4 Commercial and social importance of the Norwegian Sea

4.1 Value creation in industries associated with the Norwegian Sea

4.1.1 Fisheries, aquaculture and safe seafood

For centuries, fisheries have been a key source of income and the foundation for culture along the coast, and today Norway is one of the world’s largest exporters of seafood from capture fisheries and aquaculture. It is also a major supplier of technology and knowledge-based services for this sector. Statistics show that exports of Norwegian seafood increased in 2008, to a total of 2.3 million tonnes and a value of NOK 3.9 billion. 1 Employment in this sector declined until 2006, but since then the trend seems to have levelled off and stabilised. One of the most important reasons for the success of this sector, and a precondition for future growth, is Norway’s sustainable management of these natural resources and maintenance of clean, productive sea areas.

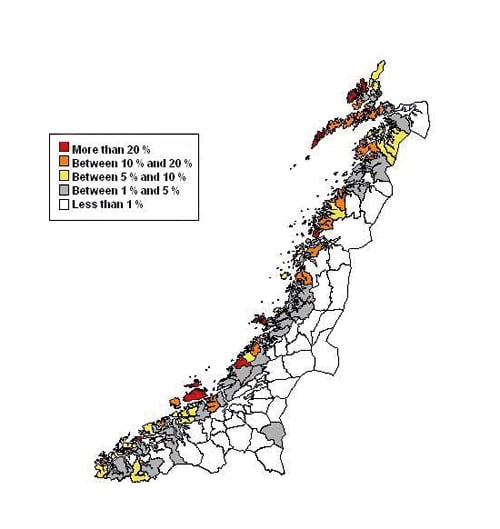

For a number of small settlements along the coast of the Norwegian Sea, the marine sector is the most important industry in terms of settlement and employment, see Figure 4.1. In its broadest sense, the sector comprises fisheries and aquaculture, which includes everything from fish farming, whaling and sealing to manufacturing and export activities and marine services and suppliers.

Figure 4-1.EPS Employment in fishing, fish farming and fish processing in 2007 as a percentage of total employment in the counties of Møre og Romsdal, Sør-Trøndelag, Nord-Trøndelag and Nordland.

Source Ministry of Local Government and Regional Development, based on figures from Statistics Norway

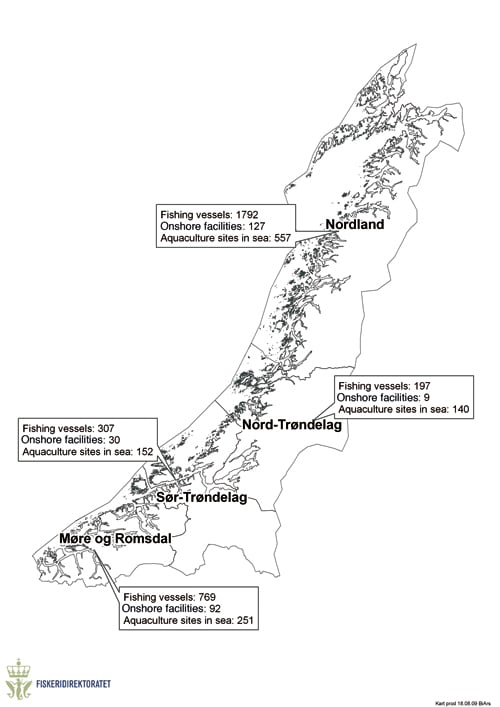

The four counties bordering on the Norwegian Sea account for a major share of Norway’s total activities in this sector. In 2007 approximately 44 % of vessels were registered in one of these four counties. Figure 4.2 gives an overview of the number of vessels, onshore facilities and approved aquaculture sites in Møre og Romsdal, Sør-Trøndelag, Nord-Trøndelag and Nordland.

Figure 4-2.EPS Number of vessels, onshore facilities and approved aquaculture sites in the counties bordering on the Norwegian Sea.

Source Directorate of Fisheries

Of the four counties bordering on the Norwegian Sea, Møre og Romsdal and Nordland have the largest numbers of people employed in fishing and aquaculture.

Table 4.1 Employment in the fishing fleet, aquaculture and fish processing by county in 2007

| Møre og Romsdal | Sør-Trøndelag | Nord-Trøndelag | Nordland | Total | |

|---|---|---|---|---|---|

| Fishing fleet | 2 723 | 509 | 318 | 3 183 | 6 733 |

| Fish farming | 647 | 410 | 347 | 727 | 2 131 |

| Fish processing | 2 084 | 979 | 352 | 2 246 | 5 661 |

| Total | 5 454 | 1 898 | 1 017 | 6 156 | 14 525 |

Source Statistics Norway

Commercial importance of fishing and aquaculture – spin-off effects

A study of the spin-off effects of this industry conducted in 2008 showed that in 2006 fishing and aquaculture in Norway accounted for a total of 43 375 person-years. 2 The industry contributed NOK 38.9 billion to the gross domestic product (GDP) and had a production value of NOK 101.7 billion. 3 This amounted to approximately 1.8 % of both Norway’s GDP and total employment in the country.

The core activities in fishing and aquaculture (fishing, fish farming, fish processing and wholesaling) accounted for 22 600 person-years. Core activities in the whole country contributed NOK 23 billion to GDP, with a production value of NOK 63 billion. In addition, the spin-off effects of the industry represented 20 600 person-years, a contribution to GDP of NOK 15.9 billion and a production value of NOK 38.7 billion. The sums are more or less equally divided between the direct effects for subcontractors and the indirect effects on the business sector in general.

In total, fishing accounted for 13 200 person-years in 20069, 9 700 of which came from core activities. Fish farming accounted for a total of 12 500 person-years, approximately 27 % of which came from core activities, while the rest were accounted for by spin-off activities. Fish processing accounted for approximately 12 400 person-years, 8 200 of which came from core activities.

