Part 2

The Government’s assessments and measures

6 Management and prioritisation of economic crime

6.1 Economic crime must be given sufficient priority

Prioritisation between different types of crime in the police and the prosecuting authority is done based on policy governing documents, such as the Government platform, Prop. 1 S and Recommendation 6 S. The management signals are communicated to the agencies e.g. through the ministries’ letters of allocation.

The police have a distinctive governance structure. In principle, the responsibility is divided into two parts, with criminal proceedings under the Higher Prosecution Authorities (DHP), and the rest of the police work under the National Police Directorate (POD). Both agencies are under the Ministry of Justice and Public Security.

The Ministry’s letter of allocation to the police, and POD’s performance agreements for the police districts, are designed based on a starting point of performance management, often in combination with more detailed management in individual areas. Detailed management can be a challenge for the police’s goal attainment.

In the Ministry of Justice and Public Security’s letter of allocation to the police for 2024, organised and economic crime is highlighted as one of the priority areas where POD has been asked to report on the efforts of both preventive measures and criminal proceedings. Furthermore, it has been specifically pointed out that proceeds from criminal acts shall be confiscated, and that cases with confiscation potential shall be prioritised. Efforts to combat economic crime were also highlighted as a priority crime area in the letters of allocation to the police for 2022 and 2023, but to varying degrees in the previous years. As a follow-up to the interagency cooperation to prevent and combat work-related crime, this topic has been highlighted in the annual letters of allocation since 2015.

The Director of Public Prosecutions has the overall responsibility for criminal proceedings, both in the police and in the Higher Prosecution Authorities. For criminal proceedings, the Director of Public Prosecutions’ signals communicated through the annual circular on goals and priorities are therefore an important governing document. In this circular, the Director of Public Prosecutions specifies which case areas are to be given special priority at any given time with regard to initiating and conducting investigations. Economic crime is included in the Director of Public Prosecutions’ central priority areas, along with a number of other areas.

This chapter takes a closer look at potential solutions that can help ensure that economic crime is given sufficient priority in the police districts and that cases are not discontinued due to a lack of capacity.

6.2 The need for coordinated management

The prevention and combating of economic crime is the responsibility of several agencies and several ministries. It is therefore an important prerequisite that the use of policy instruments and management in this field are coordinated across the ministries. Coordination through governance and management is a key ministerial task. It will also entail a clear division of responsibilities between the agencies. In such cases, management must be coordinated to achieve the best possible effect from the measures.1

As mentioned, the Ministry of Justice and Public Security’s letter of allocation to the police provides guidelines for which areas are to be prioritised each year and for which goals are to be achieved. Similarly, other ministries issue guidelines to their subordinate agencies. The management of the police must be seen in the context of the management of the regulatory agencies, which are also measured by their results in the fight against economic crime.

Several of the control agencies’ efforts to combat economic crime have been strengthened in recent years, based on a political desire to reduce the scale of, for example, fraud and work-related crime. For example, one of the objectives of the Norwegian Labour Inspection Authority is to uncover and combat work-related crime, and one of the six main objectives of the Financial Supervisory Authority of Norway is to combat crime in the financial area. Furthermore, the Tax Administration is monitored on whether businesses experience a high probability of detection. Preventing and combating work-related crime is also a priority area for the Tax Administration. In the Competition Authority’s letter of allocation, the Authority is asked to uncover and prevent competition crime in order to achieve its main objective. Norwegian Customs’ main goal is that the actors in the movement of goods should perceive the risk of non-compliance as high. The Labour and Welfare Administration is asked to prevent, detect, and follow up on social security misuse. For 2023 and 2024 specifically, the agency was asked to strengthen its efforts to carry out follow-up checks with the aim of uncovering several incorrect payments related to the temporary COVID measures.

However, strengthening efforts to combat economic crime may have the potential for greater socio-economic benefit if the resource input in the various sectors is better coordinated. For example, an initiative within a regulatory agency will have a greater effect if the resources in the police are similarly prioritised for the processing of criminal complaints resulting from the initiative.

From time to time, common goals may be expressed across several ministries, as is sometimes the case for the agencies that are part of the work-related crime cooperation, where common guidelines are given in the letters of allocation from the Ministry of Labour and Social Inclusion, the Ministry of Finance, and the Ministry of Justice and Public Security to the agencies concerned. The need for improvement of the strategic management in this area is also discussed in an evaluation of the agency’s cooperation against work-related crime, which has since been followed up in a joint assignment to the agencies participating in the cooperation.2

The Government’s assessment

The Government believes that there is a need for more coordinated management in the area of economic crime. We have a greater chance of succeeding when multiple ministries and agencies have similar priorities. A first step towards this could be to establish a mechanism for following up the measures in this white paper, organised as a permanent cooperation between the relevant ministries, and with the potential for participation by relevant subordinate agencies.

A model for such cooperation could be the interdepartmental cooperation on the fight against economic crime, which was established in 2004 and eventually became known as the Departmental Committee against Economic crime (DEPØK). The collaboration was led by the Ministry of Justice and Public Security and also had participants from, among others, the Ministry of Finance, the Ministry of Trade, Industry and Fisheries, and the Ministry of Labour and Social Inclusion, as well as the National Authority for Investigation and Prosecution of Economic and Environmental Crime (Økokrim). The committee was responsible for following up on previous governments’ action plans against economic crime.

In addition to following up on the measures in the white paper, such interministerial cooperation may be well suited to considering the use of instruments that can promote co-governance and common priorities. This could help to increase goal attainment and ensure a more effective fight against current challenges. The cooperation will not have any formal status in the ordinary management dialogue, but will have the purpose of promoting coordinated prioritisation and the use of policy instruments.

A number of the measures in this white paper are also important for efforts to combat work-related crime. The Government considers the efforts to combat economic crime and work-related crime in context, and will also facilitate continued cooperation across areas of government in this area.

The Ministry of Justice and Public Security is closest to establishing cooperation on economic crime as described and facilitating a mechanism for following up the measures in the white paper. The mechanism will also facilitate follow-up of other challenges addressed in the white paper. Initially, the mechanism will have a time perspective of four years.

-

The Government will establish an interdepartmental mechanism for following up the measures in the white paper on economic crime. A matrix will be prepared for further follow-up of the measures in the white paper and other measures identified by the collaboration, initially for a period of four years.

6.3 Local variations can lead to lower priorities and less equality before the law

The police’s social mandate is broad. Through preventive, enforcement and assisting activities, the police shall be part of society’s overall efforts to promote and consolidate citizens’ legal protection, security, and welfare in general. Consideration for life and health is of course given priority, which in the field of criminal cases means that violence, murder, and sexual offences will often be given the highest priority.

When more ambitious goals and priorities are put forward than it is possible to achieve within a given resource framework, the real priorities are pushed downwards in the management line. The Norwegian Agency for Public and Financial Management’s (DFØ) follow-up report on the police reform from December 2022 also states that the real priorities in practice take place some way down in the chain of command.3 It is therein described as a challenge for the police that they are steered far more and more closely by factors relating to efforts and activities than by achieved results and effects.

Equality before the law is fundamental to the rule of law and to a well-functioning democracy. Equality before the law means that similar cases must be treated equally. However, based on insights from Project Eco and statistics and interviews with the police districts, there is no doubt that financial criminal cases are processed and prioritised differently in the police districts.

A specific example is that the threshold amount for when a case is considered sufficiently serious to be processed by a specialist environment may vary. At one point, the limit in Møre og Romsdal Police District was in practice NOK 200,000, while it was NOK 2 million in East Police District. The threshold amount is not absolute, but for cases that fall below these thresholds, there is a higher probability that the case will be handled by generalists without financial expertise.

