Part 1

Status and challenges

1 Introduction and summary

1.1 The Government’s objective for this white paper

Combating and limiting the scope of economic crime is not only a question of preventing financial loss, but also of protecting our common societal values. In this white paper, the Government will report on the current status and challenges and propose measures that can strengthen joint efforts to prevent and combat economic crime in Norway.

The Hurdal Platform states that the Government will “strengthen the police’s work on money laundering, economic crime, work-related crime, fisheries crime and other related crime, as well as consider increased penalties in these areas and introduce civil-law confiscation.” Combating tax crimes (related to both direct and indirect taxes) and undeclared work are also important priorities.

Economic crime affects our common values. Undeclared work and other tax crimes (related to both direct and indirect taxes) leads to major losses of income for the state and prevents funds from benefiting society. Undeclared work also means that individuals do not earn social security rights such as pensions, sickness benefits, and maternity benefits. In some cases, undeclared work occurs in combination with social security fraud. In such cases, the state pays a benefit to which the person is not entitled, while at the same time losing income in the form of tax and employer’s national insurance contributions. Failure to take action against this type of offence can lead to weakened tax morale and in the long run undermine the welfare state as we know it. Fisheries crime and other forms of illegal resource extraction also negatively affect societal assets.

Similarly, crime such as corruption can hinder economic development and entail increased costs for the authorities and businesses, improper use of public resources, and the risk of incorrect decisions by the authorities.

In addition, economic crime also affects individuals. Work-related crime and online fraud against the elderly are examples of economic crimes that affect vulnerable individuals.

Organised criminals are involved in economic crime to a greater extent than before. The boundaries between purely economic crime and other profit-motivated crime are becoming blurred. If this is not addressed, the consequences can be major financial losses for individuals, companies and society, as well as a loss of trust and security.

The police and the prosecuting authority are key players in both the prevention and combating of economic crime. But these key players alone are not sufficient in the fight against economic crime. Strengthening the work of the police will therefore only be part of the solution. The regulatory agencies also make a significant contribution to limiting the scope of economic crime.1 The same applies to businesses and private individuals, who must also be aware of their role in preventing and detecting crime in the future. Effective protection against economic crime presupposes that this is considered a responsibility for society as a whole.

For the Government, it is an important socio-economic goal to utilise all resources in the most efficient way possible. This requires good and coordinated collaboration, information sharing, and a clear definition of roles and responsibilities at all stages, from crime prevention to securing and collecting confiscated proceeds from crime. Cases should be resolved by the entity that is best suited to the specific case. The police and the prosecuting authority should continue to deal with the most serious economic crimes, where there is a need to use special methods, and where punishment and confiscation are the appropriate response.

It is also a goal of this white paper to organise regulations, systems and enforcement in a way that enables actors to a greater extent to refrain from committing economic crime in the first place. This can be achieved by increasing the likelihood of detection through, for example, more transparency, targeted inspections, and supervision based on risk assessments, and by making it easier to comply with laws and regulations. Put another way: it should be easy to do the right thing and riskier to commit crimes.

A high degree of trust, both in the state and between individual actors, is a great strength for Norway.2 The trust that has been developed over generations contributes to low transaction costs and more efficient operation of the private and public sectors. Trust takes a long time to build, but a short time to tear down. It is therefore important that we safeguard trust in our society. The extent of economic crime and fraud, and the increase in the number of dismissals of these cases that we have seen in recent years, may challenge trust in Norwegian society. This white paper is intended to facilitate further efforts to limit the scope of economic crime and strengthen the fight against it, so that we can maintain trust and security in our society.

Figure 1.1 It is important to safeguard security and trust in society

Photo: courtesy of the National Authority for Investigation and Prosecution of Economic and Environmental Crime (Økokrim)

Since the early 1990s, various governments have presented action plans to counter economic crime. The problem descriptions and proposed measures have been strikingly similar for the last thirty years. The last general action plan in this area was in force from 2011 to 2014. Since then, relevant action plans have had a narrower thematic focus. In 2015, the Solberg Government presented its first Strategy against Work-Related Crime. The strategy was revised and updated in 2017 and 2019 and again in 2021. In 2017, the Strategy for combating money laundering, terrorist financing and the financing of the proliferation of weapons of mass destruction was presented. This was updated in 2020.

The Government believes that there is once again a need to look at economic crime in a comprehensive perspective, with attention to intersectional topics that can strengthen the fight against all forms of economic crime. The topics discussed in this white paper include organisation, competence, prevention, transparency, technology, and the relationship between administrative sanctions and penalties. In addition, the white paper discusses the need for changes to the rules on money laundering and confiscation of proceeds from crime, which are potentially effective tools in the fight against all forms of profit-motivated crime, including organised crime.

The white paper will also facilitate knowledge-based policy development and a more enlightened debate on the prevention and combating of economic crime, as well as contribute to strengthening society’s general awareness of the challenges in question. The white paper will also be a good starting point for further collaboration, both strategically and operationally, between relevant authorities, and for a more coordinated prioritisation in this area.

1.2 Input to the work on the white paper

The white paper has been prepared by the Ministry of Justice and Public Security in consultation with the Ministry of Finance, the Ministry of Trade, Industry and Fisheries, the Ministry of Labour and Social Inclusion, the Ministry of Culture and Equality, and the Ministry of Climate and Environment. During the work, input has been received from the Ministry of Justice and Public Security’s subordinate agencies, and from the aforementioned ministries and their subordinate agencies. Through a press release published on the Government’s website, an announcement was made in the autumn of 2022 for written input from other actors. These were asked to answer four questions:

-

What do you see as the biggest challenges in your field when it comes to the fight against economic crime?

-

What can be done to better prevent economic crime?

-

How can one more effectively deprive criminals of the proceeds of economic crime?

-

How can better cooperation between the public and private sectors be facilitated when it comes to combating economic crime?

Input was received from various actors and organisations, including Finance Norway, the Confederation of Norwegian Enterprise (NHO), the law firm Erling Grimstad, the Norwegian Public Roads Administration, Econa, the Norwegian Economic crime Association (Norsk Økrimforening), Tax Justice Norway, DNB, the Norwegian Union of Journalists, the Brønnøysund Register Centre, Virke, YS, and Helfo, as well as some private individuals. The white paper will not refer to specific input.

In the autumn of 2022 and in the winter and spring of 2023, the Ministry of Justice and Public Security arranged input meetings with both public and private actors who play a key role in the fight against economic crime. Input meetings were held with Norwegian Customs, the Norwegian Tax Administration, the Central Cooperation Forum (DSSF),3 Cooperation against the Black Economy (SMSØ),4 and Finance Norway. In addition, the National Authority for Investigation and Prosecution of Economic and Environmental Crime (hereafter, Økokrim), the Director of Public Prosecutions, the National Criminal Investigation Service (hereafter, Kripos), the National Police Directorate and the police districts have participated in meetings on various parts of the white paper. Academia, including the Norwegian Police University College, has also participated in some of the meetings.

1.3 Topics not included in this report

As stated above, several ministries have been involved in the work on the white paper. Some of the ministries involved also have related work in their fields that must be reconciled with this white paper.

For example, in April 2020, the Ministry of Climate and Environment presented its White paper on environmental crime, which presented a comprehensive policy to strengthen efforts in the environmental field.5 In the same way as economic crime, environmental crime has a great potential for damage. Environmental crime can destroy the natural basis, deplete society’s resources, and damage nature’s ability to grow and self-renew. Environmental crime has common features with economic crime in that the criminal activities affect society’s shared resources, are often profit-motivated, and are difficult to uncover and investigate. The measures in the white paper are being followed up. There is therefore less focus on environmental crime in this white paper, even though it is natural to consider profit-motivated environmental crime in the context of other economic crime.

The Cultural Environment Law Commission was appointed on 22 June 2022, and is working on a draft of a new Cultural Environment Act. The legislative work includes rules on administrative and criminal sanctions for crimes against cultural property, which in many cases will be financially motivated offences.

The Ministry of Culture and Equality (KUD) is responsible for following up the manipulation of sports competitions, the gambling industry, and cultural property crime. These fields are often exploited for laundering the proceeds of organised crime groups. The Ministry of Foreign Affairs has therefore also followed the work on the white paper closely. The Norwegian parliament (the Storting) has adopted a new law on gambling and a new regulation on gambling, both of which entered into force on 1 January 2023. This work is not discussed further in this white paper.

With regard to work-related crime, to which the Government also gives high priority, an Action Plan against Social Dumping and Work-related Crime was presented on 1 October 2022.6 The introduction to this plan emphasises that there is a close connection between social dumping, work-related crime and other forms of economic crime, such as fraud, social security fraud, bankruptcy-related crime, tax crimes (related to both direct and indirect taxes), accounting-related crime, and securities-related crime. The Government chose to concentrate the action plan on topics that affect working life to the greatest extent, with reference to the fact that efforts to combat more purely economic crime would be safeguarded through other processes.

A similar delimitation was made for the work on secure identity and integrated identity management, which is one of the basic prerequisites for effective prevention and combating of work-related crime and other forms of economic crime. The work on secure identity will be followed up as part of further work on the Area Review of ID Administration from 2019.7 For the sake of context, the challenges and measures from the area review that are relevant to the work on preventing and combating economic crime will also be discussed in the white paper (see Chapter 9).

With regard to digital security, the Ministry of Justice and Public Security presented a white paper on National control and digital resilience in December 2022.8 Certain parts of this white paper may be relevant to the fight against economic crime, for example with regard to ownership in real estate, which is discussed in Chapter 9.3.