Textbox 4.1 Lovund – swimming against the current

While a number of small settlements along the coast are suffering from depopulation and closures, Lovund is experiencing the opposite. This small island in the outer skerries off the coast of Helgeland has doubled its population since 1970, and in 2007 had a permanent population of approximately 390. The average age is under 30 and childcare facilities have had to be expanded in recent years. Local enthusiasm and fish farming are among the main reasons for this trend. The industry is highly structured and this, together with local patriotism and the determination of the local population, has enabled the community to do well throughout the recent economic fluctuations. A number of up-to-date businesses associated with fish farming have been built up over the last couple of decades: fish from fish farms over a large area are slaughtered on the island, packed in locally produced Styrofoam boxes and loaded onto locally produced pallets before being exported to many different parts of the world. The fishing village is considered one of the most attractive on this coast, the surrounding landscape is magnificent and there are opportunities for canoeing, puffin-watching and mountain hikes. Facilities include visitors’ berths, accommodation in fishermen’s cabins and a centre for coastal culture.

The total contribution to GDP from fisheries was approximately NOK 10.8 billion in 2006, approximately NOK 7 700 billion of which came from core activities in the fishing fleet. The contribution of fish farming to GDP in 2006 was approximately NOK 13.8 billion, approximately NOK 7.3 billion of which came from activities associated with hatcheries and fish farms.

In 2006 fish farming contributed NOK 10.2 billion to GDP, and wholesaling NOK 3.1 billion.

Risks to the reputation of Norwegian seafood

The seafood industry in Norway has built up a good reputation thanks to the cold clean waters off the coast, and Norwegian seafood is marketed in over 20 important seafood markets as a healthy, safe, high-quality food. One condition for continuing this favourable trend is that Norway manages its natural resources sustainably and maintains clean and productive sea areas.

A survey conducted in 2008 showed that consumers in the most important Norwegian seafood markets attach great importance to safe, secure food. Pollution of various kinds in the sea and coastal zone could cause consumers to question whether fish from the Norwegian Sea is safe to eat or to use as raw material for feed. Spills of oil, radioactive waste or pollutants from petroleum activities or maritime transport, or other accidents could also threaten the reputation of Norwegian seafood. The level of environmentally hazardous substances in fish can also be affected by long-range transboundary transport of pollutants. For some substances it takes only a small increase to have a negative impact on seafood safety and reputation. Other factors that are directly or indirectly related to the operation of fish farms, such as disease and escapes, will also have a substantial impact on the future development of the industry. In order to ensure seafood safety in Europe, the EU has set limit values for a number of priority substances, which also apply in the EEA. Thus it is important to survey and document the status of Norwegian wild fish stocks in terms of limit values and seafood safety in both domestic and external markets. Such work is extensive and resource-consuming, and in order to obtain adequate data, baseline studies of the most important commercial species have been started.

4.1.2 Petroleum activities and wind power

Petroleum resources in the Norwegian Sea

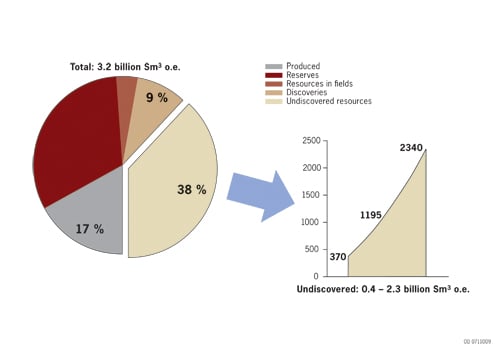

A total of 2.0 billion standard cubic metres of oil equivalents (Sm3 o.e.) has been proven in the Norwegian Sea, 0.6 billion of which has already been produced. The remaining recoverable reserves amount to approximately 1.0 billion Sm3 o.e., 66 % of which is gas. Contingent resources and discoveries amount to 0.4 billion Sm3 o.e. In 2008 the total volume of petroleum production in the Norwegian Sea was 64 million Sm3 o.e. Nine new discoveries have been made in the Norwegian Sea, most of which contain gas. Undiscovered resources in the area are estimated at 1.2 billion Sm3 o.e. (expected value). The Norwegian Petroleum Directorate estimates total discovered and undiscovered resources on the Norwegian continental shelf at approximately 13 billion Sm3 o.e. «Resources» is a collective term for all technically recoverable quantities of petroleum. The resource accounts include all resources on the Norwegian continental shelf, including those in areas that are not currently open for petroleum activities. The estimates do not include the area of overlapping claims in the Barents Sea or the continental shelf around Jan Mayen.

Figure 4-3.EPS shows the distribution of estimated resources in the Norwegian Sea, including a range of uncertainty for undiscovered resources.

Source Norwegian Petroleum Directorate

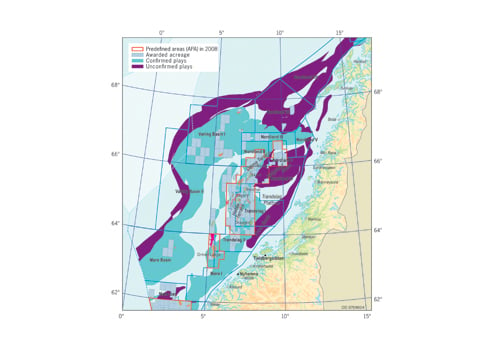

Relatively shallow areas of the Norwegian Sea – the Trøndelag Platform, the Halten and Dønn Terraces and the area along the Møre coast – have been gradually opened for petroleum activities since 1979. The first exploration well was drilled in 1980 and the first discoveries were made on the Halten Terrace in 1981. The deep-water areas in the Møre and Vøring Basins were opened for petroleum activities in 1994. As of 2009, 166 exploration wells have been drilled in the Norwegian Sea. Estimates of remaining reserves have increased as a result of reserve upgrades in several of the fields in the Norwegian Sea.

Figure 4-4.EPS Overview of plays and petroleum activities in the Norwegian Sea.

Source Norwegian Petroleum Directorate

Activity has been greatest on the Halten and Dønn Terraces off Sør-Trøndelag, Nord-Trøndelag and Nordland. Most of the discoveries and almost all the developed fields are to be found in this area. The Draugen field was the first in the Norwegian Sea to be developed, and production started in 1993. To begin with, exploration activities concentrated on oil, but since gas transport infrastructure was established there has been growing interest in exploration for gas. The Halten and Dønn Terraces are the most mature area and also the area where the largest remaining undiscovered resources are expected to lie.

Large parts of the Møre and Vøring Basins have a depth of more than 1000 m, which initially proved an obstacle to petroleum activities. There was considered to be a high likelihood of gas discoveries in this region, and in 1997 the gas field Ormen Lange, in the eastern part of the Møre Basin, was discovered.