In addition, the resource situation is significantly different in different police districts. This also leads to different priorities. For example, some police districts may work in a structured manner on criminal complaints made by the Tax Administration, while the same type of cases are generally given lower priority for capacity reasons in other police districts.

Such differences can lead to legal inequality, and are perceived as unsatisfactory and unfair for those affected by the crime.

6.4 A comprehensive system of priorities

Criminal procedure is based on a balance between efficiency and the rule of law.4 Prioritisation is a prerequisite for working efficiently when there is a shortage of resources. There are significant differences in how resource-intensive different offences are for the police and the prosecuting authority. It is therefore necessary to have a very different distribution of resources between different crime areas and different tasks in the police and prosecuting authority.

Some offences are serious in the form of major financial losses for the victim, while other offences violate physical and mental health. Other offences are in turn serious for society as a whole in that they affect fundamental societal functions and national interests. How the different dimensions of the seriousness of offences are to be weighted in the allocation of resources is a matter of fundamental value choices. This may justify that priorities should be rooted in the public’s perception of justice through open and verifiable processes in the public sphere.

Without concrete guidelines for priorities, it is more difficult to distribute resources, but also to justify the distribution. At the same time, the prosecuting authority is independent and cannot be instructed in individual cases, which will also have an impact on the guidelines that can be given for handling criminal cases.

The police and the prosecuting authority have a fundamental challenge in that the need for resources will always exceed the resources that are available. This is shown by the fact that the police and the prosecuting authority already have a number of principles and guidelines that assume that resources are scarce. However, these principles and guidelines have not been set in a comprehensive system. Most of the priorities are therefore left to the local police district. Measures may be necessary to ensure, among other things, that the Director of Public Prosecutions’ directives and priorities have an impact on the police’s activities.

The question of examining prioritisation criteria is relevant to some of the challenges described in Box 5.1 and has therefore been discussed in connection with the work on the white paper. However, since all areas of crime compete for the same resources, the question of how to ensure a more comprehensive system of priorities must be addressed in a broader perspective than a white paper on economic crime allows.

6.5 Organisational structure as a tool for prioritisation

6.5.1 Other organisational models

The way in which an agency or field is organised may affect both its room for manoeuvre and governance. Organisation can also contribute to a real prioritisation of certain disciplines, particularly if new units are established with specific purposes or if resource management of certain areas is based on a professional division, such as the work-related crime cooperation with the establishment of work-related crime centres.

The agencies themselves have considerable leeway in terms of their own organisation. In some cases, however, it is the case that the responsible ministry is involved in issues relating to this, particularly where organisational changes introduce a need for regulation or financial support.

Questions about organisational changes in the field of economic crime have been discussed several times.5 Considerations that are opposed to each other in these assessments are often the need for shielding resources, compared to the need for flexibility in resource utilisation and interaction between different professional environments.

As mentioned earlier, other countries have chosen different models for investigating and prosecuting economic crime (see section 4.7). There may be reason to take a closer look at the possibility of alternatives to the current organisation as a solution to some of the challenges listed in Box 5.1.

6.5.2 Study of how the police is organised

In 2022, at the same time as the work on this white paper was initiated, the National Police Directorate tasked Økokrim with investigating whether the police’s organisation of intelligence, prevention, and investigation of economic crime and environmental crime supports a targeted and effective solution to its social mandate. The report was intended to shed light on and assess the appropriateness of the current organisation with current professional administrative responsibilities and other ways of organising the work.

For its report, Økokrim has obtained information, views and assessments from all police districts, the Higher Prosecution Authority, and other stakeholders. The police chiefs of East Police District, Innlandet Police District, Agder Police District and the Chief of Kripos have participated in the project’s reference group.

The report with recommendations for organisational changes was submitted to the National Police Directorate in late August 2023. The National Police Directorate has initially responded by sending it for consultation to all units in the police, trade unions, and the chief safety representative. When this round of consultations has ended, the Director of Public Prosecutions will also be involved and give their assessment.

-

The Government will follow up on Økokrim’s report on the organisation of the police’s efforts to combat economic crime and environmental crime once the National Police Directorate has completed its work.

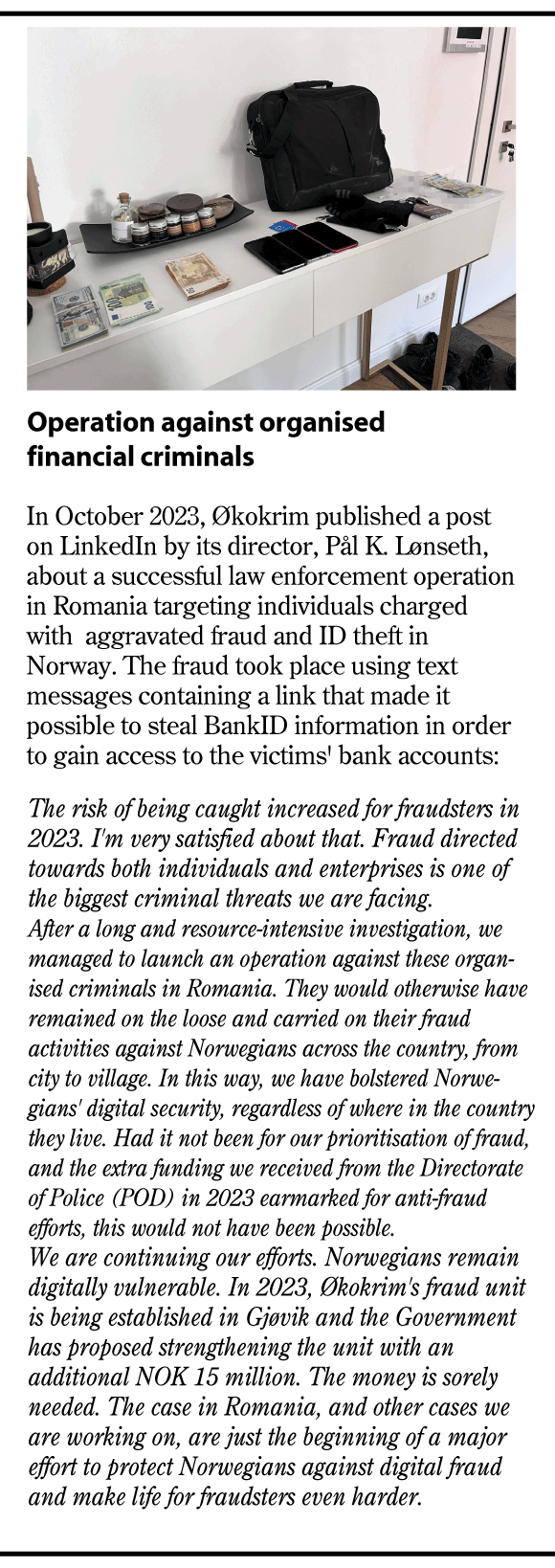

Figure 6.1 Operation against organised financial criminals

Source: Økokrim

6.5.3 Establishment of a fraud unit

As described in section 3.3, both the police and banks have registered a large increase in the number of digital fraud cases in recent years. Both private individuals, organisations and companies risk financial losses as a result of this. The police, banks, and IT security departments must also devote considerable resources to uncovering this crime. A consequence that is equally serious to financial losses may be that the public’s trust in private and public bodies, as well as in digital solutions, is weakened.

To address this challenge, Økokrim has decided to establish a national fraud unit. The purpose of the department will be to identify fraud offences that affect citizens across police districts, and/or that have international ramifications, and to bring about a more effective and structured fight against fraud, for example by implementing preventive measures in cooperation with banks and others in the business sector. These efforts will also help to strengthen the investigation of fraud that is organised and carried out systematically. In June 2023, the Government decided that Økokrim’s fraud unit will be located in Gjøvik.