2 Economic crime: definition, characteristics and consequences

2.1 What is economic crime?

In the Norwegian context and in this white paper, ‘economic crime’ is used as a broad umbrella term for offences that can often be linked to lawful business activity, or business activity that pretends to be legal and whose purpose is to generate financial gain. The offences include fraud, tax crimes (related to both direct and indirect taxes), corruption, embezzlement, accounting violations, wage theft, money laundering, misuse of government support schemes, and social security fraud.

There is no single internationally accepted definition of economic crime. However, there is agreement on three factors9. Economic crime usually takes place in a context that is in principle legitimate and professional. Crime creates, or has the intent to create, financial gain. In addition, the perpetrator is often physically separated from a specific victim.

In the scientific literature, there are different approaches to the concept. One approach focuses on the offender, and deals with what characterises those who commit economic crime. This literature is based on the premise that economic crime is carried out by virtue of the access the criminal has as a result of a position of trust, office or post. Because the crime is committed in a context that is usually legitimate, the breach of trust is the most important characteristic of economic crime.

Another approach to economic crime emphasises the criminal act or offence. Although the offences are different, they have some common denominators beyond the fact that they generate profit. Economic crime often has no specific victim, but instead affects the state’s finances or society’s assets. Examples include tax fraud, social security fraud, and abuse of public support schemes. Some types of economic crime also affect the market. Insider crime, competition crime and securities-related crime are examples of this. Crime also often affects the business sector, through distortion of competition or as corruption, ransomware, and fraud. Private individuals can also be affected by this type of crime, for example through an increase in the price of goods and services in the market.

Offences that are included in the concept of economic crime are discussed in Box 2.1.

Textbox 2.1 Brief information about certain key offences1

-

Fraud: The fraud provision includes deceptively securing assets to which one is not entitled. Fraud can occur through active actions and concealment, can be committed in many different ways, and can affect both the public sector, private enterprises, and private individuals.

-

Accounting violations: Most forms of business activity trigger the accounting obligation for enterprises. Violations of accounting regulations are punishable under the Penal Code (straffeloven), the Accounting Act (regnskapsloven), or the Bookkeeping Act (bokføringsloven). The accounts provide information about the enterprise’s finances and are important for public authorities to be able to check that mandatory statements are submitted and that taxes and duties are correct. Accounting can also show whether transactions are in violation of laws and regulations, and whether they may be punishable.

-

Bankruptcy-related crime: This is a crime that includes several penal provisions, including Chapter 31 of the Penal Code on creditor protection. Accounting violations, illegal withdrawals of assets, transfers to family, failure to submit VAT returns and breach of the duty to keep tax deduction funds separate are matters that are often linked to bankruptcies. The violations are often motivated by poor finances.

-

Tax crimes: Tax crimes (skattesvik and skatteundragelse, in Norwegian), is a term that applies to evading various types of taxes, VAT, excise duties and customs duties. The criminal offence consists of providing incorrect or incomplete information, or completely failing to provide information, when this may lead to a tax advantage.

-

Securities-related crime: Financial instruments can include shares, certificates and bonds, as well as derivatives. The most important violations of the Securities Trading Act are insider trading, prohibition of advice for those in possession of insider information, market manipulation, breach of the duty of confidentiality, and the duty to provide information. In addition, the use of unfair business practices/breaches of good business practice, as well as investment services without authorisation, are relevant infringements.

-

Competition crime: This type of act involves violations of the Competition Act, and includes abuse of a dominant position and various forms of illegal cooperation such as price fixing, tender cooperation, market sharing, and information exchanges.

-

Corruption: The concept of corruption in criminal law includes bribing or accepting bribes in the form of money, gifts or services. The term ‘improper advantage’ is the Penal Code’s term for the bribe. In order to be punishable, the act must be clearly reprehensible. Factors in the assessment are the sum of the financial advantage, the degree of transparency and the position of the person in question.

-

Breach of financial trust: Breach of financial trust is characterised by the breach of trust committed by someone who, in his or her role of managing or supervising certain interests, such as the general manager, abuses the role to act against the interests that the person in question is supposed to safeguard, and where the offence is committed to obtain an advantage for oneself or others. Embezzlement is a related offence, but does not require one to play a special role.

-

Money laundering: Money laundering is actions that in various ways help to secure the proceeds of criminal acts by concealing where they go or who has control over them, or that conceal the illegal origin of income or assets. Money laundering is necessary to enjoy the benefits of unlawful proceeds, and the purpose is to integrate the proceeds into the legal economy. Money laundering can be carried out for others or to ensure the proceeds of one’s own criminal acts (self-laundering).

1 The list is not exhaustive. Further descriptions of various forms of economic crime can be found, for example, on Økokrim’s website.

Different types of economic crime can overlap and be integrated into each other. Other collective terms are also used for offences that overlap wholly or partly with the umbrella term economic crime (see Box 2.2).

Textbox 2.2 Other collective terms

Work-related crime (a-krim, in Norwegian) is a collective term for acts that violate Norwegian laws on wages and working conditions, social security, and taxes and duties, often carried out in an organised manner, which exploit workers, have a distorting effect on competition, and undermine the structure of society. At the same time, work-related crime is an example of the complexity of economic crime, as it can often consist of tax crime, accounting-related crime, money laundering, racketeering, and fraud. In addition, it may include forms of crime that fall outside the concept of economic crime, such as human trafficking.

Fisheries crime are various offences committed throughout the value chain in the fishing industry from catch to landing, processing, transport, export, and sale. Fisheries crime is primarily economic crime, but also has interfaces with work-related crime and environmental crime. Because the fishing takes place at sea where the right to inspect is limited, the offences are often difficult to detect and investigate. In addition, fisheries crime often crosses borders.

Cultural heritage crime is an act that violates legal rules that protect cultural monuments and cultural environments. The crime is multifaceted and can be committed due to ignorance or carelessness, or be deliberate criminal acts. Interventions in automatically protected cultural monuments are often financially motivated, for example where someone deliberately ploughs areas with automatically protected cultural monuments, or to demolish or rebuild buildings that are protected under the Cultural Heritage Act. Illicit trade in cultural artefacts is an example of economic crime that is often transnational and organised.

2.2 Profit-motivated crime, organised crime, and economic crime

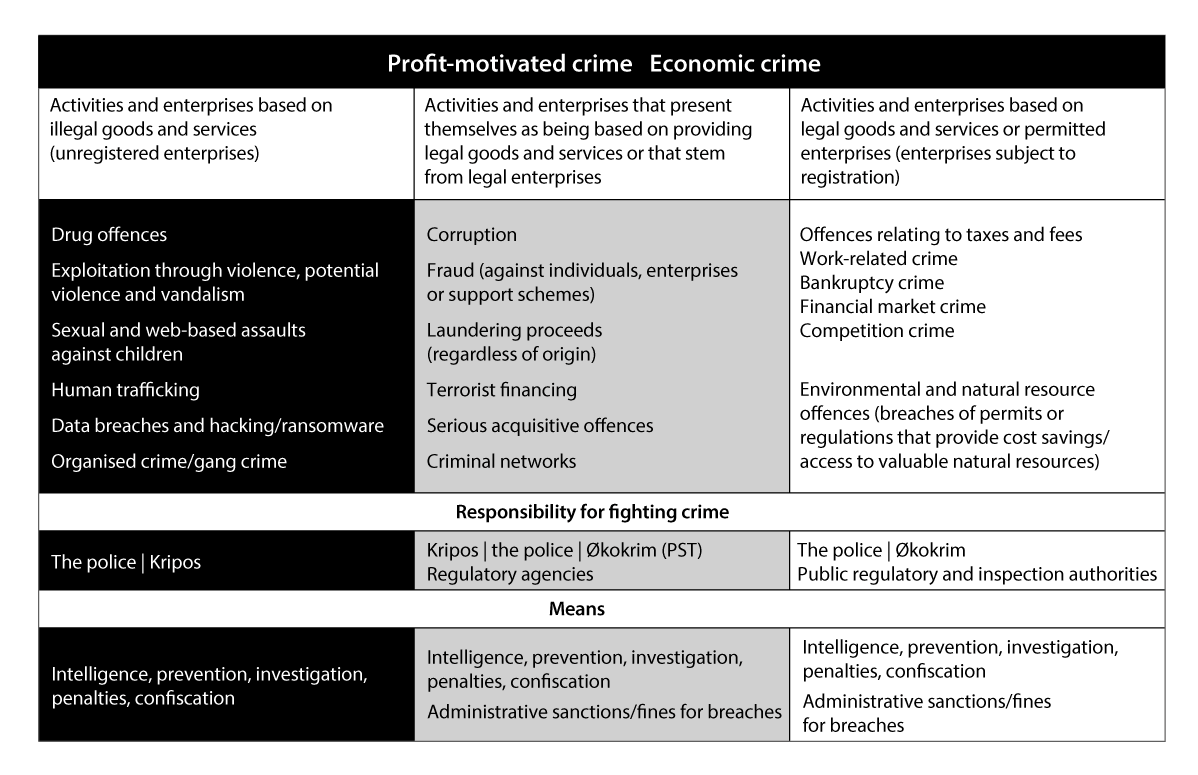

Profit-motivated crime is a broad term that can basically be used for all types of crime that generate profit, including economic crime, as defined in Chapter 2.1. However, it may be appropriate to draw a distinction between economic crime and other profit-motivated crime based on the distinction between whether the activity is based on legal or illegal activity, goods or services. In the following, economic crime and other profit-motivated crime are discussed on the basis of this distinction. Box 2.3 describes the difference and how responsibility for follow-up by the police is divided between the special agencies Økokrim and Kripos.