Exploratory drilling in deep-water areas has mainly resulted in gas discoveries. There has been little exploration in the most westerly parts of the deep-water areas, and resource estimates are very uncertain.

Small petroleum discoveries have been found along the Møre coast and further small to medium-sized discoveries are expected to be made near shore off the coast of Møre og Romsdal and the northernmost part of Sogn og Fjordane.

There has been very little exploration activity in the nearshore areas known as the Froan Basin off Nord-Trøndelag and the Helgeland Basin off Nordland. It may be possible in the future to refine gas from coal-bearing formations in more nearshore areas of the Trøndelag Platform.

Textbox 4.2 Lessons learnt from activities in the Norwegian Sea

As licences are granted for blocks further and further north on the Norwegian continental shelf, the local and regional spin-off effects are becoming increasingly marked.

In 2006 Møreforsking Molde conducted a survey of employment in petroleum-related industries and estimated this at 25 700 person-years altogether in Møre og Romsdal. The maritime business cluster accounted for the largest share of person-years: 11 500. Since the early 1970s, the maritime industry has grown to become an international industry with an export share of 70 % and is considered to be extremely innovative. It has become less dependent on activities on the Norwegian continental shelf.

There are over 100 major suppliers to the petroleum sector, and their petroleum-related turnover was approximately NOK 3.6 billion in 2008, a growth of 53 % since 2005. Employment ncreased by 85 % in the same period, to 2 130 person-years. The total spin-off effect on employment of petroleum-related activities in the Kristiansund region is estimated at just over 3 500 person-years in 2008, as compared with 2 000 person-years in 2005.

Figure 4-5.EPS Ormen Lange

Source StatoilHydro (Photo: Eilev Leren, StatoilHydro)

In recent years the increase in suppliers of technical services has been particularly large, which has resulted in a strong growth in knowledge-based jobs in this region.

The development of the Ormen Lange field in the Norwegian Sea is one of the largest and most complicated industrial projects that has ever been carried out in Norway.

Gas from the Ormen Lange field, which is about 100 km north-west of Kristiansund in the Norwegian Sea, is piped through two multiphase pipelines to Nyhamna on the island of Gossa in Møre og Romsdal. The gas is processed for export through Langeled, a 1200-kilometre long transport pipeline, to the reception centre in Easington on the east coast of England. Langeled is the world’s longest offshore gas pipeline. Production started in October 2007 and the field will be able to meet up to 20 % of UK gas demand for up to 40 years.

Møreforsking has estimated the value of contracts for Ormen Lange at NOK 38 billion. The Norwegian share was estimated at 70 %, 11.5 % of which was accounted for by companies in Central Norway. The value of contracts that went to this region during the development phase was NOK 3.2 billion, a great deal higher than was estimated in the impact assessment for the project. Møreforsking estimated the total spin-off effects at NOK 400 million in addition to locally-awarded contracts. The study also emphasised that development of the field has increased the competence of local suppliers.

Small to medium-sized oil or gas discoveries can be expected on the Trøndelag Platform (especially the Halten Terrace), and it is still possible that large gas discoveries will be made in the Møre and Vøring Basins.

The continental shelf around Jan Mayen is a completely new exploration province, where little is currently known about the geological conditions. More seismic data are required, and shallow core drilling should be undertaken to assess the possibilities. Areas likely to contain petroleum resources extend into the waters around Iceland, and the Icelandic authorities have announced a licensing round for blocks in their waters.

Commercial activities associated with the petroleum industry

Today the petroleum industry is well established in the Norwegian Sea, with substantial national, regional and social spin-off effects. The industry is extremely profitable for Norway as a whole. The sales value of petroleum deposits in the Norwegian Sea for 2007 was approximately 2006 NOK 125 billion, and total employment in petroleum-related activities in 2007 was estimated at approximately 25 000 person-years.

The revenues from petroleum activities in the Norwegian Sea in the period up to 2025 are estimated at NOK 2 240 billion, with a net cash flow of NOK 1 370 billion. This equals an annual net cash flow of between NOK 50 million and NOK 100 million. Petroleum activities on the Norwegian continental shelf have resulted in the development of a substantial petroleum-related supply industry that employs a large number of people. The Norwegian continental shelf is an important market for this industry, and provides many opportunities for petroleum companies and suppliers to develop new technologies that can be sold on the international market. Further investment in petroleum activities in the Norwegian Sea would stimulate value creation and employment in the petroleum-related supply industry and in the Norwegian economy as a whole.

Petroleum activities in the Norwegian Sea are expected to create 25 000–40 000 person-years of employment in the country as a whole during the period 2007–2025. This includes jobs in supplier industries and spin-off effects in the form of jobs in these companies’ subcontractors and in suppliers to these subcontractors. At the regional level the average annual effect on employment is estimated at 4000 person-years, gradually increasing during the management plan period. It is important to provide good conditions for further development that will result in positive local and regional spin-off effects in the form of jobs, expertise and supplier industries.

Estimates of the effects on the broader Norwegian economy of petroleum activities in the Norwegian Sea indicate that the supply of Norwegian goods and services will amount to NOK 283 billion (at 2006 prices) in the period 2007–2025. At the national level, supplier industries are expected to account for 60 % of total investment (6 % of which will be regional) and 88 % of the operations and maintenance market (30 % of which will be regional). This shows that Norwegian offshore-related industries are already very competitive and this situation is expected to continue in the time ahead. It also shows that the operational phase is the most important in terms of the regional business sector, while investment in activities in the Norwegian Sea is important for maintaining service and supplier industries in the rest of the country.

Commercial activities associated with wind power production

Wind power production is a sector with strong growth internationally, and over the last 10 years installed wind power capacity has increased by almost 30 % per year worldwide. At present the majority of wind farms are onshore.

The development of offshore wind farms is substantially more costly and technically more complex than onshore development. However, the limited availability of suitable onshore sites is expected to result in an increase in offshore development. The technical and cost-related problems may to some extent be compensated for by the stronger wind resources at sea, and the fact that it will be possible to build larger wind turbines offshore than onshore.