The Government’s assessment

The Government is in favour of the establishment of a separate fraud unit. Ensuring the effectiveness of the fraud unit in its work to prevent fraud, including through contact with the relevant administrative bodies, fraud-prone industries and others with a role in crime prevention work, will be key.

In the national budget for 2024, the Government allocated NOK 15 million for the establishment of this. It is assumed that the work of the unit will also be able to facilitate input to the Ministry regarding proposals for regulatory changes or other needs identified in the area. The first regulatory measure that the Government already wishes to take a closer look at is the need to clarify the police’s authority to shut down websites that form the basis for digital fraud. The Ministry of Justice and Public Security will follow up the work through the ordinary management dialogue.

-

The Government will allocate funds to strengthen Økokrim’s fraud unit and consider further strengthening efforts to combat digital fraud, including considering clarification of existing legal bases for the police to prevent, stop, and avert digital fraud.

7 Recruitment and competence in the police and regulatory agencies

7.1 Competence is a fundamental prerequisite

Who is involved in the fight against economic crime and what expertise they have has a significant impact on whether the efforts pay off. Investigating economic crime has some special challenges compared to other forms of crime, partly because the evidence often involves analyses of complicated corporate structures and accounting documents.

The training of police investigators is general and does not provide investigators with special expertise in economic crime. Nor is there currently any specialised training aimed at the tasks of employees in the regulatory agencies.

For the Government, it is important that regulatory agencies, special agencies, and police districts all have access to the right expertise to combat economic crime. Furthermore, educational pathways should be facilitated that meet the need for special skills to the greatest extent possible, while at the same time facilitating a lasting and stable working relationship where competence can be built through experience. Specialised training courses for police investigators and for employees in the regulatory agencies and relevant continuing and further education programmes could contribute to this. Proper recruitment is also an important element in competence building.

This chapter discusses opportunities for strengthening competence and capacity through both recruitment and education.

7.2 Generalists and turnover in the police

The competence and prerequisites of the employees of the police to investigate and prosecute cases of economic crime depend on several factors. Education and previous professional experience are key, but colleagues’ competence, continuing and further education, access to sources and aids, personal commitment, and interest also affect the level of competence.

To work as a police investigator, one must have completed and passed the bachelor’s degree programme at the Norwegian Police University College, which is the basic education for all Norwegian police officers today. The formal competence that will provide a basis for investigating economic crime is limited to what can be extracted from general criminal law and general investigative training. In the bachelor’s programme at the Norwegian Police University College, the topic of confiscation is admittedly on the programme description, while economic crime and financial investigation are not included.

The prosecuting authority is also normally made up of generalists with no specialisation in economic crime. Legal counsellors in the police undergo training for new police advocates. This training is general and not specifically aimed at specific types of crime.

On this basis, it goes without saying that the competence acquired after basic education is important for the ability to investigate, litigate, and prosecute cases of economic crime. This is also the basis for the 2023 report What prevents the police’s investigation of corruption cases.6

Both investigators and police advocates are required to complete mandatory annual training. The topics are usually general and not aimed at economic crime. However, the Norwegian Police University College offers continuing and further education in economic crime, see section 7.6 for more on this.

Consequently, most of the specialist expertise is currently acquired through case work and transferred from more experienced colleagues. This means that experienced investigators and prosecutors are a key factor in maintaining competence.

In recent years, however, there has been a high turnover of investigators and prosecutors in the police districts. This is evident, among other things, from the Directorate for Public and Financial Management (DFØ)’s follow-up evaluation of the police reform from December 20227 and the Office of the Auditor General’s investigation of the Norwegian Police Service’s goal attainment on key tasks from 2022.8 For police investigators, the reason is often that they apply for operational service.

During 2022, the regional public prosecutor’s offices inspected the efforts against work-related crime in ten different police districts. Eight of these ten inspection reports highlight challenges with capacity and turnover of personnel resources in rural areas. Seven of the inspection reports point to challenges with a high discontinuance rate, weaknesses in investigation management, long case processing times, and long waiting times without processing the cases. This is supported by the National Police Directorate’s and the Director of Public Prosecutions’ joint report on criminal case processing in 2022, which shows that offences that were cleared up within the categories of working environment and finances in 2022 had by far the longest average case processing time, with 285 and 203 days, respectively.9

High turnover may be particularly unfortunate in police districts where there are few people who work on economic crime. The expertise is then more vulnerable than in larger and more robust environments. In addition, it is time- and resource-intensive to recruit new employees. Moreover, positions are often left unfilled for a period in connection with resignation and hiring.

7.3 Competence in regulatory agencies

It is also a challenge for the regulatory agencies that the complexity of the cases is constantly increasing. This challenges competence. There are increasing areas where cutting-edge expertise is necessary. Expertise is also, to a greater extent than before, perishable.

Each regulatory agency often has special expertise that in many cases is necessary for the successful handling of criminal cases in the field of economic crime. They know their own field of expertise and the handling of specific matters in their own agency, which is often a prerequisite for understanding criminal cases in the area. Furthermore, through their control activities, they are familiar with the preservation of evidence and trace protection. For example, the Tax Administration has good expertise in electronic trace protection and evidence preservation and good expertise in ID checks. These are areas where targeted work has been done on skills development for a number of years. In addition, the agency has expertise environments in more focused parts of the business sector and technologies such as blockchain and crypto.

Agency-specific training is available in several places, including the Directorate of Fisheries and the Coast Guard, which assist in each other’s basic training. There has also been participation from the police and prosecuting authority in these courses. This is valuable, because the police and the prosecuting authority know the special challenges associated with investigating and bringing cases before the courts. Through joint training, one can, for example, discuss how evidence should be secured by the Directorate of Fisheries and the Coast Guard so that the evidence will later have the greatest value for the police’s investigation and the prosecution’s assessments and presentation in court.

In addition, the Norwegian Police University College offers a continuing and further education programme that is also aimed at the regulatory agencies. The further education programme Interagency Combating of Economic crime is most relevant. Many employees in the regulatory agencies have completed the programme.

The further education programme Confiscation and Money Traces is offered to employees in the police and participating regulatory agencies, and is relevant for securing assets and confiscation, in addition to providing general knowledge about economic crime.

There are also courses at PHS in e.g. combating fisheries crime. The programme is specifically aimed at crime in the fishing industry, securing evidence, and control methods, and has been developed in close collaboration between the Directorate of Fisheries, the Coast Guard, and the Norwegian Police University College.

7.4 Complicated cases require special expertise

Cases of economic crime often require special expertise in the form of the ability to follow money flows, prepare financial analyses, and understand accounting and complex company structures. A professional police education alone does not provide a sufficient basis for getting to the bottom of such issues. A background in economics or knowledge of specific fields within finance and business may be important in the investigation of such cases.

Project Eco has shown that the level of competence in the police districts in the area of economic crime is often insufficient.10 The same is stated in Transparency International Norway’s and Erling Grimstad’s report What prevents the police’s investigation of corruption cases, which concludes that the investigation of corruption cases requires considerable expertise, which is called for in several of the police districts.11

This challenge applies to several types of economic crime, especially crime that requires insight into phenomena and fields, such as the securities market or money laundering through the art trade. Illustrative examples are given in Box 7.1 on corruption and 7.2 on cultural heritage crime.

Textbox 7.1 Expertise on corruption

To investigate corruption, one must understand how corruption takes place, where corruption occurs, what constitutes a ‘red flag’ for corruption, and how corruption takes place in practice.

Knowledge of the business sector is often necessary to be able to identify non-conformities that can help uncover corruption: how the business sector works, what is common practice, how industries should be understood, who has ties to each other and why, is knowledge that is required to be able to conduct targeted investigations. A new corruption case often means a new field for investigators, and it is necessary to familiarise oneself with the field in order to understand the evidence.