Textbox 2.3 Operationalisation of police work against profit-motivated and economic crime

Figure 2.1

Source: Økokrim

The different categories overlap and have been developed to help in the organisation of crime prevention efforts. They can also be important when prioritising various risks.

Both economic crime and other profit-motivated crime are often committed by criminal networks and are thus also considered organised crime. The Penal Code is based on a broad definition of organised crime: all crime can be organised as long as it involves a certain pattern of cooperation between three or more individuals, and the sentencing range for the offence is a minimum of three years.10 The number of registered cases of organised crime has fallen over time and is low. However, it is difficult to quantify the extent of organised crime because there are no separate statistical groups for this in the police’s criminal case database.

It can often be challenging to distinguish clearly between profit-motivated, financial, and organised crime. The offences often overlap, and organised crime can often take place in apparently legal enterprises, with complex company structures. Crime is often camouflaged through document forgery, the use of intermediaries (‘straw men’) in formal roles, the obscuring of transaction links or secrecy jurisdictions (tax havens). In addition, multiple offenders are often also responsible for laundering profits from, among other things, drug offences.11

When there is a correlation between financial and other profit-motivated crime, Økokrim and Kripos cooperate in the fight against it. The police districts, in their input to this white paper, have expressed the view that there is a great need for collaboration between groups that investigate economic crime and groups that investigate other profit-motivated and organised crime. To combat this crime effectively, it is necessary to exchange methods and expertise among the various groups.

Although there is an obvious need for collaboration between the various groups to achieve effective crime combating, this white paper focuses mainly on economic crime in the traditional sense. This is based on the need to highlight certain specific issues that apply to this field; see Box 5.1 below.

However, several of the measures proposed will also contribute to strengthening efforts against other profit-motivated and organised crime as well. This applies in particular to measures relating to capacity, as well as measures related to money laundering and confiscation in Chapters 12 and 13.

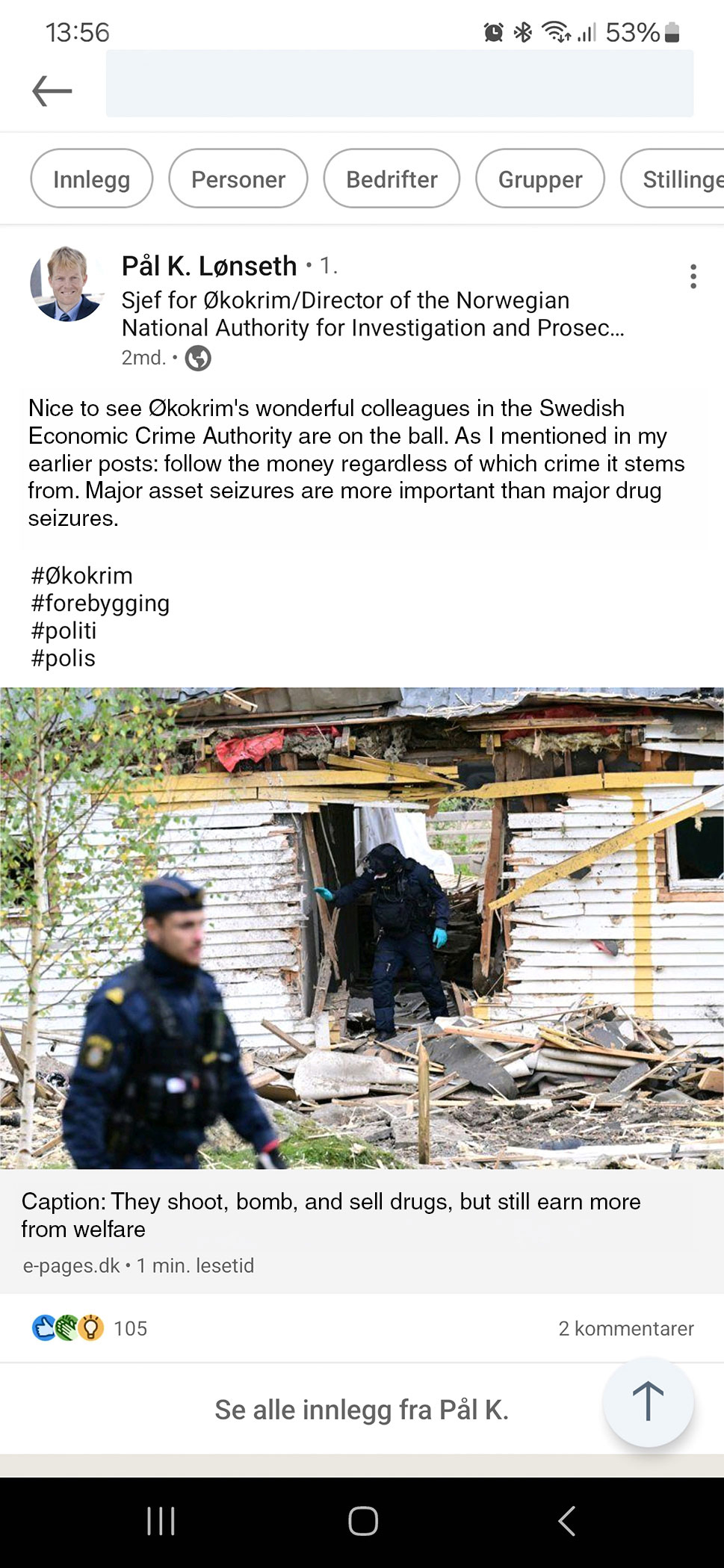

Figure 2.2 Post by Økokrim Director Pål K. Lønseth on LinkedIn.

Source: LinkedIn, screenshot used with the permission of Pål K. Lønseth

2.3 Who commits economic crime?

2.3.1 Wealthy middle-aged men

There are well-documented links between crime and various types of exclusion: research shows that low income, unemployment, and low education normally increase the risk of committing crime.12 This pattern is not true when it comes to economic crime.13 People who commit economic crime are a more complex group. However, there are several characteristics that are repeatedly seen. About 70 to 80 per cent of the perpetrators are men. The majority belong to the ethnic majority in the country in which they live. The average age is between 40 and 45 years. Of those convicted of economic crime, a small proportion of career criminals commit multiple offences. A high socioeconomic status is also a characteristic.

Few studies of economic crime have been conducted in Norway. A study of 405 Norwegian judgments showed that the convicted person had an average age of 44 years when the offence was committed.14 Those who received the longest sentences had highly trusted positions in the company (CEO and director). Most of them worked in the private sector. Just over 75 per cent committed crimes for personal gain, while the rest were convicted of offences committed by the enterprise. The employer was the victim of crime in 28 per cent of the cases, followed by the Tax Administration and the enterprise’s customers with 21 and 17 per cent of the cases, respectively.

In addition, research has pointed to factors such as motivation, opportunity, and personal willingness as prerequisites for committing economic crime. The motive may, for example, be to avoid a financial crisis, while room for opportunity is both about the opportunity to commit and to conceal the criminal acts.15

2.3.2 Professional facilitators

Access to or the ability to influence professional facilitators, such as accountants and lawyers, is often a prerequisite for certain types of economic crime to succeed and not be uncovered by the police and regulatory agencies. In several cases, there are close ties between the professional actors and key players in criminal circles. For example, the Supervisory Council for Legal Practice has uncovered several cases where lawyers assist with loan mediation and settlement without being able to document particular knowledge of the reality behind the loan agreements, and cases where legal services are used to conceal beneficial ownership in a company or in real estate.

Some lawyers have also facilitated economic crime by using client accounts, e.g. to evade creditor debt and for fraud and money laundering. The Supervisory Board has experienced several cases where there is reason to suspect that lawyers deliberately assist criminal actors/networks in moving money as part of a money laundering process.16

2.3.3 Criminal “service providers”

When criminal specialists sell their services to other criminals, this is referred to as Crime as a Service (Caas). Caas has become more prevalent among criminal networks and organised criminals; however, the extent is unknown. This business model professionalises criminal activity through criminals outsourcing assignments to actors who specialise in a criminal service, or who have special expertise related to crime. The criminal specialists fulfil functions such as money changers, money collectors, document forgers, couriers, and providers of cybercriminal services. Consequently, the network structures are becoming increasingly more complex.17

Norway has several actors who act as key money launderers for organised crime networks, among other things. Some of these use so-called “money mules” who play a central role in moving proceeds. Money mules are individuals who, in return for payment, assist criminals by receiving money digitally or in cash from one person and transferring it on to another.18 Money mules have also become a “consumer service” for criminal networks. Some of the criminal masterminds have recruited vulnerable people, and in several cases people have also been threatened and forced into the role of money mule.19

Figure 2.3 Screenshot of Økokrim’s awareness-raising campaign about money mules on Instagram

Source: Økokrim

Figure 2.4 Screenshot of Økokrim’s awareness-raising campaign about money mules on Instagram

Source: Økokrim

2.4 Characteristics of economic crime

2.4.1 Dynamic

Economic crime is dynamic, and criminals have the ability to adapt. Among other things, the OECD has pointed out an increasing risk of criminal actors entering legal businesses.20 As previously mentioned, there is an important interface between economic crime and other profit-motivated and organised crime. A trend towards multi-criminal actors who commit several types of offences in several different industries or sectors entails an expansion of the types and scope of crime.

Economic crime is also affected by geopolitical uncertainty, high inflation and a high degree of uncertainty in the markets. Lower margins in the business sector can affect both the scope and the method. This, in turn, can create pressure in some industries and contribute to more players being driven towards tax crime and other forms of economic crime in order to ensure profitability in business operations.