At present existing and planned offshore wind farms are mainly based on fixed installations in shallow water, i.e. with a typical depth ranging from 10–30 m to approximately 50 m. Wind power can be exploited to a much greater extent if turbines are built in deeper water. This applies particularly to Norwegian waters. The theoretical potential for the development of offshore wind power at depths of up to 60 m in Norwegian waters is estimated at approximately 800 TW/year, and the theoretical potential for depths of 60–300 m is estimated at approximately 13 000 TW/year. Reliable and competitive floating wind power technology is necessary for development at greater depths, but it is not clear when such technology will be sufficiently mature. These projections are based on the assumption that no large-scale developments of wind power at greater depths will be undertaken during the management plan period and that large-scale developments of wave power are unlikely to be undertaken during this period.

A number of other factors also influence where and to what extent large-scale offshore wind farms are likely to be built in Norwegian waters. Wind resources and the need to develop infrastructure for the transmission of power to land and increase the capacity of the onshore grid are critical factors here. The projections include overall estimates of these factors. The development of wind farms in the area of the management plan is expected to take place off the coast of Central Norway. It is believed that fixed wind installations can be built in this area without the necessity for constructing new large transmission lines on shore. It is considered fairly unlikely that wind farms will be established further north during the management plan period. This is partly because grid capacity is limited and partly because there seems to be considerable potential for developing renewable energy infrastructure onshore in this area with acceptable impacts on the environment and the community.

There is considerable potential for industrial development in the onshore and offshore wind farming sector in the Norwegian Sea region, especially Central Norway. In addition to good wind resources, a large number of businesses associated with the maritime and oil and gas industries are located in the region, and their expertise could be transferred to the wind power industry. For example, the development of wind power offshore will require dedicated vessels designed for assembling and maintaining wind turbines. There are also a number of companies that produce wind power technology in the region, and two research centres have been established under the research organisation SINTEF for the purpose of developing new technology for offshore wind power generation. The supplier network for oil and gas (LOG) is developing networks in the wind power sector, partly as a result of demand by wind power developers.

4.1.3 Shipping

Maritime transport is in general safer and more environmentally friendly than road transport, and the Government is seeking to ensure that more traffic is transferred from road to sea. Ship traffic in the management plan area is related to commercial activities, and the volume of maritime transport is determined by the settlement patterns and industrial structure along the Norwegian Sea coastline and north of the management plan area. Shipping has always been a key determinant of settlement along the coast. It transports goods and passengers, and is a source of jobs and a commercial activity in its own right. There are great variations in the volume of traffic in the Norwegian Sea. Ship traffic intensity is particularly high along the coast between Røst and Stad, while traffic in the rest of the Norwegian Sea is small compared with the coastal traffic.

Figure 4-6.EPS Ship traffic in October 2008, based on AIS data.

Source Norwegian Coastal Administration

In 2006 about 18 300 vessels, including fishing vessels, passed Stad. Cargo ships accounted for 59 % of the traffic and tankers for 17 %. Twenty per cent of the tankers were large, with a gross tonnage of over 50 000.

Table 4.2 Numbers of calls at the largest ports relevant to the management plan area in 2007

| PORT | NO OF CALLS 2007 |

|---|---|

| Ålesund | 3 662 |

| Molde and Romsdal | 2 381 |

| Kristiansund and Nordmøre | 5 571 |

| Trondheimsfjorden interkommunale | 1 584 |

| Indre Trondheimsfjord | 929 |

| Brønnøy | 455 |

| Mo i Rana | 1 139 |

| Bodø | 1 706 |

| Narvik | 585 |

| Tromsø | 2 048 |

| TOTAL | 20 060 |

Source Statistics Norway

The volume of shipping is influenced by general economic developments in Norway and in the rest of the world. The expansion of petroleum activities in northwestern Russia, in the Norwegian Sea and in the Barents Sea will lead to growth in ship traffic through the Norwegian Sea. The strong economic growth up to 2008 has also resulted in growth in the maritime transport and other maritime industries.

The numbers of calls at selected large ports also give an indication of the volume of ship traffic in the area.

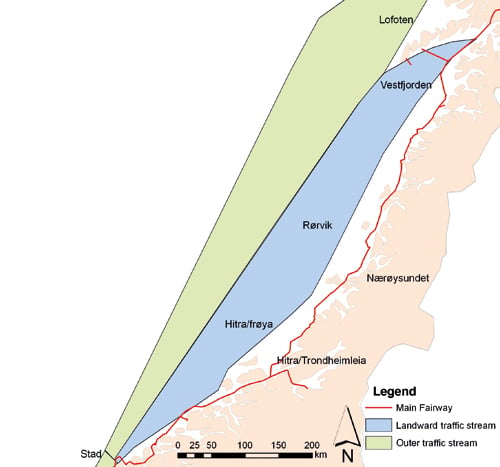

Ships that load and unload at Norwegian ports along the coast of the Norwegian Sea, whether they are sailing northwards or southwards, normally sail in the main fairway or the landward traffic stream (see Figure 4.7). The largest volume of traffic is north to Trondheim, and there is a larger volume of traffic in the main fairway than in the landward traffic stream.

Cargo ships, most of them with a gross tonnage of less than 5 000, account for 67 % of the traffic in the main fairway. Hurtigruten, other passenger vessels, ferries and cruise ships account for about 18 % of the traffic in the main fairway, but only make up 2 % of the landward traffic stream along the mainland coast. Hurtigruten accounts for most of the ship passages by passenger vessels in this size category. Few vessels with a gross tonnage of over 10 000, apart from passenger ships, sail in the main fairway past Rørvik.

Textbox 4.3 Sailing patterns and traffic density

Shipping in the management plan area follows four main patterns.

The main fairway

The main fairway is in Norway’s internal waters, and runs through both sheltered and exposed waters.

Traffic along the mainland coast in the open sea that does not follow the main fairway

This can be divided into traffic streams (landward and outer), depending on whether the ships sail inside or outside a line drawn between Stad and Røst.

Seagoing routes

These are followed by vessels that do not sail along the coast, generally ships in international traffic.

Offshore traffic

This refers to traffic to offshore installations, which crosses the main north–south traffic streams along the mainland coast.

Figure 4-7.EPS The main fairway and the landward- and outer traffic streams along the mainland coast.