Corruption is difficult to prove because everyone involved often benefits from keeping the crime concealed. There is rarely a specific offender. The relationship can lie far back in time, the people involved are often resourceful, they have often coordinated cover stories, and it is difficult to get explanations that shed light on the case.

Corruption cases often require extensive money trail investigations to find the payment of a bribe, which is often concealed to give the transfer a semblance of legitimacy. Transfers of sums are concealed as loans and consideration in agreements. To uncover this, one must understand accounting. It can be extra challenging to follow the money trails when virtual currency and cash are also used to hinder traceability.

In cases that have links abroad, international cooperation is also necessary. In addition to methodological knowledge, this often requires both language skills and cultural understanding.

Textbox 7.2 Expertise on cultural heritage

In 2008, the study Working with cultural heritage by the University of Oslo pointed to the need for competence development and more training of Norwegian Customs and the police, who are primarily responsible for preventing cultural heritage crime.1

Almost 80 per cent of the respondents said that they lacked basic knowledge about cultural artefacts and did not know what to look for. The respondents from the police were generally uncertain about how such crime should be investigated. The report stated that there was a need for a general introduction to laws and legislation, visual training in the recognition of cultural artefacts, in-depth study of art and cultural history, in addition to more knowledge about cultural heritage crime and related crime areas.

The same conclusions find support in the European Commission’s report on illegal trade in Europe, more than ten years later.2 In order to remedy the lack of knowledge among various actors, UNESCO and the European Commission developed online courses aimed at customs, the police, and the judiciary in 2018 to contribute to awareness and knowledge development. A similar competence measure was aimed at the art dealer industry. Information about these initiatives was passed on to relevant agencies and actors in Norway, but it is unknown how many took advantage of the offer.

1 Jacobsen, H.M., Steen, T. and Ulsberg, M. (2008).

2 European Commission (2019).

7.5 Interdisciplinary competence is a criterion for success

The police districts’ economic and environmental departments are currently composed of special investigators with a background in economics, police investigators, and lawyers.

The special investigator often has financial expertise, in the form of a master’s degree in economics or accounting. Such a background is often necessary to understand complex accounting and catch red flags for economic crime. Money trail investigation and the ability to perform financial analyses also require such expertise. However, as new employees in the police, these special investigators do not generally have expertise in the police’s investigative methods. Interdisciplinary cooperation between the special investigator and the police investigator is therefore absolutely necessary.

PHS also offers two study programmes for civilians who have a bachelor’s degree in a field that provides relevant expertise for civilian positions in police investigations. The study programme General Introduction to Investigation – Strategies and Principles and General Introduction to Investigation Methodology are intended to equip specialists to contribute to investigative tasks in the police.

Each police district also employs one or more assistance auditors, a total of 20 people as of May 2023. The assistance auditor scheme means that auditors from the Tax Administration work on criminal cases under the authority of the Chief of Police, while retaining their employment with the Tax Administration. The assistance auditors are tasked with financial criminal cases, mainly in the area of taxation. The background for this part of the Tax Administration’s auditor assistance to the police is a desire to strengthen efforts to combat economic crime. An experienced assistance auditor has considerable accounting and auditing expertise and can contribute to better investigation and litigation. The scheme has been permanent since 1 January 1997 and is regulated in the National Police Directorate’s circular 2006/012 (with subsequent amendments).

“Interdisciplinary staffing with skilled employees” was already highlighted in the Director of Public Prosecutions’ circular 1/2006 as one of seven success criteria for a well-functioning economic and environmental department.12 However, as Table 7.1 shows, there are few special investigators with a background in economics at the eco-/environmental departments in the police districts. Developments since 2015 have been limited.13

Table 7.1 Overview of competence in the police districts from 2015 to 2023

|

2015 As of 14.9.15 Eco-/ environment |

2022 As of 30.06.22 Eco-/ environment |

2022 As of 30.06.2 Work- related crime |

2023 As of 30.06.23 Eco-/ environment |

2023 As of 30.06.23 Work- related crime |

|

|---|---|---|---|---|---|

|

Number of full-time equivalents in the police districts’ economic and environmental depts., including lawyers |

257.5 |

355.5 |

43.5 |

361.3 |

28.9 |

|

Proportion with only PHS education |

145 |

182.5 |

35.5 |

213.3 |

22.5 |

|

Relevant continuing education |

- |

- |

- |

- |

- |

|

Special investigators with other education (mainly economics education) |

50 |

58 |

2 |

64.2 |

1 |

Source: Økokrim

This shortage is exacerbated by the fact that this type of expertise is necessary, and also used, in other cases in the districts. Money trail investigations are often necessary and useful in cases of other profit-motivated crime, as pointed out in chapter 2.2. However, when employees are constantly withdrawn from the eco-/environmental departments, this necessarily affects the investigation of cases of economic crime.14

Technological development means that people are also dependent on technological expertise to an even greater extent than before. In the area of economic crime, there is a particular need for capacity and expertise to review and analyse digital evidence, including large digital seizures. The Office of the Auditor General’s investigation of the police’s efforts to combat crime through the use of ICT concluded that the police’s ability to detect and solve ICT crime had significant weaknesses.15 This is also linked to economic crime, which increasingly involves the use of digital tools.

Figure 7.1 Investigating economic crime requires different types of expertise

Photo: Leif Ingvald Skaug

The Government’s assessment

In the Government’s opinion, having enough employees with the right expertise in the police districts’ eco-/environmental departments is crucial for the police’s ability to succeed in investigating and preventing cases of economic crime. There is a need for more investigators with a background in economics in the police districts’ eco- and environmental departments. The development in the crime situation described in chapter 2 also indicates that there is a need for more investigators with the expertise and capacity to handle digital evidence, including seizures, in financial cases.

A strengthening of capacity and expertise in these areas is expected to have a positive effect on lowering the number of cases being discontinued as a result of a lack of case processing capacity. At the same time, strengthening the eco-/environmental departments will be beneficial for money trail investigations in other profit-motivated and organised crime, and contribute to greater opportunities for collaboration and assistance without necessarily stopping the investigation of major financial cases.

In the national budget for 2024, it has been decided to permanently strengthen the capacity of the police districts through earmarked positions for investigators with financial expertise and investigators with expertise in handling digital evidence.

Strengthening capacity will in itself help to make police districts less vulnerable and better facilitate the safeguarding of competent employees in the future. At the same time, this could help to create professional environments that ensure that important experience-based learning is not lost when investigators move to other positions after a short time.

-

The Government will strengthen Økokrim and existing professional environments in the police districts with new special investigators with financial expertise, as well as digital tools and expertise in handling digital evidence.

7.6 Relevant measures at the Norwegian Police University College and other research and educational institutions

As mentioned above, it is not realistic that the police will be able to solve economic crime only with the help of police graduates. Today’s crime situation requires the police to recruit specialists and provide them with investigative expertise.

However, the education should also facilitate further use of economists/auditors, computer engineers, and other specialists who can contribute to raising the analytical capacity, quality, and efficiency of investigations. The competition for civilian professionals such as economists, technologists, and lawyers is intense, and it is important to implement adequate measures to ensure recruitment and measures to retain critical expertise.

The regulatory agencies also need additional expertise to be better able to handle more cases and to prevent economic crime. Similarly, there may be a need for private actors, including those who have a role in anti-money laundering work, to strengthen their expertise. There has been a shift in recent years towards more knowledge-based work, and there have been demands for higher formal qualifications for a number of positions in both the police and in the regulatory agencies.

The Police University College has a central role in the education of those who work with economic crime. However, as previously mentioned, economic crime is not a topic covered to a large extent in the basic training for the police. It is important that employees who work with economic crime have a study programme that is perceived as useful and adequate. The requirement for a relevant and comprehensive study programme must apply regardless of what makes up the employee’s basic education.