Digitalisation and globalisation create new opportunities to camouflage crime through less traceability. Opportunities for the preparation of fictitious documentation are an additional dimension in global crime. These aspects help make it possible to carry out the crime on a larger scale and from a distance, with constant changes in methods, resulting in a lower risk of detection.

2.4.2 Crossing national borders

Both globalisation and digitalisation pave the way for cross-border transactions and cross-border activities. This can present challenges to the control agencies and the police in obtaining the necessary information. Effective combating of illegal cross-border transactions requires cooperation with the authorities of other countries and foreign payment services.

There are still authorities in some countries that provide little or no assistance, or with which it is difficult to cooperate for various reasons (see Chapter 14 on international cooperation).

Increased attention to the cross-border movement of goods is also important for the fight against economic crime. Norwegian Customs’ inspection activities uncover many factors linked to organised crime and the black economy, such as smuggling of food products, counterfeit brands, easily marketable and highly taxed goods such as spirits and cigarettes, and ordinary trade goods, as well as currency smuggling. A case uncovered by Norwegian Customs is often linked to a case of economic crime.

The EU expansion to countries in Central and Eastern Europe has led to considerable labour migration to Norway. Many foreign workers work in the building and construction sector, the fishing industry, agriculture, or in cleaning and other service industries.21 Although labour exploitation and other work-related crime in these industries is not necessarily linked to labour immigration, the police and regulatory agencies have found that labour immigrants have a higher risk of being subjected to poor working conditions. Various forms of exploitation of foreign workers and evasion of taxes and duties are the most widespread forms of work-related crime. Other typical forms of work-related crime are fraud, including social security fraud, use of fictitious information, bankruptcy-related crime, and evasion of employer responsibilities. In many cases, the illegal activities have international ramifications, and investigations require cooperation with authorities in other countries. The same applies to the collection of tax claims and other claims abroad.

2.4.3 New technology creates new risks

The digitalisation of society has led to simplification and better compliance in several areas. At the same time, digitalisation represents increased opportunities for committing crime. National borders are being erased for criminal actors – but not for the police – and profit-driven criminals and other criminal actors have been given greater room for manoeuvre than before.

Increased digitalisation in public administration also provides new opportunities for various forms of social security fraud. Digital solutions in the Norwegian Labour and Welfare Administration can, among other things, increase the risk of document fraud, ID fraud, and fraud involving electronic signatures, and it can be difficult to find out who has actually applied for a benefit. Furthermore, increased use of digital follow-up makes it more difficult to control residence requirements related to certain benefits paid by the Norwegian Labour and Welfare Administration.

Digitalisation in the business world makes it possible for online companies to achieve significant dominance, as well as to undermine competition in new ways. The development of digital currency, such as Bitcoin and other cryptocurrencies, has allowed criminals to use unregistered currency exchangers and mixers as a money laundering means to anonymise transactions in an attempt to avoid detection by the authorities.22 Cryptocurrency is used as a means of payment for fraud and ransomware, and to fund criminal activities both in Norway and abroad. Digital extortion in the form of ransomware is discussed in more detail in Box 2.4.

Textbox 2.4 Ransomware

Ransomware can cause major financial losses, while at the same time there is the opportunity of high profits and little risk of identification and prosecution. This is also related to the fact that the criminals are located, and commit the crime from, abroad.

In 2019, Norsk Hydro was the victim of a ransomware attack. The total costs resulting from the attack are estimated at NOK 650–750 million.1 The organised criminals behind the attack were suspected of having perpetrated 1,800 attacks in a total of 71 countries, using the same ransomware, LockerGoga.

In 2021, the White House initiated an international collaboration to combat ransomware, the International Counter Ransomware Initiative (CRI). A total of 48 countries, including Norway, the EU and Interpol, participate in the collaboration, which takes place at both a policy and an operational level. The cooperation has a particular focus on countering increasingly sophisticated ransomware attacks, sharing information about good cyber security, and ensuring that the CRI countries stand together to fight cybercriminals.

1 Hydro (2019).

The National Audit Office of Norway’s study of the police’s efforts to combat crime using ICT from 2 February 2021 concludes that the police’s ability to uncover and solve digital crime has clear weaknesses that, when seen together, are serious.23 Among other things, the report finds that the police lack the capacity to address the development in financial cybercrime.

2.4.4 ID fraud facilitates economic crime

ID fraud means the use of false or forged ID documents or copies and photos of such documents, as well as the use of other people’s genuine ID documents and wrongfully sent genuine ID documents. ID fraud also includes the misuse of identity without the presentation of ID proof.24

In addition, the term also encompasses the misuse of certificates, such as the misuse or falsification of birth certificates, citizenship certificates, and marriage certificates.

ID fraud poses a security threat and is often included in cross-border crime, such as human smuggling and human trafficking, as well as the smuggling of drugs, weapons, and stolen vehicles. Europol’s threat assessment highlights ID misuse as one of the most serious criminal threats facing the EU.25 There is considerable international attention to the need to limit the scope for criminal activity by combating ID misuse, both as an underlying facilitator of crime and as a tool in its actual execution.

Misuse of identification numbers is also increasingly taking place digitally. In addition, ID fraud facilitates economic crime, corruption, crimes for profit, and terrorism. ID fraud is also a factor in fraud cases. A false or stolen identity is used to build trust and scam money, create a digital identity in someone else’s name, or to take out a loan using a family member or someone else’s Bank ID, etc.

2.4.5 Hidden ownership may conceal economic crime

The ability to conceal ownership or control behind a series of companies, often across national borders, makes it more difficult to prevent, uncover, and investigate economic crimes such as tax crimes (related to both direct and indirect taxes), money laundering, corruption, and insider trading. These often involve the establishment or use of services in states that allow the identity of an indirect owner or party that indirectly controls a company to remain secret, for example through the use of trusts, as well as the use of financial instruments.

Concealed ownership, secrecy, complicated company structures and indirect transactions via intermediaries (‘straw men’) help to make money laundering in the real estate market possible. According to Transparency International’s report Who Owns Oslo from 2021, over 500 properties in Aker Brygge, Tjuvholmen, Sørenga, and Bjørvika are owned by companies registered in so-called tax havens.26 While it cannot be established that the money used to acquire the properties are proceeds from crime, the findings do give an indication of the risk of money laundering.

The interest group Tax Justice Norway has discussed these issues for many years, most recently in the latest edition of the book Skjult – skatteparadis, kapitalflukt og hemmelighold [Hidden – Tax Havens, Capital Flight and Secrecy] from January 2023. Among other things, the book has a separate chapter on the status of relevant measures for more transparency concerning ownership, including country-by-country reporting and a register of beneficial ownership.

Another way to conceal ownership or proceeds of crime is through investing in property abroad. In the so-called “Dubai leaks”, it has been revealed that several Norwegians who have committed crimes in Norway own property in Dubai.27

In fisheries management, it can also be a challenge to uncover any hidden agreements indicating that someone other than the stated majority owner is the beneficial owner, has a financial interest in the operation that corresponds to the ownership interest, and exercises real control over companies that own fishing vessels, in violation of Section 6 of the Partnership Act.

2.4.6 War and conflict affect the extent of economic crime

The world today is characterised by global great power rivalry and competition between democracies and authoritarian regimes. In Europe, the Putin regime, through its attack on Ukraine in violation of international law, has caused the most serious security policy situation since World War II.

Some state actors use a wide range of instruments to achieve their goals, and there are not always clear distinctions between state, private, and criminal enterprises. Different economic means can be part of so-called hybrid threats.28

War and conflict provide greater room for manoeuvre for criminal networks to expand their activities, including in the area of economic crime. Among other things, the risk of corruption is expected to increase.29 War also increases the risk of looting and the illegal trade in cultural monuments. At the same time, refugees from the war find themselves in a vulnerable situation for human trafficking and work-related crime. A further element is the possibility of various forms of fraud through false fundraising campaigns and the like. Criminal networks both in Ukraine and Russia are also known for their involvement in various forms of cybercrime.

2.5 Consequences: eroded trust and security and financial loss

Economic crime can have serious consequences in the form of major financial losses for individual victims, companies, and society as a whole. The consequences may vary depending on the scope and type of crime committed.

Economic crime can contribute to greater inequality and injustice. This happens, among other things, because crime makes markets less well-functioning and harms competition. Businesses that do not pay taxes and duties can offer goods and services at a lower price than others. This, in turn, has negative consequences for the organised part of business and working life. At the same time, non-payment of taxes and duties will result in lower revenues for the state.

Economic crime can also have negative consequences for the reputation of the person affected. A company that is subjected to a major fraud or data attack may appear poorly prepared and less professional. Crime can thus erode trust and credibility with customers, partners, and investors. Eroded trust between business and industry participants may also increase transaction costs and reduce the efficiency of the economy because market participants in general, and creditors in particular, must devote more resources to ensuring that their requirements are met.

Those who are victims of economic crime lose money and assets. Private individuals can lose large sums of money to fraud and find it unsafe to communicate digitally. Companies can also lose large sums. In some cases, such as in bankruptcy-related crimes, creditors suffer a financial loss. This may mean that employees do not receive pay for work performed, or that the Norwegian Labour and Welfare Administration’s (here after referred to as NAV) Wage Guarantee must cover pay expenses.

In addition, economic crime leads to increased costs and reduced productivity for the public sector and for the business sector, because time and resources must be spent on safeguarding against and preventing economic crime. This in turn can contribute to lower economic growth and value creation. Economic crime can also mean that some actors unjustly enrich themselves at the expense of others, for example through the exploitation of labour. This may, for example, involve a combination of undeclared work and social security fraud, in that the employer forces or exerts pressure on the employee to apply for benefits.