Source Norwegian Coastal Administration

Cargo ships, most of them with a gross tonnage of 1 000 to 5 000, make up 83 % of the landward traffic stream along the mainland coast. In contrast to the traffic in the main fairway, the number of relatively small vessels (gross tonnage less than 1 000) is insignificant.

Most of the outer traffic stream in the open sea along the mainland coast consists of cargo ships and tankers that are sailing past the management plan area. North-going ships in the outer traffic stream pass relatively close to Stad in the south, while their routes begin to spread outwards towards the Lofoten and Vesterålen Islands. Ships calling at Russian ports account for about half the total volume of traffic, and most of these are cargo ships and tankers. Tankers calling at Russian ports are usually large, most of them with a gross tonnage of more than 25 000.

Through the IMO, Norway has adopted routeing measures off the coast of North Norway between Vardø and Røst as from 1 July 2007, which consist of a series of traffic separation schemes joined by recommended routes. The measures apply to tankers of all sizes and cargo ships in international traffic with a gross tonnage of more than 5 000. These measures have altered the sailing patterns of a considerable number of ships in the management plan area, which now have to revise their routes to take account of the traffic separation schemes. Ships from the North Sea on their way to the Barents Sea now pass close to the coast at Stad, after which they head for the traffic separation scheme off Røst.

Seagoing routes lie further out to sea than the route followed by the outer traffic stream along the mainland coast and generally do not run parallel with the Norwegian coast. These routes cover a large area and have a relatively small volume of traffic. Figures from the COAST database show that almost 800 vessels a year sail this part of the Norwegian Sea. The traffic consists of ships sailing to and from Svalbard and between Iceland and ports north of Mo i Rana. Traffic from ports on the west coast of England sail west of Shetland to Russian and North Norwegian ports or the oil platforms in the Norwegian Sea. This only accounts for a very small part of the total volume of traffic in the management plan area.

There are currently 12 oil and gas fields on stream in the Norwegian Sea. Gas is transported from the fields by pipelines and oil in tankers. The installations depend on regular supplies from land, and ships from the main supply bases sail along fixed routes to and from the fields. There are two main supply bases for the Norwegian Sea: Kristiansund and Sandnessjøen. Approximately 600 sailings per year deliver supplies to these installations, crossing the north–south traffic flows. There is also shuttle tanker traffic to and from oil platforms. In 2006, 238 cargoes of crude oil were shipped from the installations in the Norwegian Sea.

The movements of fishing vessels in the management plan area depend on where fishing is taking place, on the fishery and on the season. Much of the activity of the smaller fishing vessels naturally takes place within a reasonable distance from the closest port where the fish can be sold. The activity of the seagoing fishing fleet is less influenced by where the vessels deliver their catches, since these vessels have a greater action radius than the small vessels. From August until the end of the year, most Norwegian and foreign fishing vessels sailing to and from the herring fishing grounds in the Norwegian exclusive economic zone are to be found in the sea areas and fishing banks west and north-west of Troms and around the Lofoten and Vesterålen Islands. In January the site of activity changes, since the herring begin their spawning migration southwards towards the Møre banks. Fishing on these banks ceases at the end of February or at the latest by mid-March. Generally traffic from these fisheries is mainly to and from the onshore facilities at Værøy, Svolvær, Lødingen, Bodø, Træna, Uthaug, Ellingsøy, Harøysund and Måløy, but also to those south and north of the management plan area. From January to the end of April a great many trawlers and vessels fishing with conventional gear sail to and from the fisheries and between fishing grounds. During these months most of the activity takes place around the Lofoten and Vesterålen Islands and on the Halten and Møre banks. The largest volume of fishing vessel traffic for the year as a whole is generally to and from the Møre banks. Traffic to and from other fisheries in the management plan area, both in coastal waters and in the open sea, is more sporadic.

Commercial activities associated with shipping

Norway’s connection with the sea has for centuries been a source of commercial activities in the shipping and fisheries sectors. Today Norway is the fifth largest shipping nation in the world. The Norwegian commercial fleet consisted in 2007 of 1 314 ships, 746 of which were registered in the Norwegian Ordinary Ship Register (NOR). 4

Since shipping is an international industry it is difficult to estimate how much Norwegian shipping activity is included in maritime activities in the counties in the management plan area. However it is estimated that about 70 % of the tonnage in Norwegian waters at any time is Norwegian owned. 5

The growth of the commercial fleet has led to a parallel growth in the land-based maritime industry. Natural conditions in many places along the coast are suitable for shipyards, which for many years dominated commercial activities in this sector.

Norwegian shipping operates in most shipping markets and occupies a leading place worldwide in a number of offshore markets such as the rig and supply markets.

Petroleum activities stimulate innovation among land-based maritime industries. Shipyards build both vessels and installations for the offshore industry, and these activities in turn provide a market for subcontractors, service deliverers and other related industries. This is an important part of the Norwegian maritime cluster, which includes companies all over the country and has groups of segments in different parts of the country.

Maritime industries are capital-intensive, which makes them vulnerable to macroeconomic fluctuations. After many years of economic expansion the maritime industries have experienced strong growth, apart from the shipbuilding industry, where profitability has been poor in spite of the favourable economic climate. The financial crisis will worsen conditions for many companies, and cutbacks and restructuring will become increasingly necessary in the course of 2009 and 2010.

The maritime sector in Møre og Romsdal is large, with a total of about 170 companies, including shipyards, service deliverers, producers of equipment and shipping companies. These companies have a total turnover of approximately NOK 25 billion a year and employ 13 000 persons. The sector is largely targeted at offshore activities and the different parts of the sector are closely interrelated; for example many of the shipyards and equipment producers supply local shipping companies. This close relationship results in a high degree of innovation and high-quality products, and the sector occupies a leading position worldwide.