The Government’s assessment

It is important to acknowledge that the investigation of economic crime requires a different level of expertise than that which can be acquired through today’s basic education at the Norwegian Police University College. Although experience-based learning will continue to be necessary in the future, it will provide a quite different starting point if new employees who are recruited also have a basic understanding of the field.

The Government believes that there may be reason to consider whether the curriculum of the basic degree programme and continued education programme at the Norwegian Police University College should to a greater extent facilitate specialisation in investigation. A master’s programme in investigation, with an emphasis on the specialised expertise required to investigate, among other things, economic crime, may be an option that should be explored.

Arrangements must be made for the subject curricula at the Norwegian Police University College to take into account the relevant competence needs, both in the basic degree programme and the continued education programmes. For example, knowledge of technical and tactical ID checks is not part of the curriculum for students at the Norwegian Police University College today. Basic knowledge of ID checks is an important tool in several of the police’s tasks, and could potentially be considered as part of the basic training. Similar knowledge may also be useful for the regulatory agencies.

Furthermore, provision should also be made for utilising other parts of the education system to offer relevant expertise in economic crime. One measure to strengthen the work in this area is the development of studies that tailor expertise on the topics of financial control/investigation, financial intelligence, and anti-money laundering. A number of regulatory agencies (the Norwegian Tax Administration, Norwegian Customs, NAV Control, the Financial Supervisory Authority of Norway, the Directorate of Fisheries, the Norwegian Gaming Authority, and the Norwegian Public Roads Administration) desire such expertise.

A proposal is being considered to establish an education programme on financial control and investigation as a collaboration between the Norwegian Police University College and other educational institutions. Such an offering is intended to educate people who it may be relevant to recruit both to the police and to the regulatory agencies. In the Government’s view, this is an important step on the way to ensuring that both the regulatory agencies and the police have access to people with the right expertise in the work on economic crime, who are also motivated to work in this particular field.

In the national budget for 2024, funds have been earmarked for a study on establishing an investigator degree programme at the Norwegian Police University College, possibly in collaboration with another educational institution.

This type of measure will need to be discussed further in dialogue with the National Police Directorate, the Police University College, and the Ministry of Education and Research.

-

The Government will follow up on the establishment of new training programmes in the field of economic crime for investigators and employees in the regulatory agencies.

-

The Government will establish special studies in the field of investigations, including of economic crime.

8 Staying ahead of crime: coordinated efforts to improve prevention

8.1 Prevention is profitable

It is a key goal of the Government that as many people as possible refrain from committing economic crime. Prevention is therefore key.

A review of the literature on preventive efforts shows that, compared with other areas of crime, there is limited research in the Norwegian context that deals with the prevention of economic crime.16 In the literature that exists, it is often emphasised that financial offenders are rational. In light of this, the importance of ordinary criminal proceedings as an important preventive element is emphasised. At the same time, the police and the prosecuting authority have limited resources. Moreover, there will probably be less room for manoeuvre for further strengthening the police in future national budgets.17 A broad preventive effort to counteract fraud should therefore also be prioritised for economic crime.

The police shall contribute to reduced crime and increased security for the public. The police are most useful if their combined efforts help reduce crime and unwanted incidents, reduce the harmful effects, and prevent recurrence. Prevention is therefore the police’s main strategy and must form the basis for how it completes all its duties.18 Reducing the number of offences and criminal acts can also contribute to security and stability, as well as increase people’s trust in the authorities and the justice system.

At the same time, one sees that economic crime is also largely moving into the digital space. National and international actors exploit vulnerabilities in legislation, regulations, infrastructure, and technical solutions to commit economic crime. A broad preventive effort to counteract irregularities and remediate vulnerabilities should therefore also be prioritised for economic crime. It will often be actors outside the police who have the right tools and measures.

A good overview of the threat and vulnerability situation is important for staying ahead of crime. The Government wishes to ensure that the sum of information can be utilised in the best possible way in a preventive track as well. Cooperation and information sharing and disclosure between public agencies and active involvement of the business community are important to achieve the best possible results.

This chapter discusses, among other things, measures that can strengthen prevention, including through better utilisation of intelligence and more cooperation between the police, regulatory agencies, and private actors. Rules and mechanisms that support transparency and information about beneficial ownership and identity are also important preventive factors, along with good utilisation of technology. These topics are discussed in chapters 9 and 10.

8.2 Prevention is the police’s primary strategy

The police work with intelligence and prevention of economic crime by collecting information about trends, methods, and vulnerabilities that are exploited by criminals. There is great potential in a proactive approach to this type of crime. The police will further develop their work on sharing and disclosing relevant information to cooperating agencies, superior authorities, the business sector, and private individuals in order to enable them to assess preventive measures within their own area of responsibility.

Investigation and prosecution, including confiscation of proceeds from criminal acts, have a preventive effect by highlighting the risk of detection and consequences for both individuals and the general public. However, proactive work will generally be more cost-effective than conducting reactive investigations, which often require a lot of resources and time. By preventing crime from happening, it is also possible to prevent individuals, businesses, and society from suffering financial losses and being exposed to other negative consequences as a result of crime.

Criminal actors adapt and develop new methods to circumvent the measures that are put in place. The police, authorities, and partners must therefore have good knowledge of risks and be able to initiate relevant preventive measures within their own area of responsibility.

In 2020, Økokrim established a separate department for intelligence and prevention. The police districts also have various projects that contribute to more targeted prevention of economic crime, including work-related crime. However, the overall feedback from the police is that the resources for prevention through e.g. collecting, analysing, and producing a knowledge base in the field of economic crime, are not sufficient.

8.3 The regulatory agencies’ preventive efforts

The regulatory agencies work preventively within their administrative areas. The deterrent effect inherent in the risk of being discovered, the possibility of sanctions, and the reporting of individual cases are important for preventive purposes. In addition, the regulatory agencies’ exercise of authority, license processing, data management, register management, and guidance contribute to the prevention of crime.

Part of the regulatory agencies’ preventive efforts consists of incorporating control mechanisms when developing new systems. The development towards digitalised and user-friendly services must also be balanced against the need for control and the need to avoid manipulation and abuse. System support that can help uncover and report inconsistent information between the registers is a key preventive mechanism that the agencies must develop to a greater extent.

The level of control must be sufficiently high, and controls must be carried out in a planned manner and based on risk assessments. The agencies’ preventive efforts are aimed at different target and risk groups and groups with identified problems. Prevention takes place e.g. through training and guidance. Preventive efforts depend on good access to and good quality of the agencies’ basic data, good register quality, and comprehensive ID management.

The agencies also emphasise mobilising actors outside the agency. This can be done through training, guidance, and binding cooperation agreements. For example, the Tax Administration cooperates with large public and private purchasers of services with a high risk of tax crime. The goal is to reduce the market for rogue providers and thereby reduce the potential for economic crime.

Experience from other countries and other agencies also provides useful knowledge for preventive efforts. For the Labour Inspection Authority, information measures aimed at foreign workers in Norway are an important preventive measure. The Norwegian Labour and Welfare Administration, for its part, has prepared an action plan against social security fraud and incorrect payments, which includes measures related to digital solutions, automated solutions and the use of register data as part of the preventive work. An important preventive element for the Financial Supervisory Authority is assessment of whether enterprises have sound procedures in place for the activities they are to conduct, both in the licensing process and through supervision. The Norwegian Competition Authority is carrying out important advocacy work aimed at companies to highlight the importance of competition and increase awareness of the Competition Act.19 Dialogue with industry associations, meetings, and lectures for various industries and organisations, and other forms of information sharing, are all a part of this.

