share of the world economy and in terms of wielding political and economic influence.

The demographic and economic weight of non-Western countries will gravitate power towards the Southeast. The weight of liberal values may be reduced accordingly.

Against this pessimistic backdrop, what can we do? How can we best ensure that we continue on a path of economic and social development that supports stability, promotes growth and reduces tensions?

First, we must work to strengthen the global system. Only by doing so will the system support stable development also into the future.

As an arena for negotiating new initiatives, the WTO has for a long period failed to deliver. The agreement governing trade in services was concluded in the 1990s.

Meanwhile, the world has changed.

Power has shifted towards new countries. Some of which fail to live up to multilateral standards. In addition, the economy has become more digitalized.

Our concepts of value creation and trade are challenged. In particular, more value is attached to intellectual property. Protection of such immaterial value is a legitimate concern.

The regulatory framework risks falling behind.

Still, I will highlight the WTO as our foremost guarantee for a peaceful handling of the global rebalancing of economic power that is taking place.

Shortcomings should not be used as arguments against the system. Rather, they should spur our efforts to improve it!

Second, we need fair distribution of the gains from trade.

Although markets are international, distribution policies are typically national.

We must acknowledge that national policies need to redistribute the gains from trade to a broader part of our populations. In particular, policies should provide citizens with the means to participate in an ever-changing occupational landscape.

For those who fall behind in the labour market, measures and retraining programs should support their efforts to re-enter. And a sound security net must ensure that all citizens enjoy reasonable living standards.

Otherwise, if national policies fail, people will blame international integration.

Finally, I will stress the importance of a fair and efficient tax system.

A well-functioning tax system constitutes the backbone of a strong and supportive public sector. The state’s capacity to tax is therefore crucial to the sustainability of public finances and the welfare state.

Equally important, support for free and open markets will only be maintained if global companies are taxed where the value is created and the taxation of cross-border activity is fair.

That requires international cooperation. We must stand together to fight international profit shifting and the erosion of our tax bases.

We have come a long way. Recent years have brought major achievements in information sharing through the Common Reporting Standard and Country by Country Reporting. As we all know, information is key to correct taxation.

Furthermore, the international principles for allocating taxing rights between countries are strengthened through the BEPS project on Base Erosion and Profit Shifting, developed by the OECD.

The project brings together more than 115 countries and jurisdictions to tackle the gaps between different tax systems. The aim is to prevent both double taxation and tax avoidance by aggressive tax planning.

Yet, it is a challenge to identify regulation that supports efficiency in the markets of the new economic landscape. The digital economy is truly global, transcending borders easily, and relies on new business models that require us to think in new ways.

I strongly support the efforts on taxation and the digital economy within the OECD’s global framework.

And I am deeply concerned that if we fail in our efforts, our tax base could be severely diminished. That will undermine support for international trade.

Let me sum up:

Maintaining an open world economy is a challenge. It has taken decades of targeted effort and compromises to get where we are today.

Current developments risk undermining this world order.

Technological change and international trade must not be made scapegoats for the failures of domestic policies.

I am a firm believer that international integration and technology hold the potential to provide the world with astonishing welfare gains into a very distant future. Even if others build barriers to economic integration, our economies will gain from continuing on the path of deeper integration.

Increased opposition and decreased influence of the liberal economic order should motivate renewed efforts to build support for free and open markets and societies. This is the time to improve our model, not swap it for a less liberal one.

In fact, we can’t afford not to.

Thank you!