An analysis conducted by the consulting company Menon Business Economics showed that value creation in the maritime sector in Møre og Romsdal in 2005 amounted to just under NOK 8 billion, of which 40 % was contributed by shipping companies, 34 % by equipment producers, 18 % by shipyards and 8 % by service deliverers. 6

According to the analysis, the key maritime institutions in Sør- and Nord-Trøndelag were the Norwegian University of Science and Technology and the research institute MARINTEK at SINTEF. The shipbuilding industry and the offshore sector, both Norwegian and foreign, make use of MARINTEK’s expertise and ocean laboratories for testing new vessels. The Ministry of Trade and Industry has made a commitment (NOK 8 million) to a pilot project for developing the next generation of maritime research and innovation centres (the World Ocean Space Center). There are 180 maritime companies in Sør- and Nord-Trøndelag, and value creation in the maritime industry is equally divided between four main groups: equipment producers, shipyards, shipping companies and service deliverers.

The maritime sector in North Norway consists mainly of fisheries, and owners of fishing vessels are the largest contributors to value creation. Equipment suppliers and maritime service deliverers each accounted for 23 % of value creation in this sector in 2006, shipping companies for 47 % and the shipbuilding industry for 7 %. 7 The largest single company in the sea transport sector is Hurtigruten, with a turnover of NOK 3.8 billion in 2007. 8

One of the objectives of the Government’s maritime strategy is that Norwegian shipping should become a more environmentally friendly and more competitive alternative to road transport, enabling a larger volume of goods to be transported by sea. The strategy has five priority areas: globalisation and national policies; environmentally sustainable maritime industries; maritime competence; maritime research and innovation; and short sea shipping. The strategy contains 54 measures, and a progress report will be delivered in spring 2009. The environment is a maritime research and innovation area that has especially high priority.

4.1.4 Tourism

The magnificent scenery along and off the Norwegian coast already attracts large numbers of tourists. Tourism in the management plan area is based on the natural environment – a rich resource that unlike many other resources is difficult to measure in terms of money. Viable coastal communities and the spectacular scenery are tourist attractions in themselves, and value creation in the tourist industry therefore depends on maintaining rich, clean sea areas. Tourists are attracted to the area by the possibilities it offers for fishing, eating fresh seafood and observing marine mammals and seabirds. Hurtigruten is one of Norway’s best-known brand names abroad, and the route along the coast is an experience that has been described as «the world’s most beautiful sea voyage». This means that the environmental value of the seas is essential to tourism in the coastal zone.

The tourist industry covers a wide range of activities and sectors, a large proportion of which involve sales to travellers. Transport, accommodation and restaurant services, travel and tour companies, and companies offering attractions and activities of various kinds are all part of the tourist industry.

Tourism is a strongly expanding industry both in Norway and internationally. Few countries have as long and varied a coastline as Norway, and the coast and fjords have great potential in terms of tourism. Encouraging tourist industries promotes development in coastal communities and creates new, interesting jobs that can halt or limit the depopulation that is depleting many coastal municipalities.

The coast is also an important element in the Government’s tourism strategy, which was launched on 18 December 2007, and the coast and coastal culture are a key element in Innovation Norway’s branding strategy for promoting Norway as a tourist destination. The number of sports fishermen visiting Norway has increased enormously in the last few years, and it is estimated that foreign sports fishermen bring in over NOK 3 billion a year. In 2007 Innovation Norway therefore launched a campaign promoting coast and deep-sea fishing that targeted specific markets. However, such initiatives must be weighed against the impacts of the resulting pressure on fish resources. Sports fishing results in a substantial harvest of coastal species, even though foreign tourists are only permitted to fish using a rod and handline. The efforts of the Government and Innovation Norway, together with other efforts such as the development of national tourist roads and measures under the Government’s action plan for coastal culture, will all have an impact on the tourist industry in the coastal zone of the management plan area; for example five out of 18 national tourist roads that are being developed or planned are in this area (Andøya, Lofoten, Helgelandskysten Nord, Helgelandskysten Sør and Atlanterhavsvegen). One of the main measures in the Action Plan is to promote enthusiasm and spread knowledge about the cultural heritage along the coast that can be used as a resource for value creation in tourism and other sectors.

4.2 Population, employment and value creation in the counties bordering on the Norwegian Sea

4.2.1 Population and settlement

On 1 January 2007, Møre og Romsdal had a population of just over 245 000, well over half of whom lived in settlements along the coast. The population has been increasing steadily over a long period, with the strongest growth along the Sunnmøre coast. Much of the value creation in Møre og Romsdal takes place in the coastal zone, which has a long historical tradition of commercial activity based on the Norwegian Sea, predominantly fisheries and shipping. These have now been supplemented by other industries in the coastal zone; for example, the southern part of Møre og Romsdal has a large maritime sector. Shipbuilding and manufacturing of machinery and other equipment are now more important drivers of business development than fisheries. The maritime cluster in coastal Møre og Romsdal plays a leading role worldwide in the development, building and operation of technically advanced ships in the oil industry. There are also petroleum-related activities onshore in the county, such as the methanol plant on Tjeldbergodden and the processing plant for the gas field Ormen Lange at Nyhamna.

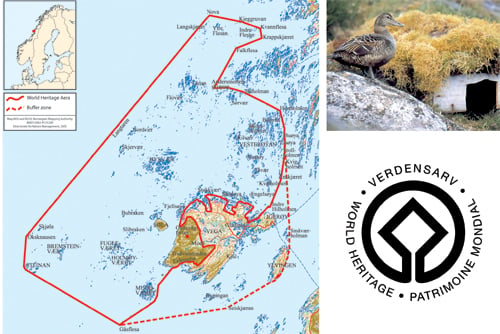

Textbox 4.4 The Vega Archipelago – UNESCO World Heritage site

The Vega Archipelago on the coast of Helgeland, Nordland, was inscribed on the World Heritage List (established under the Convention concerning the Protection of the World Cultural and Natural Heritage) in 2004.

In the justification for the inscription, it was emphasised that the Vega islands are a living cultural landscape that «reflects the way generations of fishermen/farmers have maintained a sustainable living» based on fishing and harvesting eider down. The islands have a particularly rich natural environment. Twenty-two per cent of the Archipelago is protected under the Nature Conservation Act (one protected landscape, four nature reserves and four bird reserves). The Planning and Building Act is the most important instrument for maintaining the environmental value of the rest of the archipelago. Two cultural monuments are protected by individual protection orders under the Cultural Heritage Act.