In 2022, a department for the prevention of fisheries crime was established in the Ministry of Trade, Industry and Fisheries and in the Directorate of Fisheries. Regulatory tools are also important in the field of fisheries crime to prevent illegal activities.

The Norwegian Maritime Authority carries out both regular and unannounced inspections on Norwegian vessels. One of the focus areas of the Norwegian Maritime Authority’s inspections is the working and living conditions of those who work on board. In addition, reports of concern and tips about violations of the law are also processed. Through guidance on the regulations, the Directorate also wish to contribute to compliance with legal and regulatory requirements, and in this way prevent economic crime, among other things.

Figure 8.1 Prevention of fisheries crime

Photo: Jørgen Ree Wiig/Directorate of Fisheries

8.4 Intelligence: decision-making support for more targeted prevention and control

8.4.1 Intelligence within the police

Overall, the opportunities for the police and regulatory agencies to obtain information provide unique opportunities to establish a strong decision-making basis for further follow-up.

The police have an established national intelligence structure, which includes both the police districts and special agencies. The National Criminal Investigation Service is the national intelligence point. The police’s strategic intelligence products are based on the acquisition of targeted intelligence production at the district level, where the National Criminal Investigation Service has national production responsibility.

It is a goal that the police and regulatory agencies, the National Interagency Analysis and Intelligence Centre (NTAES) and the work-related crime centres can share information to be able to implement preventive activities and prioritise measures across the response options available to the police and the regulatory agencies together.

Economic crime has received increased focus in the police’s intelligence products in recent times. The police’s decision-making basis has therefore become better than before. The police’s information is particularly related to criminal networks in the areas of work-related crime, fisheries crime, foreign exchange exports, drug offences, and money laundering.

8.4.2 The regulatory agencies’ risk analyses and intelligence

Like the police, the regulatory agencies also engage in intelligence, knowledge building, and risk analysis through the collection of information and analyses in their areas. By sharing risk assessments and analyses with the police, they contribute to strengthening the data basis in the police’s intelligence production. The regulatory authorities also use information from the police to focus their control efforts and thus prevent crime by increasing the risk of it being detected.

In 2019, the Tax Administration established a separate department for intelligence. Much of the information the Tax Administration has in its own registers, and the analyses they conduct, can be of crucial importance for other agencies’ ability to uncover or follow up economic crime or other crime. The wage compensation case described in Box 8.1 is an example of this.

Textbox 8.1 The wage compensation case

In the period from March to August 2020, during the COVID-19 pandemic, a temporary unemployment benefit was established for furloughed workers (the wage compensation scheme). In May 2020, the Tax Administration discovered suspicious changes in its systems, and sent a tip-off to NAV Control about possible fictitious registration of employment relationships that could have been made to exploit the system. In parallel with this, NAV Control had begun to investigate individual actors and saw the same methods being used as the Tax Administration.

In connection with the investigation of these cases, NAV Control uncovered extensive ID fraud and registration of fictitious employment relationships using stolen and borrowed identities. The data was entered and then deleted after a short time to obtain unjustified salary compensation and make the misuse difficult to detect. Fictitious income data was also entered into the a-ordning scheme to obtain unjustified compensation for freelancers, as well as to form the basis for unemployment benefits and other support schemes. Fictitious income data has also been used in loan fraud against banks. These fraud offences have largely been carried out by people who have committed several types of crime (multi-crime offenders).

During the summer of 2020, NAV Control submitted a total of 17 criminal complaints to Oslo Police District and six reports to Økokrim. NAV Control assisted the police in the investigation. The cooperation between the police and NAV Control and the Tax Administration, respectively, was an important success factor. In parallel with the investigation, the Norwegian Labour and Welfare Administration made changes to the application system, establishing preventive measures to stop future fraud attempts.

The wage compensation case is an example of the systematic and risk-based use of register data. The Tax Administration’s analysis team assessed that payments in connection with the temporary COVID-19 schemes constituted a risk, and measures were implemented.

For Norwegian Customs’ control activities and other policy instruments to be targeted, they are dependent on intelligence as a basis for decision-making. The agency has therefore invested in technology and expertise in data and analysis, and collaborates with other agencies and actors that are relevant. Similarly, the Financial Supervisory Authority uses information from Økokrim and the police districts as an important source for its priorities.

In cooperation with the Coast Guard and fish sales associations, the Directorate of Fisheries prepares national strategic risk assessments to ensure that control resources are used where the need is greatest. In NOU 2019: 21 On the Future of Fisheries Control (Framtidens fiskerikontroll – at time of publication in Norwegian only), the Fisheries Control Committee proposed a strengthening of Økokrim’s intelligence capacity in the area of fisheries crime. In the revised national budget for 2023, NOK 5 million was transferred from the Ministry of Trade, Industry and Fisheries to the Ministry of Justice and Public Security’s budgets for this purpose. The funds will be used to build up a basic intelligence function in the area of fisheries crime. The aim is to provide the supervisory authorities and the police with a solid knowledge base for working more efficiently in their prevention and control work and, for the police, a good basis for decision-making in order to identify the right cases for investigation and prosecution. The measure is a trial project with a duration of four years, which began in the autumn of 2023, cf. Prop. 118 S (2022–2023) Additional allocations and reprioritisation in the 2023 national budget (Tilleggsbevilgninger og omprioriteringer i statsbudsjettet 2023 – at time of publication in Norwegian only).

8.4.3 Use of financial intelligence in the police and in the Tax Administration

Financial intelligence is particularly important for the prevention and combating of economic crime, but is also of great importance to other forms of crime.

In Norway, financial intelligence is mainly handled by the Financial Intelligence Unit (FIU) in the Department of Intelligence and Prevention at Økokrim. The FIU is the recipient of reports of suspicious transactions from reportable entities (STRs) pursuant to the Money Laundering Act. In addition, the FIU has the authority to obtain additional information about both reportable entities, from other countries’ FIUs and from a large number of public registers. The information is compiled and analysed and can be passed on to police districts, special agencies, and other supervisory authorities that can use it in criminal cases and in confiscation cases.

An important purpose of the reporting obligation under the Money Laundering Act is to make it easier to uncover profit-motivated crime and to prevent financial institutions and other reportable entities from being misused in the context of money laundering. The FIU is equipped with a unique legal warrant and access to sources for its analysis work. This makes it possible for valuable information that could not have been obtained in any other way to flow into the police’s preventive and crime-fighting activities.

Information received in STRs is used by the FIU in analyses that are intended to cover various purposes:

-

Strategic products

-

Thematic reports and information letters

-

Dissemination of intelligence products

-

Creation of criminal cases and self-reports in criminal cases

-

Suspension and confiscation

In 2014, Norway was criticised by the Financial Action Task Force (FATF) for making too little use of financial intelligence, because there are few criminal cases that can be directly traced back to STRs.20 In 2017, the Director of Public Prosecutions issued separate instructions on the use of information from the FIU in the police districts.21 It follows from the instructions that it is an overarching objective that the information received by the police from the FIU shall be used for the prevention and investigation of crime where there is suspicion of laundering of the proceeds of a criminal offence or the financing of terrorism, and for the confiscation of proceeds and artefacts. The police’s internal procedures must ensure that this purpose is safeguarded. The police use information from the FIU to a greater extent now than before, but there still seem to be challenges associated with the use of intelligence information from the FIU for the establishment of criminal proceedings.22

Information from STRs can also be communicated to the Norwegian Tax Administration for use in its work on tax and duties. The information is provided in written reports where the information has been processed. The STRs provide the Tax Administration with a better basis for risk assessments, as well as a better basis for dealing with serious tax crimes (related to both direct and indirect taxes) while there are still funds to secure. These reports have been important in triggering control activities by the agency, and the information has been of great importance in extensive tax cases. A cooperation agreement has been entered into to strengthen cooperation, and a secondment scheme has been established where employees from the Tax Administration work at the FIU and have direct access to information in the Money Laundering Register, to ensure an efficient and targeted transfer of information in line with the Tax Administration’s priorities.23

The supervisory authorities also receive information from the FIU where it is relevant to their control activities.