Eroded trust is a particularly serious consequence of economic crime. If the authorities lack the ability to react to economic crime, it may lead to an impression amongst the general public that economic crime is widespread and that criminals are getting away with their crimes. This can lead to a loss of confidence in the authorities’ ability to deal with crime. Compliance with tax rules illustrates the importance of trust. In areas where there is no third-party reporting, i.e. where the employer, banks, or other institutions report directly to the Tax Administration, the authorities are largely dependent on voluntary compliance. Trust in the authorities contributes to higher voluntary compliance. Trust takes a long time to build, and is easy to lose. Eroded trust means that the authorities have to use controls and harsh measures to a greater extent to increase compliance, which is far more resource-intensive and less effective than voluntary compliance. Ultimately, this can weaken the political stability of a country.

In the financial sector, the consequences of eroded confidence are illustrated in a different way. Economic crime against banks, credit systems, and the securities market affects systems in which the population must have confidence in order for them to function. If people lose confidence in the financial market, financial institutions, and banks, it can lead to them staying away from investments and savings, and to so-called “bank runs” which can in turn weaken the country’s economy.

3 The scale of economic crime

3.1 Registered crime and unreported figures

The scale of economic crime is the total number of offences reported to the police and the number of unreported crimes.30

For registered crime, with the exception of 2022, there has been a decline in the number of offences reported to the police for many years. At the same time, the proportion of cases that have been dropped has been made has increased considerably. The composition of economic crime has changed considerably, and fraud accounts for an increasing share of the offences reported to the police.

When it comes to unreported figures, we generally have a better overview of economic crime directed at businesses, municipalities, and private individuals than in cases where there is no specific victim. The National Safety Survey 2020 and 2022 and the National Survey on the Scope of Economic crime Aimed at Businesses and Municipalities together provide a better knowledge base on unreported figures on economic crimes against specific victims than we have had previously.31

There is still a need for more knowledge and research on the scale of crimes without a specific victim.

3.2 The scale and development of registered crime

The statistics on reported offences show that there have been fewer cases, while the police are also making more decisions not to prosecute cases. Fraud accounts for an increasing share of registered economic crime.

3.2.1 Fewer economic crimes reported

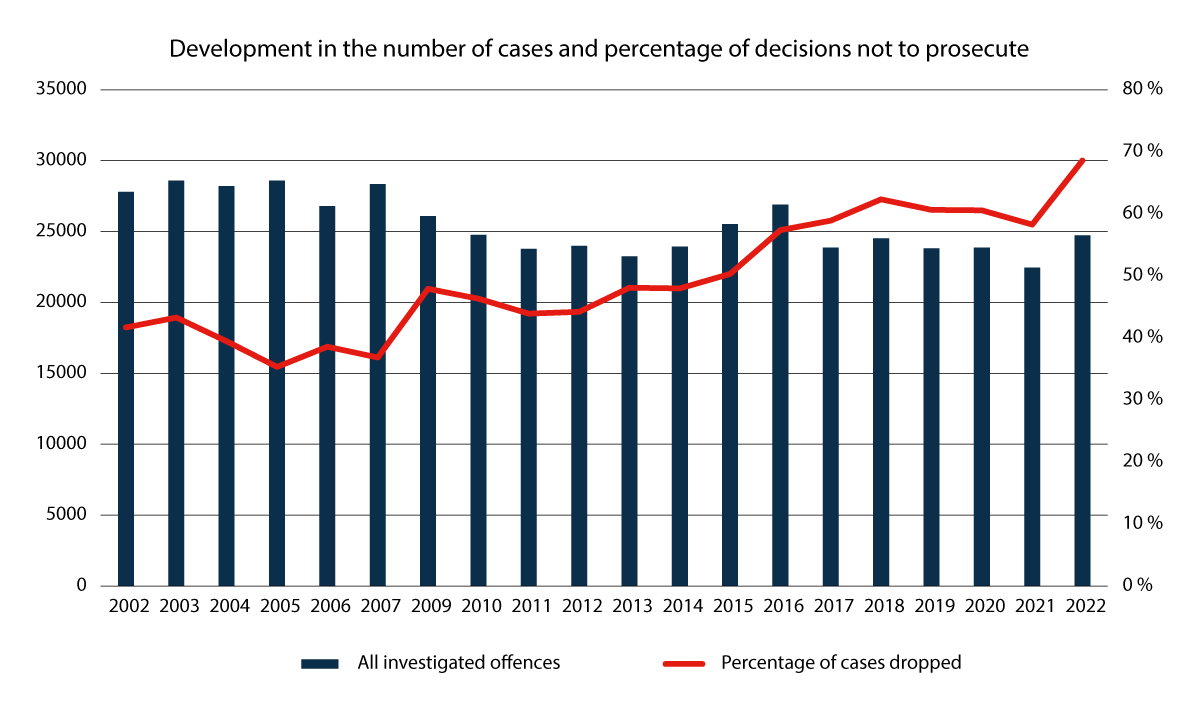

As shown in figure 3.1, there has been a decline in the number of registered cases over the past 20 years. The decline has been mostly stable, but with some variation. Despite an increase from 2021 to 2022, the trend over the past five years is fewer cases. There were about 2,100 fewer cases in 2022 than in 2016.

Figure 3.1 Development in the number of reported cases of economic crime and the proportion that are discontinued.1

1 The table does not include figures for 2008. This is due to a single fraud case in Oslo that alone caused 8,000 reports, which would have made it more difficult to compare the development in the number of cases in other years.

Source: Statistics Norway 2023, table 09405: Offences investigated, by statistical variable, type of offence, police decision and year

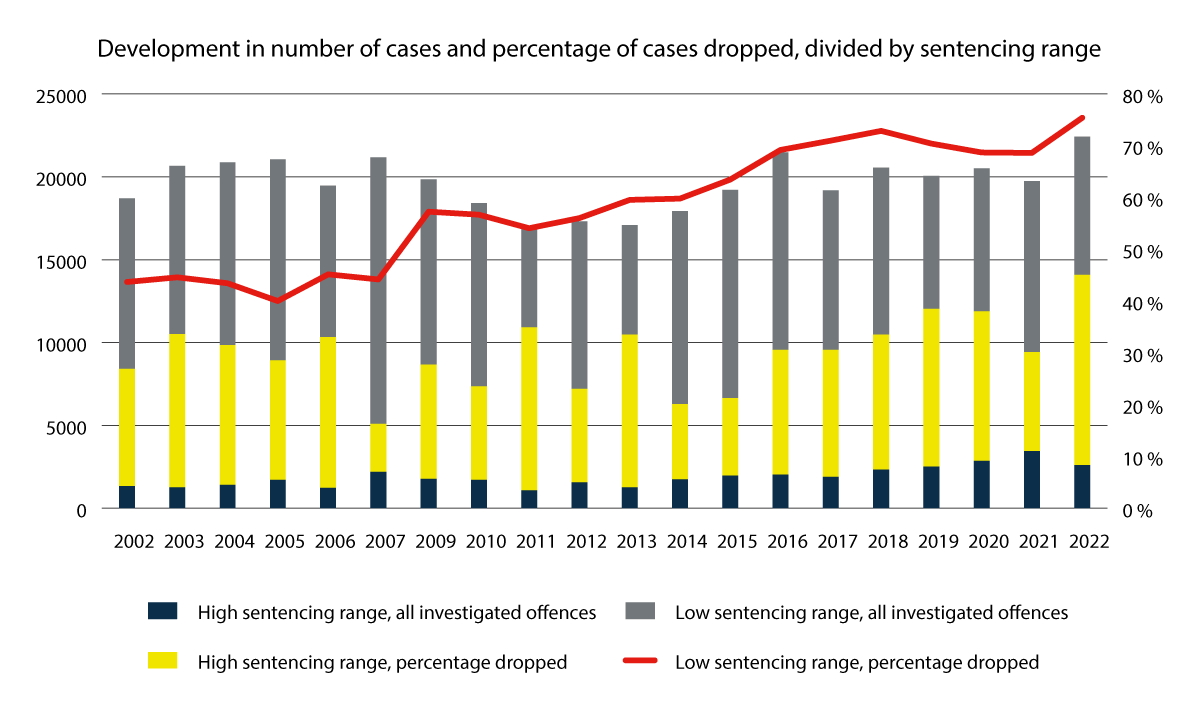

Figure 3.2 Development in the number of cases of economic crime reported to the police and the proportion of cases discontinued, by maximum sentence over / under 6 years

Source: Statistics Norway 2023, table 09405: Offences investigated, by statistical variable, type of offence, police decision and year

Figure 3.2 shows that the vast majority of cases have a maximum sentence of less than six years. Following several years that saw a decline in cases with a low penalty, the number of cases increased from 2021 to 2022.32 The number of cases with a high maximum sentence was relatively stable between 2002 and 2012. Since 2012, there have been about three times as many cases with a maximum sentence of more than six years.

A review of the figures from Statistics Norway shows that there has been a decrease in virtually all types of economic crime during the period. Overall, the decrease in the period is of about 3,000 cases. Since 2016, there have been about 2,100 fewer cases.

The change in the number of reported cases by the regulatory agencies is related to the use of administrative sanctions, changes in the agencies’ reporting instructions, and the division of labour between the police and other agencies more generally. This is discussed in more detail in Chapter 11.