The Vega Archipelago covers 1037 km2, about 970 km2 of which is seascape. The rest consists of islands, islets and skerries. Fishing, farming and hunting have been practised there for the last 10 000 years, and since the Middle Ages the harvesting of eggs and down from wild eider ducks have become an important supplement to these activities. This sustainable livelihood, based on «the now unique practice of eider down harvesting», was emphasised in the justification for the inscription on the World Heritage List.

The World Heritage Convention does not specify any clear commitments with regard to protection of cultural properties. However, according to Articles 3 and 5, parties to the Convention are obliged to identify and protect their cultural and natural heritage, although the convention says little about legal protection under national law. The Operational Guidelines for the Implementation of the World Heritage Convention list the requirements that must be met when a property is nominated for inscription on the World Heritage List. These include «adequate long-term legislative, regulatory, contractual, planning, institutional and/ or traditional measures» to protect the property. There must also be a sound management plan or other management regime that safeguards the outstanding universal value of the property and ensures that it is not subject to development or changes that would have a negative impact.

The Norwegian World Heritage sites will be developed as leading examples of best practice in cultural heritage management. This will require a strict management regime, and a management plan for the Vega Archipelago has been developed for the period 2005–2010. Large areas of the seascape are shallow, with high species diversity and substantial biological and commercial resources. In the decision to inscribe the property on the World Heritage List, it was recommended that Norway should consider expanding the property to include a buffer zone consisting of islands and sea areas to the north and north-west.

Figure 4-8.EPS Vegaøyan – the Vega Archipelago – is a UNESCO World Heritage site.

Source Ministry of the Environment

On 1 January 2007, Sør-Trøndelag had a total population of almost 279 000 people, and the number continues to rise. The population is mainly concentrated in the five municipalities around Trondheim, where 72 % live today and which is the area of strongest growth. The coastal zone has a much smaller population, about 24 000 people distributed between eight municipalities, which is less than 9 % of the total population of the county. On 1 January 2007, Nord-Trøndelag had a total population of around 129 000 people. Most of them do not live in the coastal zone but in the lowland districts east of the Trondheimsfjorden. The coastal zone has a population of about 11 500 distributed between five municipalities, which is only 9 % of the population of the county.

In Sør-Trøndelag and Nord-Trøndelag the coastal zone is less important in terms of value creation than in Møre og Romsdal. Almost all the growth in population, value creation and employment in Sør-Trøndelag is concentrated in the Trondheim area. Fishing accounts for only a small part of the value creation in the county and there is little petroleum activity. Fish farming is a much more important sector than fishing. Land-based activities related to the petroleum industry are localised in Stjørdal. A great deal of maritime research is conducted in both Nord-Trøndelag and Sør-Trøndelag, at the University of Science and Technology and MARINTEK.

On 1 January 2007 Nordland county had a population of around 235 000. The numbers have been decreasing for the last 20 years, and in the last 10 years the county has experienced a population decline of almost 5000 a year. The decline is most marked on the islands and in small coastal municipalities that have no large urban centres. The only areas to experience population growth during this period are Salten and Bodø municipalities, and Bodø is by far the largest area of growth in the county. Today around 60 % of the population lives and works in the coastal zone. Of all the counties in the country, Nordland is the county with the largest number of fish farms and where the second largest quantity of fish is landed. This has substantial spin-off effects in other industries, especially the fish processing industry and service industries for the fishing fleet, but also for salmon-slaughtering plants, fish feed manufacturing plants and suppliers of equipment for fish processing. Currently there is little petroleum-related activity in Nordland but there are some supply/helicopter services from Sandnessjøen/Brønnøysund to the Norwegian Sea.

4.2.2 Employment

As regards petroleum-related employment on the continental shelf, the table only shows the number of people in the four counties employed in the extraction of crude petroleum and natural gas.

Of the four counties bordering on the Norwegian Sea, Sør-Trøndelag had the largest number of people employed in the fourth quarter of 2007, followed by Møre og Romsdal, Nordland and Nord-Trøndelag, in that order. Most of the employed are in the service industries, which corresponds to the figures for the country as a whole. According to Statistics Norway, employment in the secondary and tertiary industries rose by about 3 % in all four countries from 2006 to 2007. In Møre og Romsdal and Nordland the number of people employed in the primary industries declined. In Nord-Trøndelag employment in the primary industries remained unchanged, whereas in Sør-Trøndelag it rose by about 1.5 %.

Table 4.3 shows that in 2007, 130 681 persons were employed in Møre og Romsdal. Employment in the manufacturing and mining and quarrying industries was high in this county, at 18 %, as compared with approximately 10 % for the country as a whole. Roughly the same number of people worked in the health and social work sector as in the manufacturing and mining and quarrying industries. Wholesale and retail and hotels and restaurants accounted for 17 % of employment in the county. Employment was higher in fishing, fish farming and related services than the national average. From 2006 to 2007 employment declined by 3 % in the primary industries and rose by 4 % in the secondary and tertiary industries.

Table 4.3 Number of employed persons in the fourth quarter of 2007 by county and industry

| Møre og Romsdal | Sør-Trøndelag | Nord-Trøndelag | Nordland | |

|---|---|---|---|---|

| Total | 13 0681 | 15 0041 | 66 166 | 11 8384 |

| Agriculture and forestry | 3 804 | 4 806 | 5 257 | 3 669 |

| Fishing, fish farming and related services | 2 986 | 901 | 523 | 3 503 |

| Extraction of crude petroleum and natural gas | 1 465 | 1 656 | 442 | 626 |

| Manufacturing and mining and quarrying | 23 885 | 14 335 | 8 382 | 11 826 |

| Electricity, gas and water supply | 1 091 | 1 101 | 672 | 1 261 |

| Construction | 9 047 | 11 743 | 5 485 | 9 048 |

| Wholesale and retail, hotels and restaurants | 22 076 | 25 976 | 10 583 | 19 328 |

| Transport and communications | 10 363 | 8 546 | 3 975 | 9 296 |

| Financial services | 1 928 | 3 054 | 644 | 1 361 |

| Business activities, real estate | 9 201 | 18 812 | 4 479 | 7 745 |

| Public admin., defence, compulsory social security | 6 315 | 8 887 | 4 240 | 9 809 |

| Education | 9 344 | 14 721 | 5 641 | 10 540 |

| Health and social work | 24 692 | 29 176 | 13 533 | 25 803 |

| Other community, social and personal services | 3 973 | 5 845 | 2 073 | 4 178 |

| Unspecified | 511 | 482 | 237 | 391 |

Source StatBank, Statistics Norway

In 2007, 150 041 persons were employed in Sør-Trøndelag. Of these, 19 % were employed in the health and social work sector and 17 % in wholesale and retail, hotels and restaurants. Sør-Trøndelag had relatively more people employed in business activities (13 %) than the other three counties. Manufacturing and education accounted for about 10 % of employment in the county. According to Statistics Norway, from the fourth quarter of 2006 to the fourth quarter of 2007 employment in the primary industries rose by 1.5 % and in the secondary and tertiary industries by 4 %.