The Government’s assessment

Financial intelligence is an underutilised source of both preventive measures and crime investigations. The anti-money laundering regulations impose costly and extensive obligations on a large number of reportable actors, and it is important to ensure that the regulations are significantly effective in leading to the prevention, detection, and clearing up of crime. Shortcomings in the use of financial intelligence not only result in poorer results in crime prevention and crime fighting, but can also ultimately undermine the legitimacy of the regulations if the private sector’s increasing resource use and reporting do not lead to an adequate response by the police and prosecuting authorities; see more about this in section 8.4.4.

With analysis of STRs, there is room for improvement and further benefits relating to all of the above purposes:

-

more strategic products can be developed, which can help both the police and the regulatory agencies to have a better and more complete knowledge base for their priorities and efforts,

-

guidelines (thematic reports and information letters) can better enable those with a reporting obligation to uncover and report suspicious circumstances,

-

increased dissemination of intelligence products can provide a basis for more measures by the police and supervisory authorities,

-

the analyses can and should provide a basis for more criminal cases, and

-

more confiscation claims. With the help of the anti-money laundering regulations and the FIU’s legal basis, there is also a unique opportunity to stop transactions before or shortly after they are carried out, which provides unique opportunities to safeguard assets.

There is also considerable potential for improvement in the utilisation of financial intelligence by using more technology in the processing and analysis of such information.

As discussed above, it is important to ensure that financial intelligence leads to more criminal cases. In addition to increasing capacity in the police districts, other measures should also be implemented. There is currently no clear description of how or in what format financial intelligence should be shared. This is also not mentioned in the police’s intelligence doctrine. A standard or description of how the police can use intelligence information from the FIU to establish a criminal case could contribute to better utilisation of this information.

The Ministry of Justice and Public Security has commissioned the National Police Directorate to conduct a study of the police’s use of financial intelligence (including products produced by the FIU) and the specific results this produces, how many resources are used for anti-money laundering work nationally, and how the use of financial intelligence leads to cases of confiscation, and to identify any opportunities for improvement. It will be natural to take a closer look at solutions related to the challenges associated with the use of financial intelligence when this report is available. In this context, consideration will also be given to how the information can be shared more effectively with other agencies.

-

The Government will strengthen the police’s use of information from the Financial Intelligence Unit of Økokrim.

-

The Government will examine how financial intelligence can be shared with and utilised more effectively by other agencies, such as Norwegian Customs, the Financial Supervisory Authority of Norway, and the Norwegian Tax Administration.

8.4.4 Financial intelligence: increased reporting, but no increase in the capacity to process the reports

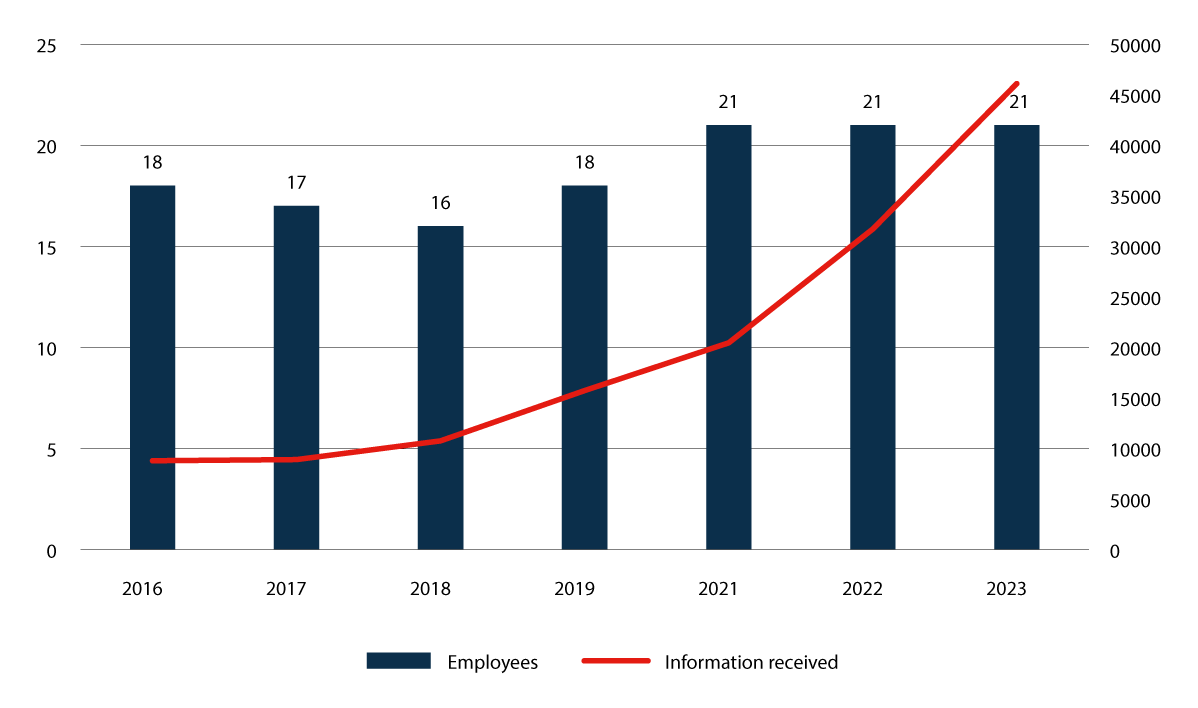

As mentioned in chapter 3.4, Økokrim and the FIU have in recent years noted a significant increase in the number of STRs from reportable entities in Norway, STRs from abroad, and reports on cross-border transactions with Norwegian recipients mediated by other Financial Intelligence Units (FIUs). The figure below shows the increase over the past seven years. The increase reflects the fact that those with a reporting obligation use considerable resources to prevent and make money laundering more difficult. The number of employees and available resources at the FIU and Økokrim has been relatively stable in the same period (Figure 8.2).

Figure 8.2 Information received vs. employees in the FIU

The increase in national STRs is largely due to increased reporting from certain reportable groups. At the same time that the number of STRs is increasing in scale, so is the content, quality and complexity of each individual report. This has gradually made it more challenging to utilise and analyse information that is reported, despite increased automated processing. Political agreement has recently been reached in the EU on a package of new anti-money laundering rules (see further discussion in section 12.4). The implementation of the new Anti-Money Laundering Directive, which is part of this package, will place additional demands on resources and systems to cover expected and new tasks resulting from the regulation.

The increased amount of data received has not been met with any change in the way data is processed, assessed, and analysed. The number of operational analyses carried out by the FIU, and the number of products disseminated for criminal proceedings and intelligence for use by the FIU’s partners have thus been relatively stable in recent years. Furthermore, the technical solutions related to software and the format of the reporting form itself have not been further developed to simplify, streamline, or otherwise promote good extractions and analyses of the actual data basis that comes in from the reporting entities. This increases the risk that time-critical information is not analysed and disseminated.

At the same time, there has been a marked increase in the number of requests for prohibitions on the execution of transactions, particularly related to ongoing fraud and international acquisitions or trades.24 In such inquiries, there is a great potential for the confiscation of illegal proceeds of crime.25

The Government’s assessment

The Government has noted that there is a major difference in the use of resources by those subject to the reporting obligation and the capacity of the police to process information from those subject to the reporting obligation. Both the police and other authorities may miss out on important information that the reportable entities have put a lot of effort into procuring. This leads to the information not being utilised well enough for preventive purposes. A lack of capacity to handle incoming information may also have consequences for the number of criminal cases concerning money laundering and confiscation of proceeds of crime.