Within the different categories of cases, there is a wide range of different types of cases. Several of the cases in the categories of receiving proceeds of crime, money laundering, corruption, and taxes and duties are large, serious, and complex. Other cases, such as violation of the provision on minor fraud in Section 373 of the Penal Code, concern lower amounts of money and may be more comparable to minor theft and less complex cases of profit-motivated crime.

Over the past five years, there has been a decline in almost all case categories. The category of receiving proceeds and money laundering has fallen by just over 50 per cent. This decrease is mainly due to fewer cases of receiving proceeds of crime. Since 2012, there has been an average of 2,860 cases a year, but a further decrease of about 1,000 cases in 2021 than in 2015. The number of cases of money laundering has also fallen by over fifty per cent. Since 2012, there has been an average of 93 cases annually. The number of cases involving embezzlement has fallen by 47 per cent. In the last decade, there has been an average of 1,140 cases, and the trend is declining.

Fraud is the only category that has increased significantly. There were 19,100 cases in 2022. The number has increased by about 7,200 cases since 2002. The increase applies in particular to aggravated fraud. The number of cases of aggravated fraud has increased sharply from just under 700 in 2011 to 2,700 in 2021. However, the number of aggravated fraud cases fell by over 700 from 2021 to 2022. Ordinary fraud accounts for the majority of cases, about 75–80 per cent, depending on the year. Since fraud accounts for such a large majority of cases, it is dealt with separately in Chapter 3.3.

3.2.2 Increased share of cases that are dropped

The proportion of cases that are dropped has also increased, especially since 2016. This is due to a higher proportion of dropped cases with a low sentencing range. Since 2016, an average of 71 per cent of all cases with a maximum sentence of less than six years have been dropped. Correspondingly, an average of 35 per cent of cases with a high maximum sentence were dropped. From 2021 to 2022, the proportion of cases with a high maximum sentence that were dropped increased from 30 to 45 per cent.

Between 2002 and 2022, the proportion of dropped cases increased in 12 of 17 categories. The increase applies in particular to fraud. On average, 62 per cent of all fraud cases have been dropped during the period. This implies an increase of 26 percentage points. There is great variation between different types of fraud. For aggravated fraud and ordinary and minor fraud, the share of dropped cases is on average 30 and 67 per cent, respectively. However, the proportion of aggravated fraud cases dropped increased from 30 to 48 per cent between 2021 and 2022, despite a sharp decline in the number of cases. The proportion of fraud cases that were dropped has never been higher than in 2022.

Aside from fraud, the share of cases of economic crime that are dropped is on average 31 per cent for the entire period. The tendency is towards a higher proportion of decisions not to prosecute: Since 2016, the proportion of dropped cases has increased from 30 to 44 per cent.

In Statistics Norway’s figures, the lowest proportions of dropped cases appear for customs duties, taxes and excise duties, and accounting violations. However, there are weaknesses in the figures that mean that the proportion of dropped cases may be artificially low, for example within the cases that the Tax Administration has reported. This is discussed in Chapter 15.

Over the past five years, the police have dropped an average of 62 per cent of all cases of economic crime. From 2021 to 2022, the proportion of dropped cases increased from 58 to 69 per cent. Decisions not to prosecute can be registered in three ways: due to a lack of information about the perpetrator, a lack of evidence, or a lack of case processing capacity. The proportion of cases dropped due to a lack of case processing capacity has increased considerably over the past 20 years. There has been a particular increase in the last five years. In 2022, one in three cases were dropped due to a lack of case processing capacity.

Fraud also stands out when it comes to grounds for dropping cases, and is to a greater extent dropped than other cases due to a lack of case processing capacity. In 2016, 17 per cent of all fraud cases were dropped on these grounds. The corresponding figure for 2022 was 35 per cent.

Decisions not to prosecute made for other types of cases than fraud are primarily due to a lack of evidence. Between 2016 and 2022, on average, slightly more than one in five cases were dropped due to a lack of case processing capacity. In the same period, an average of 66 per cent were dropped due to lack of evidence.

3.3 More aggravated fraud cases

The composition of registered economic crime has changed greatly over the past 20 years. Today, most investigated offences within economic crime are fraud cases. In 2002, fraud accounted for 43 per cent of the investigated cases, followed by racketeering and money laundering, and tax offences, at 19 and 18 per cent respectively. In 2022, fraud accounted for 79 per cent of all cases, while theft and money laundering accounted for nine per cent. All other case categories accounted for less than five per cent of the total caseload.

The National Security Survey 2020 and 2022 shows a clear correlation between the amount of the financial loss and whether the offence was reported. The statistics on reported fraud reflect this. The number of minor fraud cases has remained relatively stable at just over 1,000 offences reported to the police since 2004. The number of “ordinary” fraud cases has increased by 27 per cent in the period, and there have been over 10,000 police reports a year since 2015. It is particularly worrying that the number of aggravated fraud cases has increased sharply. Since 2011, the number of aggravates fraud cases has almost tripled.

Analyses show that the increase in the number of reported fraud cases is due to more private individuals reporting fraud, while enterprises and other legal entities report far fewer frauds than before.33 An analysis of victims of all offences from 2019 showed that one in ten victims who were private individuals had been exposed to fraud.

Digital fraud is a challenge in today’s society, and is discussed in a report from Økokrim from June 2023.34 Økokrim estimates that losses in Norway related to fraud totalled more than half a billion kroner in 2022. The majority of fraud offences result in relatively small financial losses for the individual affected. However, in the case of investment fraud and romance fraud, the financial losses for the victims can be significant.

DNB reports that it detects and prevents the vast majority of attempts at fraud against private individuals through the bank’s systems. The bank states that the fraud attempts made against DNB and its customers totalled NOK 1,811 million in 2023. This is an increase of 45 per cent from 2022. The bank hindered NOK 1543 million in fraud.35

Fraud affecting Norwegian citizens and businesses is committed by criminal networks both in Norway and abroad. The profit for these is several hundred million kroner. The networks often appear to be professional and consist of a number of people with clearly defined roles and tasks. Some criminal networks run their own call centres facilitating contact with the victims and create false companies and websites that give a legitimate impression.36

Figure 3.3 Bank card purchases

Photo: Shutterstock

3.4 A large increase in suspicious transaction reports

In recent years, the number of suspicious transaction reports sent by entities with a reporting duty under the Norwegian Money Laundering Act (hvitvaskingsloven) to the Norwegian Financial Intelligence Unit (FIU) of Økokrim has increased significantly.37 The FIU’s annual report for 2022 shows that the number of suspicious transaction reports (so-called STRs) has doubled over the past five years.38 From 2021 to 2023, reporting increased by about 44 per cent.

The main reason is increased investment and expertise among those with a reporting obligation and, not least, an increase in the number of unique reporting entities. There is also a clear increase in STRs for some crime areas, including work-related crime and internet-related child abuse. However, fraud and money mule activities are the areas the FIU has received the most reports on, with a significant increase of about 100 per cent from 2020 to 2023.

In addition, in 2023, the FIU received just over 22,000 reports from similar authorities in other countries. This is also a significant increase from previous years. The increase in the number of reports from abroad is mainly due to automation of the processes in different EU and EEA countries.

3.5 Confiscation figures have remained constant for 25 years

In country evaluations by the Financial Action Task Force (FATF) in both 2014 and 2019, Norway was criticised for the fact that the confiscation figures of proceeds from crime were too weak.39 Despite attention to the importance of confiscation both nationally and internationally, confiscation figures for the police are still relatively constant.

In June 2023, the Norwegian Police University College (PHS) published the report Confiscation: An Initiative Without Results? What Works and What Doesn’t?40 The report is an empirical study of confiscation in Norway, and is based on the National Police Directorate’s (POD) and the Tax Administration at the Norwegian National Collection Agency’s (SI) own statistics on confiscation, a survey of the police districts’ confiscation specialists, and a survey of the first cohort that completed the newly established web-based confiscation study at PHS.

In the introduction to the report, it is stated that the confiscation figures for the police are at about the same level today as they were 25 years ago. It is difficult to produce precise statistics on the sum of proceeds that are actually collected from criminals. An overview of the application of the Penal Code’s rules on confiscation provides only part of the picture.

The regulatory agencies also establish claims against offenders, and the Tax Administration’s collection of confiscation claims, and other types of claims is also important for depriving offenders of their assets. In criminal cases, it is also not uncommon for the victim to have suffered a loss and to claim compensation. The report has therefore obtained various figures, including an overview showing developments in both confiscation and compensation (see Table 3.1). The table is illustrative of the conclusion that the figures have been fairly constant over several years.

Table 3.1 Confiscation and compensation. Amounts in nominal NOK

|

Amount in NOK million |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

Total |

|---|---|---|---|---|---|---|---|---|---|

|

Imposed confiscation amount |

326 |

165 |

197 |

109 |

198 |

983 |

184 |

178 |

2 340 |

|

Awarded damages |

321 |

287 |

401 |

406 |

386 |

351 |

362 |

307 |

2 821 |

|

Total confiscation and compensation claims |

647 |

452 |

598 |

515 |

584 |

1 334 |

546 |

485 |

5 161 |

Source: PHS (2023)

3.6 The police’s goal attainment

The figures above show that the police discontinue many cases of economic crime. This normally means that cases are not solved.

It may be appropriate to question whether the police are using resources efficiently enough and achieving the desired results. These matters are difficult to measure, but also to set target figures for. One can count cases, convictions, discontinuances, acquittals, fines, and dismissals of prosecution. It is also possible to count searches, detentions, extradition orders, and interrogations. Such an analysis must take into account differences between cases in terms of scale and time required. Similarly, there is a big difference between a short and simple interrogation and a lengthy and extensive interrogation. These natural differences mean that counts and comparisons have limitations.