In 2007, 66 166 persons were employed in Nord-Trøndelag. Here too, many people were employed in health and social work (20 %) and wholesale and retail, hotels and restaurants (16 %). Manufacturing and mining and quarrying accounted for 13 %. The proportion of employed in agriculture, forestry and fishing (9 %) was about three times as high as the national average (3 %). Employment in the secondary and tertiary industries rose by 5 % from 2006 to 2007.

In 2007, 118 384 persons were employed in Nordland. The largest proportion was employed in health and social work (22 %) and wholesale and retail, hotels and restaurants (16 %); 10 % were employed in manufacturing and 3 % in fishing, fish farming and related services. A high percentage of the employed in Nordland worked in the public administration, defence and compulsory social security sectors (8 %) as compared with the national average (4 %). Nordland also had relatively high employment in fishing, fish farming and related services (3 %) compared with the national average (0.6 %). From 2006 to 2007, employment in the primary industries declined by 3 % and that in the secondary and tertiary industries rose by 6 % and 3 % respectively.

4.2.3 Value creation

Value added is often used as a measure of wealth creation. Value added is defined as the difference between the value of produced goods and services (production value) and the goods and services required to produce them (material input).

This overview does not include value creation on the continental shelf because the petroleum revenues are channelled directly to the state. The figures for value creation in the extraction of crude petroleum and natural gas industries in the four counties are based on tax revenues from company headquarters/onshore activities.

Table 4.4 shows that in 2005 value added for Møre og Romsdal was NOK 58 936 million, and GDP per employed person was NOK 589 788, as compared with the national average of NOK 618 674. Manufacturing is a major industry in Møre og Romsdal, and the value added from this industry is divided between manufacturing of machinery and other equipment (about 22 %), manufacture of food products, beverages and tobacco (16 %), shipbuilding etc. (14 %) and furniture and other manufacturing (14 %). The manufacture of basic metal and chemical raw materials accounted for about 10 % and 12 % respectively. Fishing, fish farming and related services includes fishing in ocean and coastal waters, processing on board fishing vessels and fish farming. Although this sector accounts for a relatively small proportion of value creation in the county (5 %), it represents about 24 % of total value creation in the sector at the national level.

Table 4.4 Value added by county and industry in 2005, base value. NOK million

| Møre og Romsdal | Sør-Trøndelag | Nord-Trøndelag | Nordland | |

|---|---|---|---|---|

| Total | 58 936 | 70 812 | 24 888 | 51 993 |

| Agriculture and forestry | 671 | 717 | 969 | 544 |

| Fishing, fish farming and related services | 3 035 | 445 | 305 | 2 483 |

| Extraction of crude petroleum and natural gas, including services | 103 | 470 | 254 | 0 |

| Manufacturing and mining and quarrying | 14 677 | 7 904 | 3 695 | 6 735 |

| Electricity, gas and water supply | 2 785 | 2 110 | 748 | 4 251 |

| Construction | 3 426 | 5 008 | 1 673 | 3 455 |

| Wholesale and retail, hotels and restaurants | 5 738 | 9 605 | 2 541 | 4 772 |

| Ocean transport | 310 | 51 | 11 | 15 |

| Transport and communications | 2 564 | 3 863 | 2 341 | 3 025 |

| Financial services | 1 964 | 4 195 | 567 | 1 498 |

| Business activities, real estate | 8 178 | 14 239 | 3 258 | 7 163 |

| Public administration and defence | 2 632 | 4 147 | 1 719 | 4 577 |

| Education | 3 606 | 6 333 | 2 119 | 3 946 |

| Health and social work | 7 571 | 8 947 | 3 853 | 7 781 |

| Other community, social and personal services | 1 676 | 2 777 | 837 | 1 747 |

Source StatBank, Statistics Norway

Value added for Sør-Trøndelag in 2005 was NOK 70 812 million, and GDP per employed person was NOK 586 549. The industries that contributed most to value creation in Sør-Trøndelag were business activities and real estate (20 %), health and social work (13 %), wholesale and retail, hotels and restaurants (14 %), manufacturing and mining and quarrying (11 %) and education (9 %). The proportions of value added contributed by the different industries are very similar to those at national level.

Total value added for Nord-Trøndelag in 2005 was NOK 24 888 million, and GDP per employed person was NOK 499 046, which is considerably lower than the national average. The five industries that accounted for most of the value creation in this county were health and social work (15 %), manufacturing and mining and quarrying (15 %), business activities and real estate (13 %), wholesale and retail, hotel and restaurants (10 %) and education (9 %).

Value added for Nordland in 2005 was NOK 51 993 million, and GDP per employed person was NOK 542 083. The industries that accounted for most of the value creation in this county in 2005 were health and social work (15 %), manufacturing and mining and quarrying (13 %), business activities and real estate (14 %) and wholesale and retail, hotels and restaurants (9 %). Fishing, fish farming and related services in Nordland accounted for 20 % of the national value creation in this sector.

Footnotes

Figures supplied by the Norwegian Seafood Export Council and Statistics Norway.

SINTEF Fisheries and Aquaculture conducted an analysis of the spin-off effects of fishing and aquaculture in 2008.

County-specific data on value creation from the marine sector can be misleading because such data are often registered for companies whose official addresses are elsewhere than the main production site. The figures therefore apply to the country as a whole.

Source: Statistics Norway

Det Norske Veritas Report No. 2007–1651

Source: Maritim verdiskapingsbok 2007

Source: Maritim verdiskapingsbok 2007

Source: Hurtigruten Quarterly Report of 25 August 2008