Today, several manual processes are carried out in connection with the reception, analysis, and dissemination of information from the FIU. This is both resource-intensive and inappropriate. Even though the public sector’s use of resources cannot or should not necessarily be the same as that of those who are obliged to report in the private sector, Økokrim and the FIU must be given the capability to use automation to a far greater extent, in order to be able to fully utilise the legal basis provided for in the anti-money laundering regulation.

Implementation of the EU’s upcoming anti-money laundering package, including the new Anti-Money Laundering Directive, will require a comprehensive study (see section 12.4 for more details). It will be natural to monitor the challenges related to the FIU’s capacity and methods in connection with the implementation of the regulatory package.

-

The Government will ensure that Økokrim has better prerequisites, including increased capacity and new technology, including through the use of artificial intelligence, to deal with the increasing number of reports of suspicious transactions.

8.4.5 Cooperation to prevent and combat economic crime

Preventing and combating economic crime requires cooperation and coordination across different organisations and authorities. An important element in achieving this is the establishment of common standards and guidelines to ensure effective collaboration. As stated in chapter 4, there are several cooperation agreements and instructions between the police and various parts of the public administration that may be relevant to the fight against economic crime.

However, the cooperation has only focused on prevention to a limited extent. An exception here is the work-related crime cooperation, discussed in Box 8.2.

Textbox 8.2 Cooperation on work-related crime

The Norwegian Labour Inspection Authority, the Norwegian Labour and Welfare Administration, the police, and the Norwegian Tax Administration have established extensive cooperation at the national and regional level to prevent and combat work-related crime. Special work-related crime centres have been established in Oslo, Bergen, Stavanger, Kristiansand, Tønsberg, Trondheim, Bodø, and Alta, where the agencies are co-located. In addition, other partnerships have been established on work-related crime in regions and police districts not covered by work-related crime centres. The purpose of the work-related crime cooperation is to ensure that the agencies’ collective resources and sanctions are seen in context and utilised effectively. This will reduce the capacity and incentive of criminal actors to commit crime in working life.

In addition, the agencies cooperate to ensure that foreign workers are empowered to safeguard their rights and fulfil their obligations, and help ensure that clients and consumers do not facilitate work-related crime in the purchase of goods and services.

All the work-related crime centres have established knowledge groups whose main task is to build knowledge on trends, actors, environments, and methods. The knowledge products will provide decision-making support in order to be able to prioritise which actors and environments the interagency efforts should be directed at, select measures, and develop methodology.

A joint prevention strategy has also been drawn up for work-related crime that applies for the period 2020 to 2024, and in 2021 a joint interagency cooperation arena was established for the prevention of work-related crime.

In 2016, the Government established the National Interagency and Analysis and Intelligence Centre (NTAES) to strengthen efforts to combat economic crime, including work-related crime.26 The centre is a collaboration between the police, the Norwegian Tax Administration, the Norwegian Labour and Welfare Administration, the Norwegian Labour Inspection Authority, and Norwegian Customs (as required). The production of analysis and intelligence is regulated in regulations to the Police Databases Act and constitutes a separate police database.27

NTAES was evaluated by the Norwegian Agency for Public and Financial Management (DFØ) in the autumn of 2021, and the evaluation was assessed in a separate final report in the autumn of 2022.28 The evaluation clearly shows that there is support for the idea behind NTAES. It was pointed out that neither work-related crime nor economic crime can be solved without close interagency cooperation, which requires that the various agencies’ data sources be seen in context. The evaluation shows that there is a desire and need for expanded access to information sharing. The current legal basis prevents NTAES from sharing information about actors that would have been relevant to the police’s and control agencies’ work to prevent and combat crime.29

NTAE’s role and potential are also highlighted in KPMG’s evaluation report on the work-crime cooperation.30 In recommendation no. 7 in this report, it is stated that:

“NTAES has a unique opportunity to conduct analyses of threat scenarios and ensure professionalism and continuity in analysis and reporting on work-related crime. It is recommended that NTAES be assigned a clearer strategic role in overall knowledge building on work-related crime and economic crime.”

As part of the follow-up of the evaluation, work has been initiated to strengthen and clarify the knowledge work in both the agencies and at the work-related crime centres.

A lack of or varying legal basis for the publication of inspection reports and other material that may have a preventive effect can also be a challenge. It may be considered whether there is a need for a more uniform legal basis for the publication of reports and the like, which means that one can cooperate on preventive efforts.

Figure 8.3

Photo: Henry & co

The Government’s assessment

In the Government’s view, it is necessary for the authorities to give greater attention to and have a comprehensive approach to both intelligence and the prevention of economic crime, cf. the summary of the challenges in chapter 5.

To succeed in preventing and combating economic crime, it is a prerequisite that the agencies have a common knowledge base on threats and vulnerabilities. With a common knowledge base, it will be possible to prioritise effective threat and vulnerability reduction measures, and agree on an appropriate division of labour.

The Government believes that interagency intelligence cooperation is crucial for the preparation of a sound basis for decision-making. The interagency cooperation provides a basis for a broader supply of information, as well as the sharing of intelligence products, working methods and effective instruments.

The recommendations in the reports by DFØ and KPMG provide a good starting point for further development of both NTAES and the work-related crime cooperation. The police and control agencies’ intelligence in the field of economic crime should point to areas with particular potential for effective prevention and crime fighting. The intelligence should provide descriptions and assessments that are suitable for setting preventive objectives and developing preventive strategies and preventive measures.

It should also be possible to share intelligence to a greater extent with other public agencies and with the private sector in order to prevent crime. Section 59-7 of the Police Databases Regulations provides a legal basis for NTAES to share information in the form of national threat and risk assessments and intelligence products, but does not allow for the sharing of assessments related to individual actors with the police and the control agencies.

-

The Government will examine the need for amendments to the Police Databases Regulations in order to be able to share more information from the National Interagency Analysis and Intelligence Centre (NTAES), and also consider whether intelligence products can be used to a greater extent to establish common objectives for preventive efforts.

8.5 Need for and opportunities for information exchange between regulatory agencies and the police

The Regulations relating to the Sharing of Confidential Information and the Processing of Personal Data etc. in the Interagency Cooperation Against Work-Related Crime (the Work-related Crime Information Regulations) entered into force in June 2022. The regulations give the agencies participating in the work-related crime cooperation greater access to the sharing and compilation of information. In their joint annual report for 2022, the agencies state that work is underway on a data protection impact assessment with a view to implementing new regulations in the agencies’ common IT systems, and that this work is a prerequisite for achieving the opportunities for the increased sharing and processing of confidential information that the new regulations allow. A revised guide on information sharing has also been prepared for use by the agencies in the work-related crime cooperation.

The agencies’ assessment is that the new regulations provide a clearer and better legal basis, which will help to strengthen common situational awareness and make it easier to arrive at priorities for measures and the use of policy instruments. Continuous assessments and learning are taking place with regard to the regulations on information sharing.

There is a close connection between social dumping and work-related crime and other forms of economic crime. However, the legal basis for information sharing provided in the work-related crime information regulations for combating such crime is limited to the work-related crime and is therefore not sufficient in the efforts against economic crime in general.

The Government’s assessment

There is a need to detail the sharing and compilation needs that exist, and what may prevent the sharing and processing of information across agencies. Employees in various agencies that work to prevent and combat economic crime find it challenging to comply with the current regulations and get an overview of what is and what is not permitted. The privacy policy sets strict requirements for what personal data can be processed by whom and how it can be processed. Information collected for one purpose cannot automatically be used for other purposes.