One must also consider that the numbers do not say anything about the quality of the work that is done. Decisions not to prosecute and acquittals must not be equated with a poor result or failure to achieve goals. A decision not to prosecute may be the most correct result, and there may of course be good investigative and prosecution work behind a dropped case. In the same way, an acquittal in the courts may be the most correct decision, including from the perspective of the police and the prosecuting authority. Examples are cases where it is clear after the presentation of evidence in court that acquittal is correct, and cases where there was reason to clarify a legal issue in the courts and the result in the case was acquittal, but where the goal of legal clarification was achieved. Launching a case can sometimes be the only or most appropriate way to investigate elements of a case, for example when it is desirable to use covert methods. Even if the information obtained in this way does not lead to a decision to prosecute, knowledge about unknown vulnerabilities may be uncovered and remediated.

Nevertheless, the proportion of cases of economic crime that are dropped is high and has increased over time. In addition, there has been an increase in cases that are dropped due to a lack of case processing capacity.41

Another challenge seen over many years, has also been that the police drop a large number of cases based on reports from other public agencies where there is thorough documentation of serious offences. When the police and prosecuting authorities are not sufficiently able to follow up the efforts of the regulatory agencies in their areas of responsibility, this creates challenges. For example, from the point of view of the Tax Administration, a failure to follow up on tax crime can in fact be seen as a threat to the legitimacy of the tax system itself. The regulatory agencies and administrators have consistently reported capacity problems and high employee turnover in most police districts. In many police districts, this has also led to a lesser extent of the regulatory agencies reporting the criminal offences they uncover.42 See more about this in Chapters 6 and 11.

Economic crime often involves complex types of crime that can be difficult to uncover and resource-intensive to investigate. It is therefore important to work more proactively with collection, analysis, and measures to prevent crime from happening in the first place. This is discussed in more detail in chapter 8.

3.7 Unreported figures for economic crime

3.7.1 Surveys on scale

In order to know the true scale of economic crime, knowledge of unreported or uncovered crime is important. The size of the unreported figures at any given time will be affected both by the victims’ propensity to report crime, and the ability of police and regulatory agencies to uncover crime.

The extent of economic crime involving a specific victim can be investigated with the help of surveys. Although they are a recognised method for providing information on the scale of the issue, surveys also have some important limitations. Respondents may answer incorrectly, misunderstand questions, not remember when an offence has occurred, or deliberately try to exaggerate or understate the scale. The timing of the survey can also affect its results, especially when it comes to perceptions of how widespread economic crime is.

In the following, the white paper discusses surveys of a representative sample of private and public enterprises and municipalities, to highlight which offences the enterprises and municipalities themselves state that they have been subjected to in the past year. Surveys have been conducted for the years 2003, 2008, and 2021.43 The Ministry of Justice and Public Security will fund a similar study in the coming years in order to create a time series (see chapter 15).

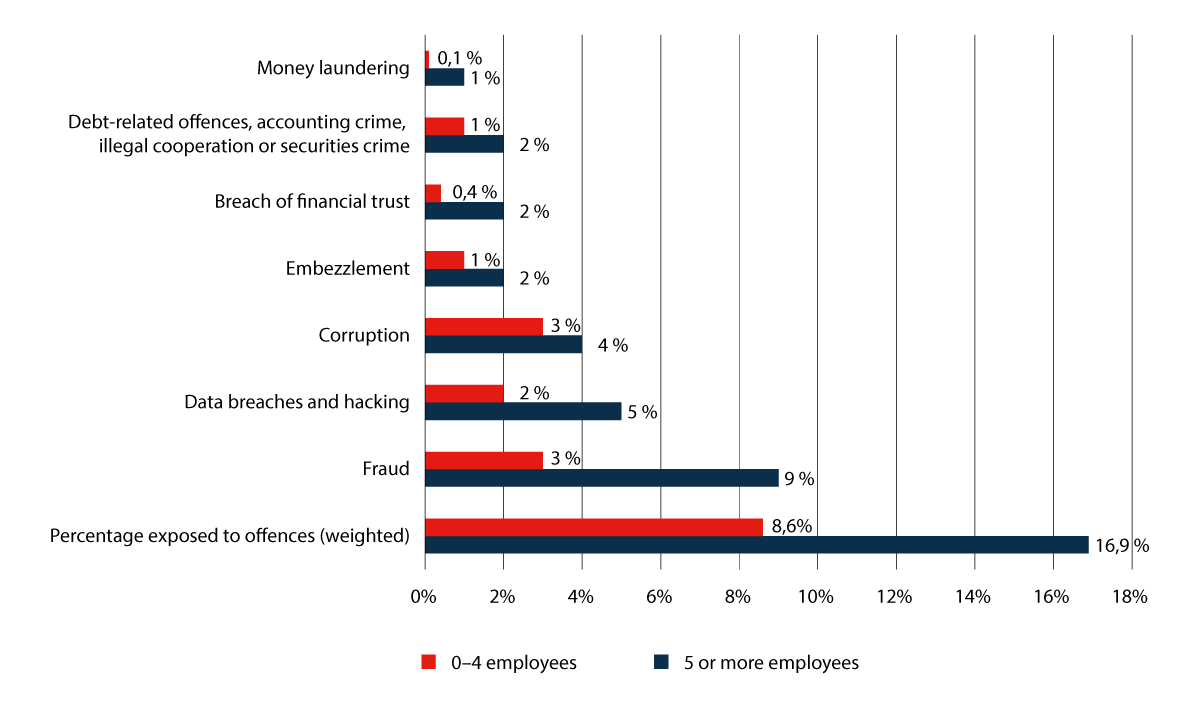

The surveys show a decrease of five per cent from 2003 to 2008, and a stable scale of economic crime since 2008.44 In total, 10 per cent of all businesses responded that they were subjected to economic crime in 2021. The figures vary greatly according to the size of the enterprises. 17 per cent of enterprises with five or more employees state that they had been exposed to economic crime during 2021.45 8.6 per cent of the enterprises with fewer than five employees answer the same.

Figure 3.4 Percentage of enterprises subjected to economic crime in 2021.

Source: Survey conducted by Vista Analyse 2022

As shown in Figure 3.4, fraud is the most common type of economic crime. Nine per cent of enterprises with five or more employees reported having been exposed to fraud.

Four and five per cent, respectively, responded that they had been victims of corruption and data breaches. The corresponding figures for enterprises with fewer than five employees are three per cent for fraud and corruption and two per cent for data breaches.

The largest enterprises with 100 or more employees are most vulnerable to economic crime. 26 per cent of enterprises with more than 100 employees stated that they had been victims of economic crime. This concerns in particular the two most common offences, fraud and data breaches. The relationship is not linear, as enterprises with 20 to 49 employees had been somewhat more subjected than those with 50 to 99 employees.

With the exception of data breaches and fraud, the companies respond that they perceive the risk of being exposed to most types of economic crime as low. Between 80 and 90 per cent of the enterprises consider the risk of being exposed to offences such as accounting-related crime, corruption, and embezzlement to be low. When it comes to data breaches, 12 per cent consider the risk to be high, and 50 per cent consider the risk to be medium. The corresponding figures for fraud are 4 and 27 per cent.

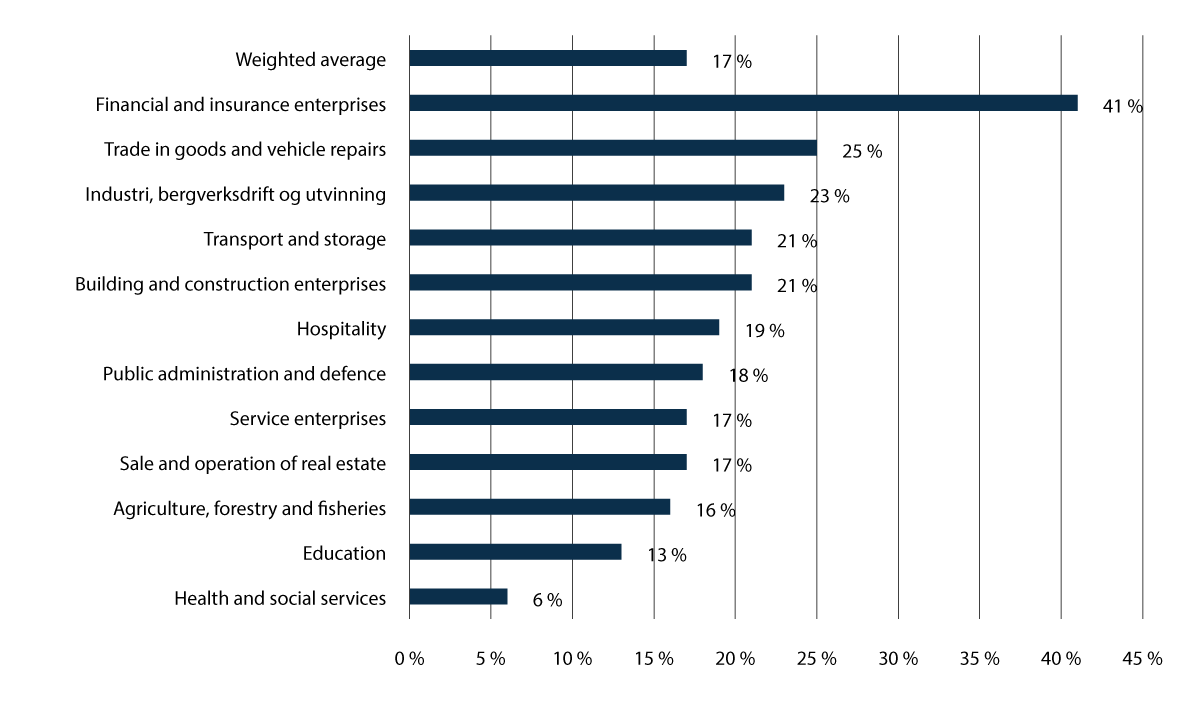

The survey also shows that there is great variation among different industries with regard to how many people have been victims of economic crime.

Figure 3.5 The percentage of enterprises reporting that they were subjected to economic crime in 2021, by type of industry. Businesses with five or more employees.

Source: Survey conducted by Vista Analyse 2022

Enterprises in finance and insurance state that they are most vulnerable. These are industries dominated by relatively few large companies with many customers who can potentially defraud them. Enterprises in health and social services and education state that they are least vulnerable. The difference between other enterprises is small, and varies between 16 and 25 per cent.

3.7.2 The enterprises report about 15 per cent of the offences

The survey also shows that the enterprises state that they have reported about 15 per cent of the offences. There is great variation between the offences. Embezzlement (39 per cent) is most commonly reported, followed by money laundering (33 per cent), and fraud (21 per cent). Corruption (2 per cent), accounting-related crime (6 per cent), and data breaches (9 per cent) are the least commonly reported.

When asked why they chose not to report, the most common answer from companies is that there is nothing to be gained from filing a complaint. Furthermore, the companies respond that it is resource-intensive to file a criminal complaint, and that it will be difficult to prove that it is a violation of the law. Few feel that the police lack competence. For data breaches and embezzlement, 29 and 42 per cent, respectively, cite a lack of police resources as the reason why they chose not to file a complaint.

The latest survey shows a decrease in the proportion who report the most recent offence affecting them to the police. In 2008, 30 per cent filed a complaint in the case, compared to 15 per cent in 2021.

3.7.3 Municipalities report a lower prevalence than enterprises

In the latest survey, Norwegian municipalities state that they have been subjected to economic crime to a lesser extent than enterprises with five or more employees. 14 per cent of the municipalities respond that they were subjected to economic crime in 2021. Fraud is most common, with 11 per cent. Three per cent respond that they had been subjected to data breaches and two per cent to breach of financial trust.

Just over half of the municipalities state that they consider the risk of most types of economic crime to be small. However, there is some variation between different types of offences. Between 30 and 45 per cent of the municipalities state that they perceive the risk of being exposed to illegal cooperation, corruption, and bribery, breach of financial trust, embezzlement, and fraud as medium. About 80 per cent of the municipalities consider the risk of data breaches to be high or medium.

It is important to note that there is methodological uncertainty associated with the results for the municipalities, due to weaker representativeness.

3.7.4 Economic crime against private individuals

The National Safety Survey 2020 and the National Safety Survey 2022 show a lower level of economic crime directed at private individuals than against businesses.46 Fraud and identity theft are among the most prevalent forms of crime. At the same time, it appears that relatively few state that they have been subjected to this. In 2020, 7.5 per cent responded that they had been subjected to fraud when buying goods or services over the internet, and 5 per cent to financial fraud when buying or selling. In 2022, the proportions were 7 and 5 per cent, respectively. 4 per cent said they had experienced payment card or personal information fraud in both 2020 and 2022. By comparison, 6 per cent had been exposed to bicycle theft in 2020, and 7 per cent in 2022.

The National Security Survey also details people’s worry about being subjected to crime. It appears that the vast majority are not worried about this. It is most common to be concerned about being subjected to fraud on the internet. In 2022, 26 per cent were concerned about this, and 15 per cent concerned about identity theft.

The survey also shows that the population reports the lowest financial loss for fraud, compared to other types of offences for gain. In 2022, the median value of the financial loss due to payment card or personal data fraud was NOK 1,200 and NOK 1,000 for fraud in connection with purchases or sales. The corresponding amounts for car theft were NOK 10,000 and NOK 4,000 for bicycle theft. In 2022, 9 and 21 per cent responded that they reported fraud in connection with purchases and sales and payment card or personal data fraud, respectively. The survey shows a clear correlation between the amount of the financial loss and the likelihood that the offence will be reported.

Another aspect of economic crime that affects individuals concerns exploitation in employment relationships. In its threat assessment from 2022, Økokrim assesses that it is likely that criminal actors will attempt to exploit refugees from Ukraine and other foreign and vulnerable workers for undeclared and illegal work. ID misuse can be included as part of this. According to Økokrim’s threat assessment, labour exploitation occurs particularly in labour-intensive occupations with a high proportion of unskilled workers. Unregistered foreign workers who receive payment in cash are vulnerable to being exploited by the employer unjustly enriching themselves on their wages. Økokrim also warns that young and vulnerable workers are being exploited by criminal actors as “money mules” to launder illegally obtained proceeds.47

According to a report by Fafo, a Norwegian independent social science research foundation, some foreign workers residing in Norway find themselves in grey areas in the labour market, but these grey areas are ones in which the exploitation does not take such forms that it can be considered human trafficking.48

3.7.5 Economic crime against the welfare state

In terms of methodology, it is challenging to research economic crimes for which there is no specified victim. Existing estimates are therefore subject to uncertainty. There are many types of economic crime where there is little research and statistics that shed light on the possible extent. The unreported numbers can be large, and we do not know how large.

Non-compliance with tax and duty regulations illustrates this challenge. “Tax gap” is a term used to describe the difference between the tax that would have been paid if everyone fulfilled their tax obligations and the tax that is actually paid. The tax gap is due to non-compliance by both registered and unregistered enterprises. However, non-compliance is not the same as economic crime. Some errors are due to unclear regulations or a lack of knowledge in the business community or among the general public. It is often difficult to distinguish between conscious and unconscious errors.

Part of the tax gap is about underreporting of legal and known activity. Another part is unregistered legal and illegal activity, also referred to as the “shadow economy”. It includes financial activity and income from illegal enterprises and activities such as drug trafficking, and from legal activities that are not reported to the tax authorities. An estimate of the Norwegian shadow economy indicates an order of magnitude of between 1–5 per cent of mainland GDP for 2019.49 This implies a total hidden value creation of NOK 27–133 billion, which corresponds to lost tax revenues of NOK 10.8–53.2 billion. Such estimates are subject to considerable uncertainty.

Another part of the tax gap is about the overreporting of deductions. Based on random checks of personal taxpayers’ deductions in the tax return, the Tax Administration has calculated a tax gap (lost tax revenue) of NOK 1.2 billion for the 300,000 taxpayers who increase their deductions in the tax return. This amount does not distinguish between conscious and unconscious errors. For other parts of the tax gap, the Tax Administration has more uncertain estimates or only individual observations of the methods used without being able to say anything about the overall scale.50

International research suggests that the use of randomised checks is the most reliable method for estimating the extent of tax evasion and tax gaps, especially in combination with other data sources.51 Based on randomised checks, a Danish study has found that there is very little tax evasion for areas where there is third-party reporting. For the self-employed, the study finds that a far larger proportion evaded taxes.52 According to a study based on randomised checks, microdata and data on the use of tax amnesties in Norway, Sweden and Denmark, the richest per thousand of the population evade about 25 per cent of their taxes.53 The study also shows that the level is so large that it would change the calculations of inequality, as the unreported income and wealth increase the wealth of the richest per thousand by thirty per cent.

A new report shows that the extent of assets concealed internationally has been significantly reduced following the introduction of information exchange agreements between countries.54 At the same time, the report points out that there are signs that evasion is shifting towards assets that are not covered by these agreements, particularly real estate.

Furthermore, research indicates that 70 per cent of the properties in Dubai that are owned by Norwegian residents had not been declared to the tax authorities, which could indicate tax evasion.55

Figure 3.6 Property abroad is not always reported to the tax authorities and may be funded with the help of proceeds from crime

Photo: courtesy of Økokrim

The extent of social security fraud and incorrect payments has been examined in five different investigations from the period 2011–2020. All the reports show large unreported figures for irregularities and errors that have not been detected. The estimates do not distinguish between conscious and unconscious errors on the part of the user or errors in the agency’s case processing, and are thus not an estimate of economic crime. The reports include six major benefits paid by the Norwegian Labour and Welfare Administration. An estimate based on these studies and the fact that many benefits have not been examined indicates that the Norwegian Labour and Welfare Administration incorrectly pays out at least NOK 5 billion per year. Of the presumed wrongly paid amount of NOK 5 billion, just under NOK 1 billion is being reclaimed.56

The Norwegian Competition Authority conducted two surveys in 2017 and 2021, the purpose of which was to detail the extent to which Norwegian companies experience competition crime in their industry.57 In the 2021 survey, between 20 and 30 per cent of business leaders answered yes to various questions about whether anti-competitive cooperation, price collusion, market sharing, and tender cooperation exist in the market in which they operate.

A knowledge overview obtained by the Ministry of Justice and Public Security in 2023 shows that most research is in the area of taxes and duties.58 The knowledge base concerning the potential scale in other areas is considerably weaker. For example, a report on the extent of bankruptcy-related crime states that there are few statistics available, and it therefore makes estimates based on impressions from actors working within the field.59

4 The organisation of efforts to combat economic crime

4.1 Joint responsibility for prevention and control

As mentioned at the outset, the prevention and combating of economic crime is the responsibility of the authorities, businesses, and private individuals.

The police and prosecuting authority are key players in both the prevention and prosecution of cases of violations.